Why Passive Income Has Become a Defining Financial Objective

For decades, passive income was often framed as an aspirational lifestyle concept — a way to supplement earnings, retire early, or achieve greater personal freedom. Today, it has become something far more important: a core financial strategy.

Persistent inflation, elevated interest rates, rising healthcare costs, market volatility, and concerns around retirement preparedness have fundamentally changed how investors think about wealth creation. Increasingly, affluent households, retirees, entrepreneurs, and accredited investors are prioritizing income-producing assets capable of generating recurring cash flow independent of active labor.

This shift is occurring against a powerful macroeconomic backdrop.

According to the Federal Reserve’s Survey of Consumer Finances, median retirement savings remain insufficient for many Americans relative to projected retirement needs. Meanwhile, inflation-adjusted purchasing power has been challenged by elevated housing, insurance, energy, and healthcare costs in recent years. Traditional stock-and-bond portfolios have also experienced periods of simultaneous volatility, forcing investors to reconsider the importance of diversification and non-correlated income streams.

As a result, passive income is no longer viewed solely as a retirement objective. It is increasingly becoming a portfolio construction priority.

Sophisticated investors are now exploring broader categories of income-producing assets, including:

- Private credit

- Real estate-backed lending

- Infrastructure investments

- Dividend-oriented equities

- Income-producing real estate

- Alternative investment funds

- Asset-backed debt structures

- Structured fixed-income solutions

This evolution reflects a broader institutional trend. Over the past decade, alternative investments and private markets have experienced substantial growth as institutional allocators searched for enhanced yield, diversification, downside protection, and contractual income streams.

In many ways, passive income investing today resembles institutional portfolio construction more than traditional retail investing.

What Is Passive Income?

Direct Answer

Passive income refers to recurring earnings generated from investments or assets that do not require ongoing active labor to maintain. Common examples include interest payments, rental income, dividends, private credit distributions, royalties, and income generated through investment funds.

Unlike earned income from employment or business operations, passive income is designed to create ongoing cash flow from invested capital.

The Evolution of Passive Income Investing

Historically, passive income strategies centered around:

- Dividend-paying stocks

- Rental properties

- Treasury bonds

- CDs and savings accounts

While these vehicles remain relevant, modern passive income investing has evolved considerably.

Today’s investors operate in a more complex environment shaped by:

- Higher inflation volatility

- Longer life expectancies

- Greater retirement uncertainty

- Increased institutional participation in private markets

- Reduced pension availability

- Greater demand for alternative investments

As a result, passive income portfolios increasingly include private market investments once primarily reserved for institutions and ultra-high-net-worth investors.

This includes areas such as:

Private Credit

Private credit refers to non-bank lending arrangements involving privately negotiated debt structures. These may include:

- Real estate bridge loans

- Asset-backed lending

- commercial lending

- specialty finance

- receivables financing

- secured business lending

Private credit has expanded rapidly following post-2008 banking regulations that reduced traditional bank lending activity in certain sectors.

Preqin projects private debt assets under management could surpass $2.8 trillion globally by 2028, reflecting sustained institutional demand for yield-oriented strategies.

Why Investors Are Prioritizing Passive Income Today

1. Inflation Has Changed Retirement Planning

Inflation materially impacts purchasing power over time.

Even moderate inflation can significantly erode retirement savings over multi-decade periods. Investors increasingly recognize the importance of assets capable of generating income growth or maintaining yield spreads above inflationary pressures.

This has increased interest in:

- Floating-rate credit

- Short-duration lending

- real assets

- real estate-backed investments

- alternative income strategies

2. Longevity Risk Is Increasing

Americans are living longer.

Longer retirements create additional pressure on investment portfolios to generate sustainable income over extended periods.

Traditional retirement models built around conservative bond allocations may no longer fully address income requirements in higher-cost environments.

As a result, investors are increasingly exploring diversified income streams beyond traditional fixed income.

3. Market Volatility Has Increased Diversification Demand

Periods of equity market volatility have reinforced the importance of portfolio diversification.

Sophisticated investors increasingly seek investments with:

- lower correlation to public equities

- contractual cash flow structures

- collateral-backed protections

- shorter duration exposure

- income-oriented return profiles

Private credit and real estate-backed debt have become particularly attractive in this environment.

Understanding Private Credit as a Passive Income Strategy

What Is Private Credit?

Private credit involves lending capital outside traditional public bond markets.

