How to Use a Self-Directed IRA to Invest in Alternative Assets in 2026: What Investors Need to Know

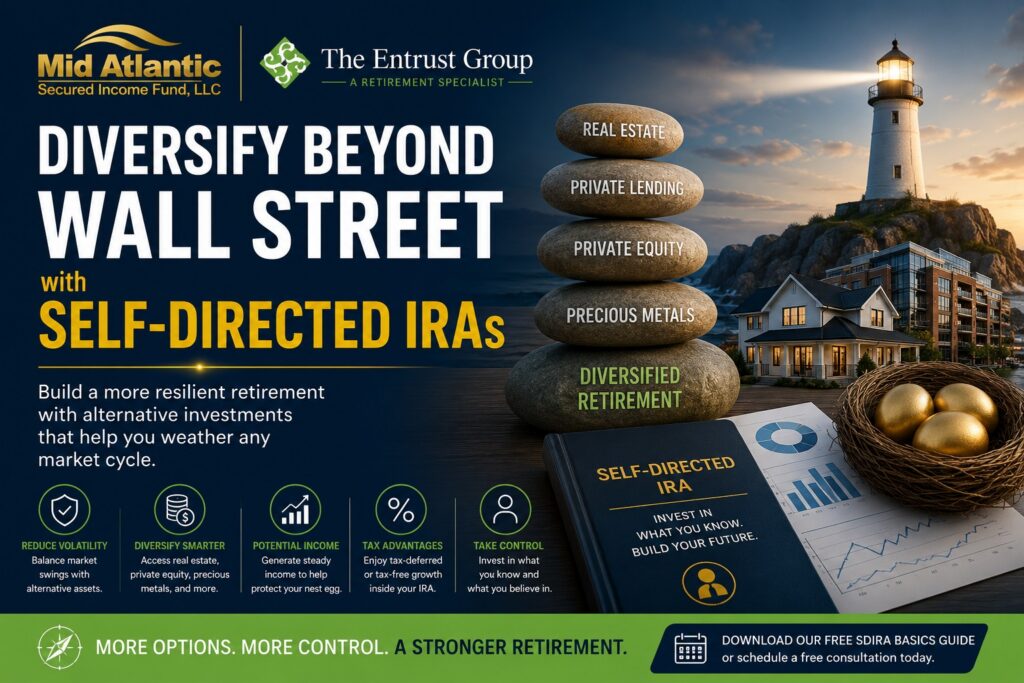

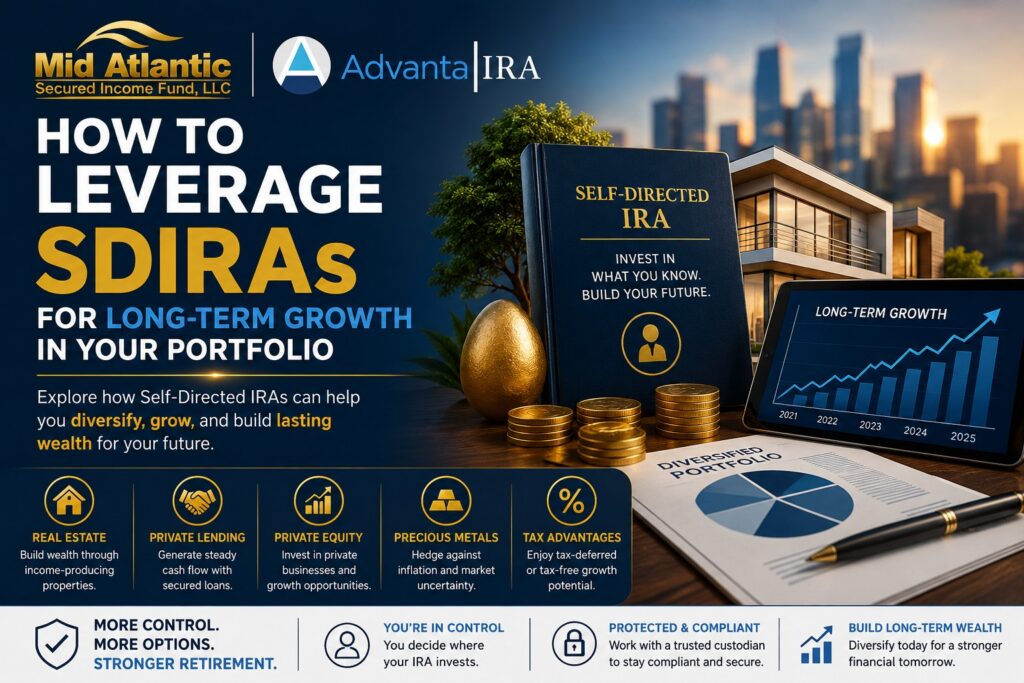

As investors continue looking for ways to diversify beyond traditional markets, self-directed IRAs (SDIRAs) have become increasingly popular. These accounts allow owners access to alternative assets to build retirement wealth. Alternative investments, such as real estate, private credit, private equity, and other non-publicly traded offerings, are not typically available through traditional brokerage accounts. For retirement savers looking for diversification strategies, understanding how self-directed IRAs work and the rules that govern them is an important first step. What Is a Self-Directed IRA? A self-directed IRA allows investors to take a more active role in their retirement strategy by choosing a broader range of investments while maintaining the same tax advantages offered by conventional retirement accounts. A self-directed IRA is a retirement account that follows the same IRS rules and tax advantages as traditional IRAs. However, self-directed investors get to invest in an asset class called alternative investments, which includes a much larger pool of options besides stocks, bonds, and mutual funds. Traditional retirement accounts held at brokerage firms typically limit investors to publicly traded assets like stocks, bonds, and mutual funds. A self-directed IRA, however, allows retirement funds to be allocated into alternative assets that fall outside those traditional categories. These accounts can be structured in the same ways as conventional retirement plans, including: Traditional IRAs Roth IRAs SEP IRAs SIMPLE IRAs Solo 401(k)s The key difference is control. With a self-directed account, the investor chooses the investments for their account. A specialized self-directed IRA custodian, such as Advanta IRA, administers the account and handles required recordkeeping and IRS reporting. This structure allows investors to incorporate assets that may behave differently from public markets and potentially enhance diversification within a retirement portfolio. Income and gains generated by investments flow into the self-directed IRA, just as it works with a conventional plan, preserving the account’s tax advantages. Why Investors Are Turning to Alternative Assets Over the past decade, alternative investments have gained attention among retirement investors seeking to reduce dependence on public market performance. Alternative assets can offer different risk and return characteristics than traditional securities, which may help create a more balanced portfolio. Some reasons investors pursue alternative assets within self-directed retirement accounts include: Diversification: Assets like real estate, gold, and private equity often move independently of stock market performance. Income potential: Many alternative investments generate recurring income, such as rental income or interest payments generated by private loans from a self-directed IRA. Access to private markets: Investors can participate in private deals and funds not available on public exchanges. Greater investment control: Self-directed accounts allow investors to pursue opportunities aligned with their expertise and investment strategy. While these advantages attract many investors, alternative investments also require careful research, due diligence, and adherence to IRS rules governing retirement accounts. Common Alternative Assets Used in Self-Directed IRAs The IRS permits retirement accounts to hold many types of investments as long as they are not specifically prohibited. As a result, self-directed