How to Secure Income in Volatile Markets

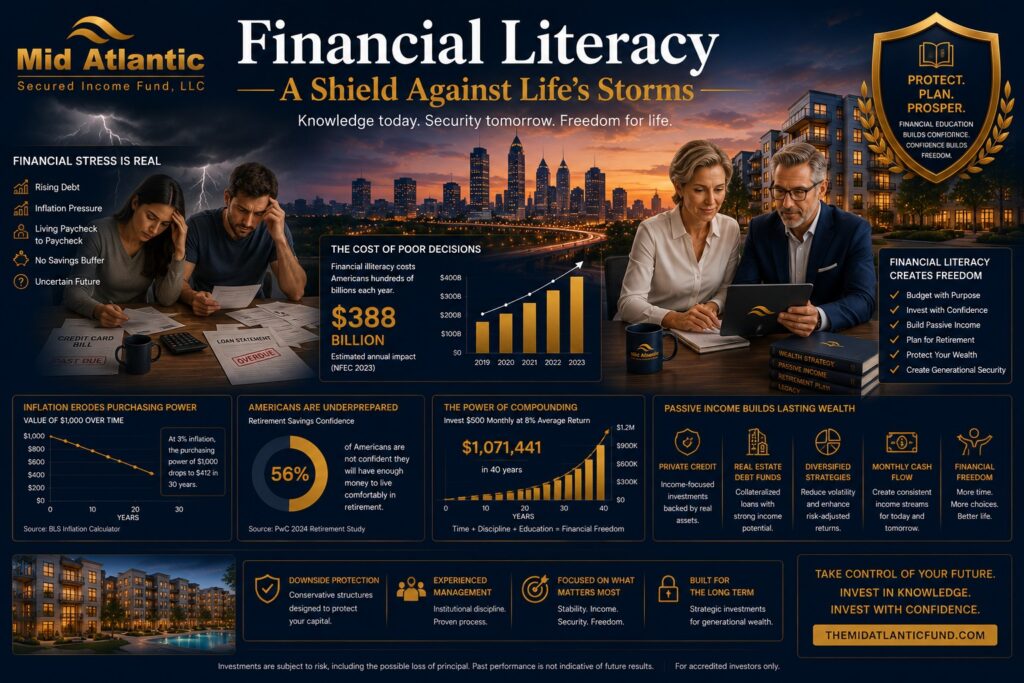

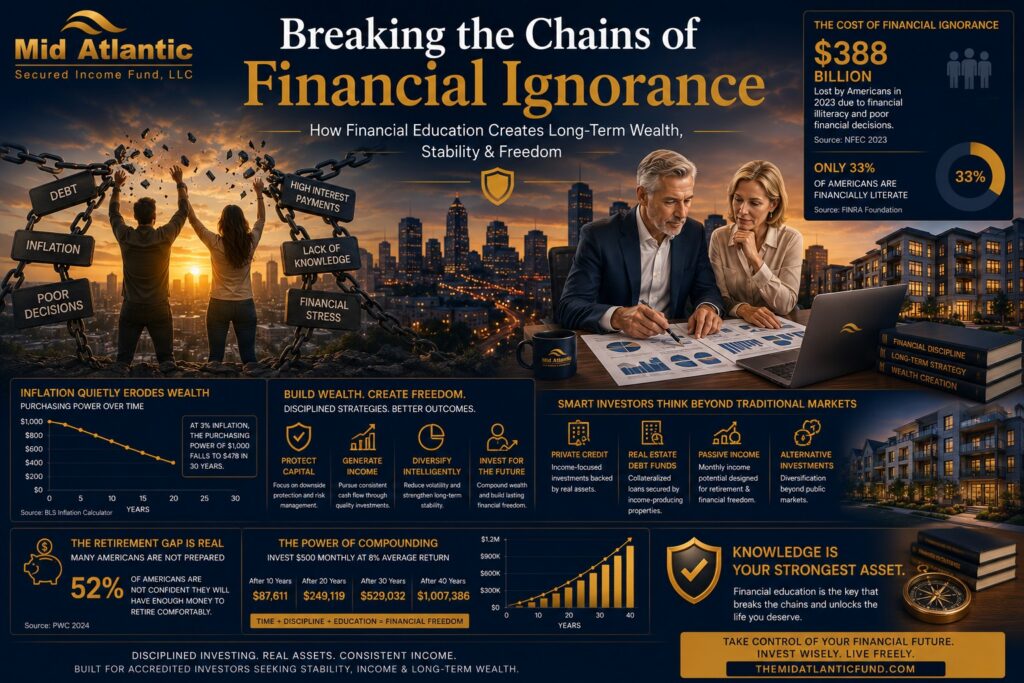

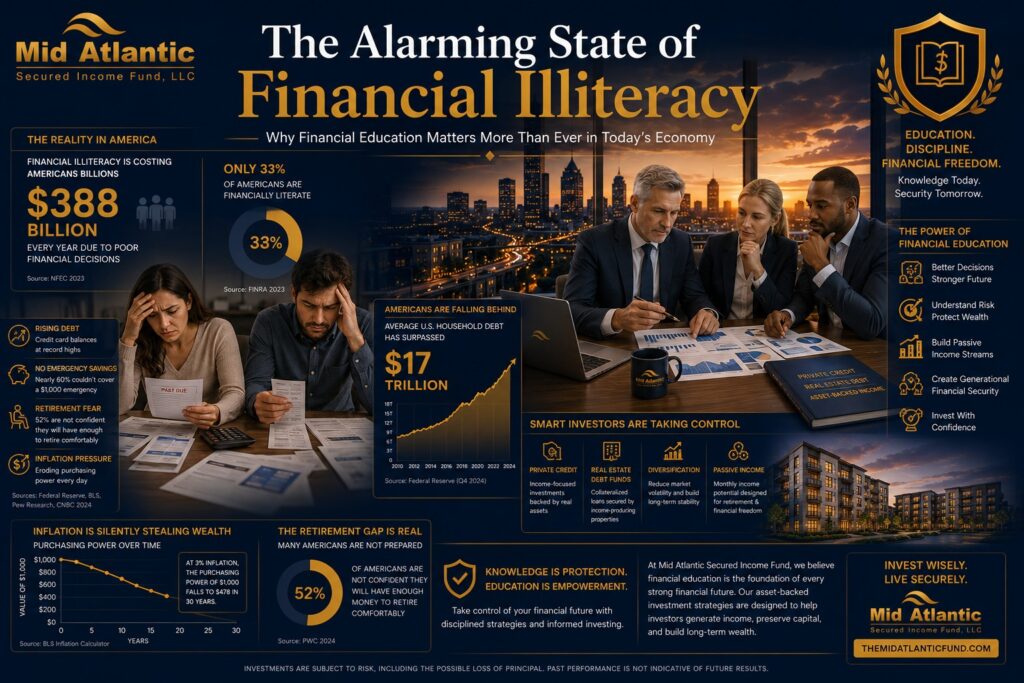

Why Investors Are Reprioritizing Stability Periods of market volatility fundamentally change investor psychology. During prolonged bull markets, many portfolios become heavily oriented toward appreciation and growth. Investors often focus on maximizing upside participation while paying comparatively less attention to downside management or income durability. Volatile markets change those priorities quickly. Sharp equity drawdowns, inflation shocks, banking instability, geopolitical disruptions, and rising interest rates tend to refocus investor attention toward: portfolio resilience, income consistency, diversification, liquidity management, and long-term financial durability. The central question increasingly becomes: “How can investors continue generating reliable income when markets become unstable?” That question has become especially relevant in the post-pandemic investment environment. According to BlackRock, Morgan Stanley, and Goldman Sachs, modern portfolio construction is increasingly shifting toward income-oriented and alternative investment strategies designed to improve resilience during uncertain economic periods. This trend has accelerated institutional interest in: private credit, secured lending, real asset exposure, alternative income investments, and asset-backed portfolio strategies. What Does It Mean to Secure Income in Volatile Markets? Direct Answer Securing income in volatile markets refers to constructing investment portfolios designed to generate more stable and predictable cash flow despite market uncertainty, economic instability, or public equity volatility. Investors often pursue this through: diversification, private credit, secured investments, real estate-backed lending, alternative fixed income, and income-producing asset-backed strategies. The goal is not eliminating risk entirely. It is improving portfolio durability and reducing excessive dependence on market appreciation alone. Why Market Volatility Has Become Structural Rather Than Temporary Volatility Is Increasingly Embedded Into Global Markets Historically, investors often treated volatility as temporary. Today, many institutions increasingly view volatility as a structural feature of modern financial markets. Several long-term forces continue contributing to elevated uncertainty: Structural Driver Impact on Markets Inflation instability Higher interest rate sensitivity Geopolitical fragmentation Increased global uncertainty Rapid monetary tightening Pressure on valuations Banking sector stress Credit market disruption Elevated sovereign debt levels Fiscal uncertainty Technology-driven