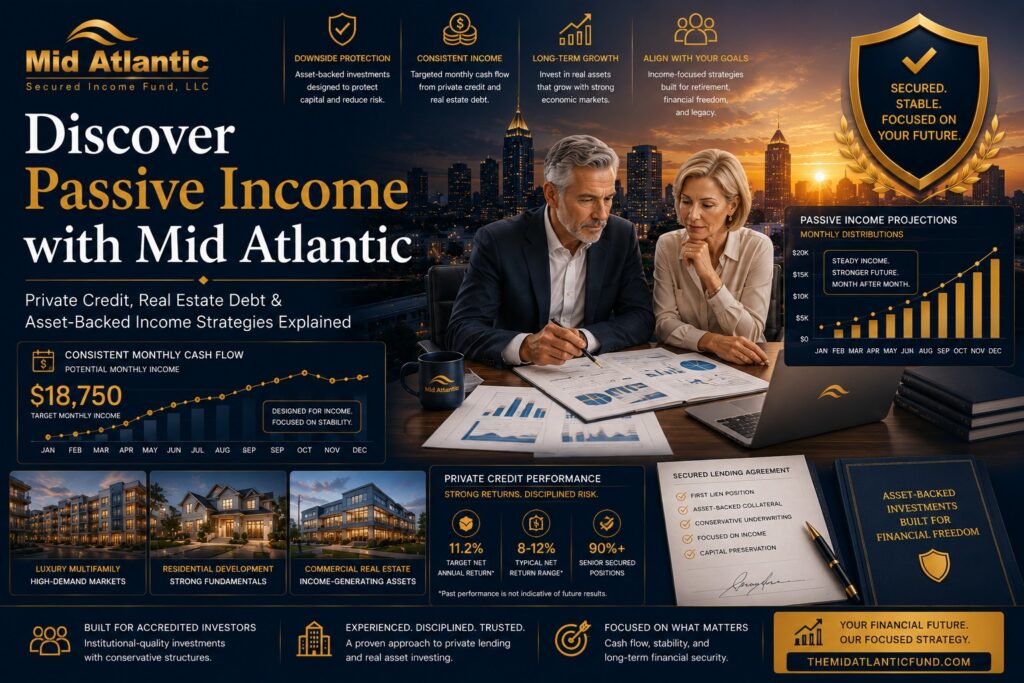

Secured Income Funds Explained: How They Work and Why Investors Use Them for Portfolio Diversification

