Tax-Efficient Investment Strategies in 2026

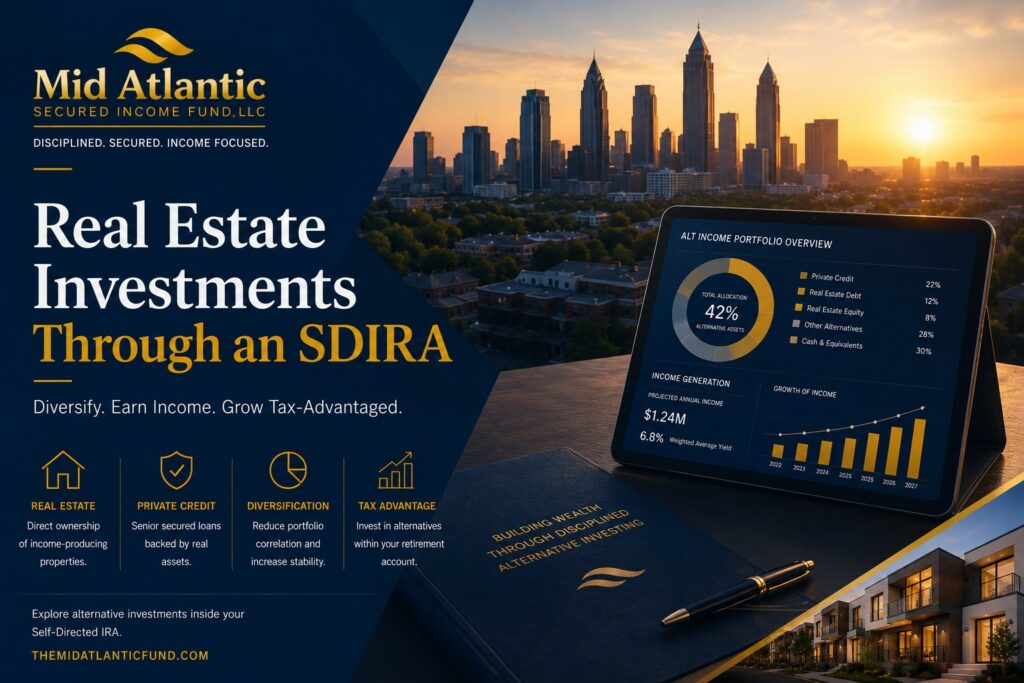

How Accredited Investors Are Structuring Portfolios for Long-Term Wealth Preservation, Income & After-Tax Performance Why After-Tax Returns Matter More Than Ever For decades, investors primarily focused on one question: “How much return can my portfolio generate?” But increasingly, sophisticated investors, family offices, wealth advisors, and accredited investors are asking a more important question: “How much of those returns do I actually keep after taxes?” That distinction has become increasingly important entering 2026. Higher investment income, elevated capital gains exposure, shifting tax policy discussions, inflationary pressures, and growing wealth concentration have made tax efficiency a central component of modern portfolio construction. Institutional investors increasingly recognize that strong nominal returns alone are insufficient if portfolios are structured inefficiently from a tax perspective. In many cases, improving after-tax efficiency can materially enhance long-term compounded wealth without requiring additional investment risk. This shift explains why accredited investors are increasingly exploring: self-directed IRAs (SDIRAs), private credit, real estate-backed investments, tax-advantaged retirement structures, alternative income strategies, and diversified portfolio frameworks designed around long-term capital preservation. The modern investment environment is no longer simply about chasing returns. It is about structuring portfolios intelligently. What Are Tax-Efficient Investment Strategies? Direct Answer Tax-efficient investment strategies are portfolio management approaches designed to maximize after-tax returns by minimizing unnecessary tax liabilities through investment selection, asset location, diversification, income structuring, and long-term planning. These strategies may involve: tax-advantaged retirement accounts, capital gains management, private market investments, municipal bonds, alternative income strategies, real estate structures, and diversified asset allocation. The goal is not tax avoidance. The goal is strategic tax optimization within existing regulatory frameworks. Why Tax Efficiency Matters More in 2026 Several structural economic trends are increasing investor focus on tax-aware portfolio construction. 1. Higher Portfolio Income Creates Higher Tax Exposure Rising interest rates have increased yields across many asset classes. While higher yields can improve portfolio income, they may also increase taxable income exposure depending on account structure and investment selection. Investors generating income from: bonds, private credit, dividends, rental cash flow, and alternative investments must increasingly evaluate the after-tax implications of portfolio design. 2. Inflation Makes Tax Drag More Painful Inflation reduces purchasing power. Taxes can compound that erosion. For example: An investor earning a 7% return while paying combined federal and state taxes may retain substantially less real purchasing power after inflation is considered. As a result, investors increasingly seek: tax-advantaged income, tax-deferred growth, and long-term compounding efficiency. 3. Public Market Volatility Has Increased Tax Awareness Market volatility often creates both risks and opportunities. Sophisticated investors increasingly use: tax-loss harvesting, rebalancing strategies, and diversification frameworks to improve long-term after-tax outcomes. The Difference Between Pre-Tax and After-Tax Returns Many investors underestimate the long-term impact of taxes on compounding. Consider two portfolios: Portfolio Annual Return Effective Tax Rate After-Tax Return Portfolio A 9% 35% 5.85% Portfolio B 7.5% 15% 6.38% Over long time horizons, tax efficiency can materially alter wealth outcomes. This is why institutional investors increasingly evaluate: tax-adjusted performance, after-tax yield, and tax-aware portfolio construction. Core Components of Tax-Efficient Investing 1. Asset Location Strategy Asset location refers to placing investments in the most tax-efficient account structures. For example: Asset Type Potential Preferred Location High-income investments Tax-advantaged accounts Growth equities Taxable accounts Alternative investments SDIRAs or retirement vehicles Municipal bonds Taxable accounts Real estate debt Tax-advantaged structures Strategic asset placement can improve long-term compounding. 