market concentration Increased equity volatility According to the International Monetary Fund and McKinsey & Company, investors are entering a more fragmented and less predictable economic environment than the prior decade of ultra-low rates and highly accommodative monetary policy. This has altered how institutions think about portfolio construction. The Traditional 60/40 Portfolio Is Under Pressure Stocks and Bonds No Longer Always Offset Each Other For decades, many investors relied heavily on the traditional: 60% equities, 40% bonds portfolio structure. The assumption was straightforward: equities provided growth, bonds provided stability and income. However, inflation shocks and rising interest rates exposed weaknesses in this framework. In 2022, both equities and bonds declined simultaneously — an outcome many investors were not structurally prepared for. This challenged longstanding diversification assumptions. As a result, institutional allocators increasingly began exploring: private credit, alternative income strategies, real asset exposure, and secured investments. Why Income Matters More During Volatile Markets Income Can Reduce Dependence on Market Timing One of the defining characteristics of resilient portfolios is recurring cash flow generation. Income-producing investments may help investors avoid excessive reliance on: speculative appreciation, forced asset liquidation, or short-term market timing decisions. This becomes especially valuable during: recessions, equity drawdowns, retirement, or inflationary periods. Income-oriented portfolios may provide: psychological stability, liquidity support, and improved financial planning consistency. This explains why institutional investors increasingly prioritize cash-flow-generating investments during uncertain environments. What Are Secured Investments? Direct Answer Secured investments are investments backed by collateral or underlying assets that may provide additional layers of investor protection compared to unsecured financial structures. Examples may include: senior secured private credit, real estate-backed loans, asset-backed lending, and collateralized income-producing investments. Secured structures are often designed to prioritize repayment rights and downside awareness. Understanding Private Credit What Is Private Credit? Private credit refers to non-bank lending where investors provide capital directly to borrowers through privately structured debt investments. Private credit strategies may include: bridge lending, commercial real estate lending, construction financing, specialty finance, and asset-backed lending. According to Apollo Global Management and Preqin, private credit has become one of the fastest-growing alternative investment sectors globally. Why Private Credit Has Gained Attention During Volatile Markets Several factors explain the growing interest in private credit during uncertain environments: 1. Contractual Income Structures Private credit often generates interest-based cash flow. 2. Senior Positioning Many private loans occupy senior positions in repayment structures. 