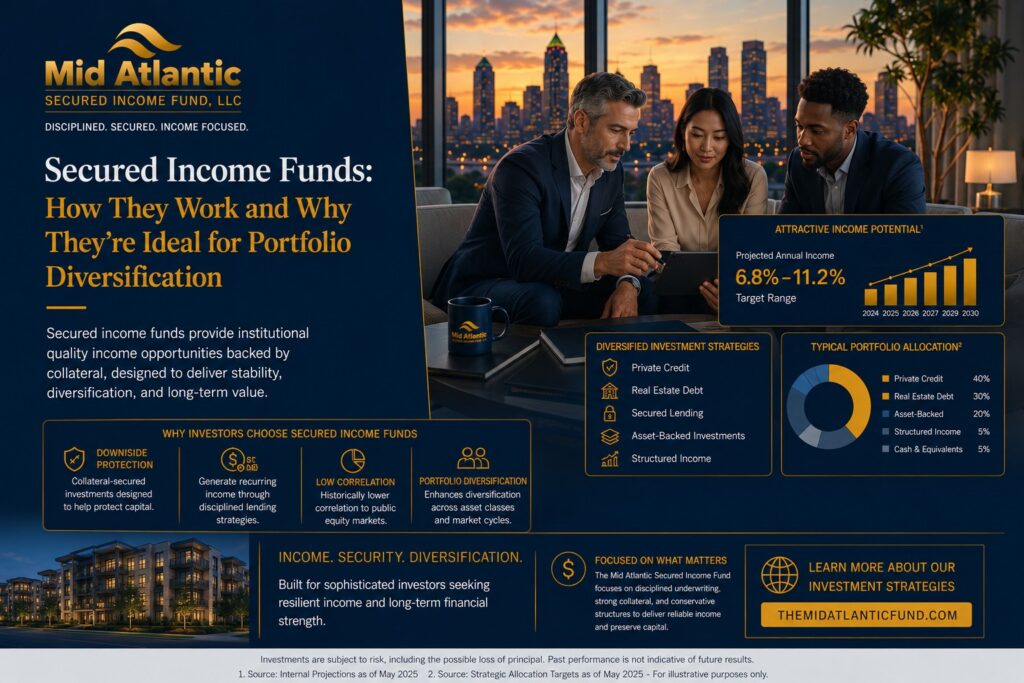

The Modern Portfolio Challenge For decades, traditional portfolio construction revolved around a familiar framework: equities for growth and bonds for stability. Yet the investment environment entering 2026 looks materially different from the one investors navigated in prior decades. Persistent inflationary pressures, elevated interest rates, geopolitical instability, regional banking concerns, and increased market volatility have forced both institutional and high-net-worth investors to rethink portfolio construction. The result is a growing shift toward alternative income-producing assets — particularly private credit and secured income strategies. Secured income funds have emerged as one of the fastest-growing categories within alternative investments because they seek to address three core investor objectives simultaneously: Consistent income generation Capital preservation Portfolio diversification This trend is not limited to institutional allocators. Family offices, RIAs, accredited investors, retirement-focused investors, and income-oriented portfolios are increasingly allocating capital toward secured lending and asset-backed income strategies. According to Preqin, global private debt assets under management surpassed approximately $1.7 trillion in recent years, with continued projected expansion driven by institutional demand for yield, downside protection, and reduced correlation to public markets. At the same time, higher interest rates have materially reshaped investor expectations around income generation and risk management. Investors are no longer simply chasing maximum returns. Increasingly, they are prioritizing durability, resilience, liquidity management, and capital discipline. Secured income funds sit directly at the center of that transition. What Is a Secured Income Fund? Direct Answer A secured income fund is an investment vehicle that generates income primarily through secured lending strategies backed by collateral such as real estate, receivables, or other assets. Unlike traditional bond funds that primarily invest in publicly traded debt securities, secured income funds often focus on private credit opportunities where investors may benefit from: contractual interest income, collateral-backed loans, senior lien positions, and enhanced downside protection structures. Many secured income funds concentrate on: real estate-backed lending, bridge lending, commercial lending, construction financing, asset-backed loans, or private credit transactions. The defining feature is collateralization. In many cases, loans are secured by tangible underlying assets that may help reduce loss severity in distressed scenarios. How Secured Income Funds Work The Core Structure Most secured income funds operate by pooling investor capital into a professionally managed lending strategy. The fund manager originates, underwrites, services, and manages loans made to borrowers. Borrowers may include: real estate developers, investors, operating businesses, bridge financing borrowers, or commercial entities seeking short-term capital solutions. Investors in the fund receive returns generated primarily through: loan interest payments, origination fees, servicing income, and other structured lending economics. Example of a Secured Lending Structure A borrower seeks a $2 million bridge loan secured by a residential redevelopment project. The secured income fund may: underwrite the project, verify collateral value, structure loan terms, establish a first-position lien, and collect monthly interest payments. If the borrower performs successfully, the fund collects contractual income. If the borrower defaults, the collateral structure may provide recovery mechanisms unavailable in unsecured lending structures. This distinction is central to why secured income investments have become increasingly attractive during volatile market environments. Why Investors Are Increasingly Using Secured Income Funds 1. Income Generation in a Volatile Market Traditional fixed-income allocations have faced significant challenges in recent years. Bond volatility increased materially during the Federal Reserve’s aggressive rate-hiking cycle. Meanwhile, many investors discovered that traditional 60/40 portfolios did not provide the same defensive characteristics historically expected. Secured income funds attempt to address this by emphasizing: contractual income streams, floating-rate exposure in some structures, shorter duration lending, and asset-backed collateral. For investors prioritizing cash flow, these strategies may offer attractive alternatives to traditional public fixed-income products. 2. Portfolio Diversification One of the primary reasons sophisticated investors allocate toward private credit and secured lending is diversification. Private credit strategies often exhibit lower correlation to public equities than traditional stock portfolios. This can help reduce portfolio concentration risk. Diversification benefits may include exposure to: private market lending, real estate debt, short-duration lending, non-public market income streams, and alternative yield sources. In volatile equity environments, diversification can become particularly valuable. 3. Capital Preservation Focus Many investors increasingly prioritize downside management over aggressive return maximization. Secured lending strategies frequently emphasize: conservative underwriting, loan-to-value discipline, collateral security, borrower vetting, and senior debt positioning. These structural protections may reduce potential loss severity compared to unsecured lending structures. The Rise of Private Credit and Alternative Income Investments Private credit has become one of the defining investment trends of the modern era. Several macroeconomic developments contributed to this growth: Bank Retrenchment Following regulatory changes after the Global Financial Crisis, many traditional banks reduced exposure to certain middle-market lending categories. This created financing gaps increasingly filled by private lenders. Higher Yield Demand Institutional investors began searching for alternatives to historically low-yield bond environments. Private credit offered: higher contractual yields, floating-rate structures, and customized lending opportunities. Institutional Adoption Major institutional firms including Apollo, Blackstone, Ares, KKR, and Blue Owl dramatically expanded private credit capabilities over the past decade. This institutional validation accelerated adoption among RIAs, family offices, and accredited investors. Are Secured Income Funds Safer Than Stocks? Direct Answer Secured income funds are not inherently “safer” than stocks, but they may offer different risk characteristics. Equities typically provide long-term growth potential but can experience substantial volatility. Secured income strategies may prioritize: income generation, lower volatility, collateral-backed structures, and downside protection mechanisms. However, risks still exist. Investors should understand: credit risk, liquidity risk, borrower default risk, real estate market risk, and fund management risk. Risk profiles vary significantly between strategies. Common Types of Secured Income Investments Real Estate Bridge Lending Short-term loans secured by residential or commercial real estate. Often used for: acquisitions, renovations, repositioning projects, or transitional financing. Construction Lending Financing provided for development or construction projects. May involve staged draw structures and detailed underwriting oversight. Asset-Backed Lending Loans secured by receivables, inventory, equipment, or contractual cash flows. Commercial Real Estate Debt Income-focused lending tied to stabilized or income-producing properties. Private Corporate Credit Senior secured loans made to operating businesses. Often structured with covenants and collateral protection. How Accredited