These loans are often directly negotiated between lenders and borrowers and may involve:

- real estate collateral

- business assets

- receivables

- contractual cash flows

- personal guarantees

- structured underwriting protections

Many private credit investments generate recurring income through scheduled interest payments.

Why Institutional Investors Favor Private Credit

Institutional allocators have increasingly embraced private credit because it may offer:

- Enhanced yield potential relative to traditional bonds

- Senior secured positioning

- Contractual income streams

- Shorter loan durations

- Asset-backed collateral protection

- Portfolio diversification

BlackRock, Apollo, Ares, and other institutional managers have significantly expanded private credit platforms in recent years.

The appeal largely stems from risk-adjusted income potential and diversification characteristics.

How Real Estate-Backed Lending Generates Passive Income

Real estate-backed lending is one of the most common forms of private credit.

In these structures, loans are secured by underlying real estate assets, which may include:

- Residential developments

- Multifamily properties

- Commercial real estate

- Construction projects

- Bridge financing opportunities

Income is typically generated through interest payments made by borrowers.

Because these investments may be collateralized by tangible real estate assets, many investors view them as more conservative than unsecured lending arrangements.

Are Debt Funds Safer Than Stocks?

Direct Answer

Debt-focused investments are not risk-free, but they generally occupy a higher position in the capital stack than equity investments. In many structures, lenders receive repayment priority ahead of common equity holders.

This can potentially reduce downside exposure relative to pure equity investing, particularly when loans are secured by collateral and underwritten conservatively.

However, risks still exist, including:

- borrower default

- real estate market declines

- liquidity constraints

- interest rate changes

- economic downturns

Investors should always evaluate underwriting quality, collateral protection, diversification, and manager experience.

Passive Income vs. Growth Investing

|

Passive Income Investing |

Growth Investing |

|---|---|

|

Focuses on recurring cash flow |

Focuses on capital appreciation |

|

Often prioritizes stability |

Often prioritizes long-term upside |

|

Frequently uses debt structures |

Primarily equity-oriented |

|

Can support retirement income |

Can support long-term accumulation |

|

Often lower volatility |

Often higher volatility |

|

May emphasize downside protection |

May emphasize aggressive growth |

Most sophisticated portfolios incorporate elements of both.

The Psychology of Passive Income

Passive income is not only a financial strategy. It is also a psychological framework.

Many investors pursue passive income because it can potentially provide:

- Greater financial flexibility

- Reduced reliance on employment income

- Improved retirement confidence

- More predictable cash flow

- Emotional stability during market volatility

Behavioral finance research consistently shows investors value predictability and income stability during uncertain economic periods.

Recurring income streams can reduce the emotional pressure associated with market fluctuations.

How Accredited Investors Use Passive Income Strategies

Accredited investors often gain access to broader investment opportunities unavailable in public markets.

These may include:

- Private credit funds

- Real estate debt funds

- Institutional lending platforms

- Alternative income strategies

- Structured finance opportunities

Many accredited investors allocate portions of their portfolios toward income-oriented alternatives to complement traditional stock and bond exposure.

What Are the Risks of Passive Income Investments?

Direct Answer

Passive income investments can involve meaningful risks depending on structure, liquidity, leverage, underwriting quality, and market conditions.

Potential risks include:

- Credit/default risk

- Liquidity risk

- Real estate market risk

- Interest rate risk

- Manager execution risk

- Economic downturn exposure

No investment strategy guarantees positive returns or principal preservation.

Risk management and underwriting discipline remain critical.

The Role of Diversification in Income Portfolios

Sophisticated income portfolios rarely rely on a single asset class.

Institutional investors frequently diversify across:

- Public fixed income

- Private credit

- Real estate debt

- Dividend equities

- Infrastructure

- Cash equivalents

- Alternative income strategies

Diversification helps reduce concentration risk and may improve portfolio resilience.

Why Short-Duration Lending Has Gained Attention

Higher-rate environments have increased investor interest in shorter-duration lending structures.

Shorter loan durations may provide:

- Faster capital recycling

- Reduced duration risk

- Greater flexibility during changing rate environments

- More frequent repricing opportunities

Bridge lending and transitional lending strategies have become increasingly prominent in private credit markets.

Passive Income and Retirement Planning

Retirement planning has fundamentally shifted from accumulation toward distribution efficiency.