IRAs are used to invest in a variety of alternative asset classes. Real Estate Real estate remains one of the most widely used investments within self-directed IRAs. Investors may purchase assets such as: Residential rental properties Commercial real estate Raw land Real estate investment partnerships or syndications Private Credit Private credit investments have become increasingly popular as investors seek income-producing passive assets. Through a self-directed IRA, investors may participate in: Private lending arrangements Mortgage notes Debt funds Bridge loans These investments can provide interest income while allowing investors to participate in financing opportunities outside traditional banking channels. Private Equity and Private Placements Self-directed IRAs can also be used to invest in privately held companies or funds, including: Venture capital investments Startup opportunities Private equity funds Private stock These investments often target long-term growth and allow retirement investors to participate in opportunities typically available only to accredited investors. Precious Metals Certain precious metals that meet IRS purity requirements can also be held within a self-directed IRA. Gold, silver, platinum, and palladium are commonly used by investors who want exposure to tangible assets or potential inflation hedges. How to Open and Fund a Self-Directed IRA Opening a self-directed IRA typically follows a straightforward process, although it requires working with a custodian that supports alternative investments. Choose a Self-Directed IRA Custodian Because traditional brokerages generally do not administer alternative assets, investors must open accounts with custodians that specialize in self-directed retirement plans. These custodians provide the administrative infrastructure necessary for alternative investments. Not all custodians are alike. Fee structures differ. Not all custodians allow every available alternative asset. Some are more experienced with specific investments than others. Investors must make sure the self-directed custodian they choose fits the criteria for their investing goals. Open the Account The investor completes an account application and selects the appropriate plan type, such as a traditional IRA, Roth IRA, or SEP IRA. Fund the Account Self-directed IRAs can be funded in several ways: Transfers from existing IRAs Rollovers from employer-sponsored retirement plans Annual contributions Identify an Investment Once the account is funded, the investor performs due diligence and identifies an investment opportunity that aligns with their strategy. The custodian then processes the transaction and ensures the asset is titled properly in the name of the retirement account. Key Compliance Rules Investors Should Understand Although self-directed IRAs allow a wide range of investment options, they must still follow IRS rules governing retirement accounts. Understanding these rules is critical to preserving the account’s tax-advantaged status. Prohibited Transactions The IRS prohibits certain transactions between a retirement account and disqualified persons, which include: The account owner Spouses Parents and grandparents Children and grandchildren Entities controlled by the account holder or other disqualified persons Fiduciaries, investment advisors, or anyone providing service to the SDIRA Examples of prohibited transactions include: Using IRA-owned property for personal benefit Selling personal assets to the IRA Buying an investment from a disqualified person Prohibited Investments Per IRS regulations, self-directed IRAs may not invest in: Life insurance Collectibles (i.e., works of art, alcohol, certain coins) Violating