2. Long-Term Capital Gains Management Long-term capital gains rates are generally lower than ordinary income tax rates. As a result, many investors emphasize: longer holding periods, tax-aware rebalancing, and lower-turnover strategies. This differs significantly from short-term speculative trading. 3. Tax-Advantaged Retirement Structures Retirement accounts remain central to tax-efficient investing. Common structures include: Traditional IRAs, Roth IRAs, 401(k)s, SEP IRAs, and Self-Directed IRAs (SDIRAs). These structures may provide: tax deferral, tax-free growth potential, or enhanced portfolio flexibility. What Is an SDIRA? Direct Answer A Self-Directed IRA (SDIRA) is a retirement account that allows investors to access alternative investments beyond traditional stocks, bonds, and mutual funds. SDIRAs may include: private credit, real estate, secured lending investments, private equity, and other alternative assets. For accredited investors, SDIRAs can create opportunities for portfolio diversification and tax-advantaged alternative investing. Why Accredited Investors Use SDIRAs Sophisticated investors increasingly use SDIRAs because they may provide: broader investment flexibility, tax-deferred or tax-free growth, alternative asset access, and enhanced diversification. In particular, SDIRAs have become increasingly popular for investors seeking exposure to: real estate-backed lending, private credit, and alternative income investments. The Growing Role of Private Credit in Tax-Efficient Portfolios Private credit has become one of the fastest-growing segments of alternative investing. According to institutional research from Preqin and Goldman Sachs, private credit assets under management have expanded significantly as investors seek: yield, diversification, and reduced public market correlation. What Is Private Credit Investing? Direct Answer Private credit investing involves non-bank lending structures where investors provide capital directly to borrowers through privately negotiated debt investments rather than publicly traded bonds. Private credit investments may include: bridge lending, commercial lending, asset-backed lending, real estate-backed loans, and specialty finance structures. These investments often emphasize: recurring income, collateral-backed security, and contractual cash flow. Why Tax Structure Matters for Passive Income Passive income is often viewed favorably by investors seeking: financial independence, retirement cash flow, and wealth preservation. However, not all passive income is taxed equally. Income from: dividends, interest, real estate, and private credit may carry different tax implications depending on: account structure, holding period, investment vehicle, and investor circumstances. This is why tax-efficient income planning has become increasingly important among high-net-worth investors. Tax-Efficient Wealth Preservation Strategies Wealth preservation and tax efficiency are closely connected. Taxes can significantly impact long-term portfolio durability. Modern wealth preservation strategies increasingly combine: diversification, tax-aware structuring, alternative investments, and income optimization. Why Family Offices Emphasize Tax Efficiency Family offices often focus heavily on: multigenerational wealth transfer, estate efficiency, tax minimization, and long-term capital durability. According to Deloitte family office surveys, alternative investments continue gaining popularity among family offices seeking: diversification, inflation resistance, and tax-aware portfolio construction. Real Estate and Tax Efficiency Real estate

Tax-Efficient Investment Strategies in 2026 Read More »