3. Collateral Backing Asset-backed structures may provide additional downside considerations. 4. Reduced Public Market Correlation Private investments may behave differently than public equities. 5. Floating-Rate Structures Certain private credit investments may adjust alongside interest rate changes. Real Estate-Backed Lending and Income Stability Why Real Assets Matter Real estate-backed lending strategies have become increasingly important within defensive portfolio construction. Unlike speculative growth assets, debt-oriented real estate investments often emphasize: contractual repayment, collateral protection, underwriting discipline, and cash flow generation. This is particularly relevant during uncertain economic periods. Institutional investors frequently evaluate: loan-to-value ratios, collateral quality, borrower strength, and asset location when assessing real estate-backed investments. Are Debt Funds Safer Than Stocks? Direct Answer Debt funds and private credit investments are not risk-free, but certain debt-oriented investment strategies may exhibit lower volatility, contractual income structures, and collateral-backed protections compared to public equities. Risk still exists and may include: borrower default, illiquidity, economic downturns, and underwriting risk. The quality of underwriting and portfolio management remains critical. Risks Investors Must Still Understand No Investment Strategy Eliminates Risk Sophisticated investors understand that volatility management is not the same as risk elimination. Key risks within income-oriented and secured investment strategies include: Risk Type Description Credit Risk Borrower default risk Liquidity Risk Limited ability to exit positions quickly Economic Risk Macroeconomic downturn impacts Interest Rate Risk Rate-driven valuation shifts Operational Risk Manager execution and servicing risk Concentration Risk Excessive exposure to one sector Institutional-quality underwriting and diversification remain central considerations. Inflation and Income Stability Inflation Changes the Definition of “Safe” Inflation is one of the most underestimated threats to long-term financial security. According to the U.S. Bureau of Labor Statistics, inflation reached multi-decade highs following pandemic-era monetary expansion and supply chain disruptions. Even moderate inflation compounds materially over time. This

How to Secure Income in Volatile Markets Read More »