Today’s retirees increasingly focus on:

- Sustainable withdrawal strategies

- Inflation resilience

- Monthly cash flow reliability

- Capital preservation

- Longevity protection

Passive income strategies can play an important role in retirement portfolios when integrated thoughtfully within broader financial plans.

Why Alternative Investments Continue to Grow

Alternative investments have expanded significantly over the last two decades.

Institutional investors increasingly allocate capital toward alternatives because they may provide:

- Enhanced diversification

- Reduced public market correlation

- Income generation

- Inflation sensitivity

- Access to private markets

According to BlackRock and Preqin research, alternatives continue to represent one of the fastest-growing areas of global asset allocation.

The Importance of Underwriting Discipline

In private credit investing, underwriting quality often matters more than headline yield.

Sophisticated investors evaluate factors such as:

- Loan-to-value ratios

- Collateral quality

- Borrower experience

- Exit strategy viability

- Market fundamentals

- Geographic trends

- Capital structure protections

Disciplined underwriting can materially influence long-term portfolio performance.

Why the Southeast Has Attracted Investment Capital

The Southeast United States — including Atlanta and broader Sun Belt markets — has experienced substantial population and economic growth.

Drivers include:

- Business migration

- Population inflows

- Housing demand

- Employment growth

- Infrastructure expansion

- Relative affordability

These trends have increased institutional interest in real estate-backed lending opportunities throughout the region.

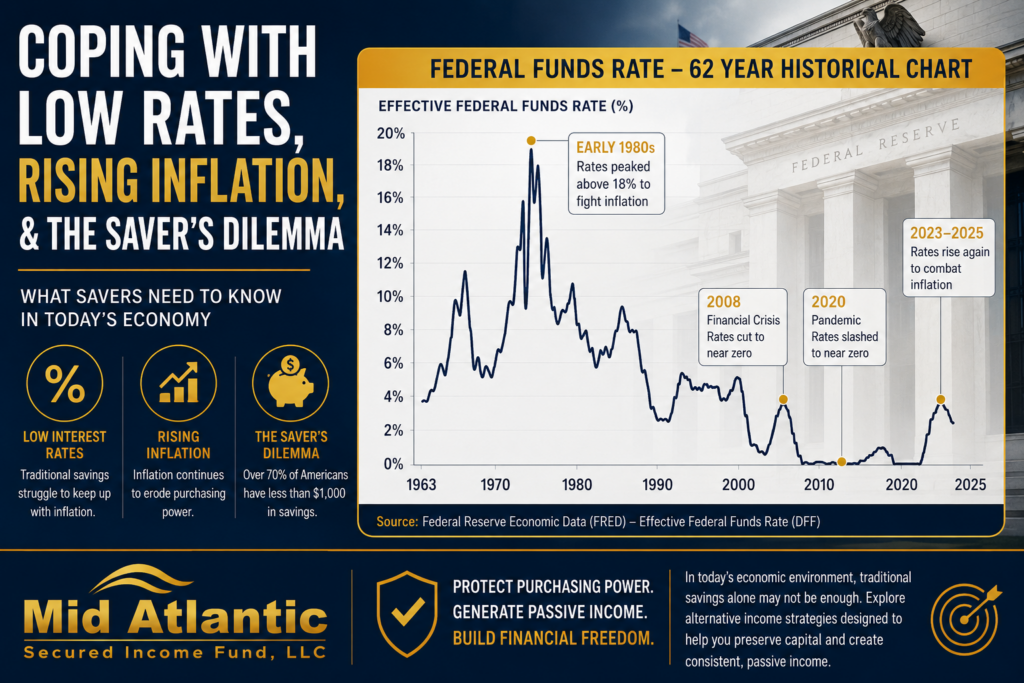

Passive Income in a Higher-Rate Environment

Higher interest rates have reshaped fixed-income markets.

For years following the Global Financial Crisis, historically low interest rates limited income generation opportunities. More recently, elevated rates have increased yields across various credit-oriented strategies.

This environment has renewed interest in:

- Private credit

- Floating-rate lending

- Structured income investments

- Asset-backed debt

However, elevated rates also increase borrower stress, making underwriting discipline increasingly important.

The Institutionalization of Private Markets

Private markets are no longer niche investment categories.

Large institutions, pension funds, insurance companies, family offices, and sovereign wealth funds increasingly allocate substantial capital toward:

- Private equity

- Private credit

- Infrastructure

- Real assets

- Alternative income strategies

This institutionalization reflects growing recognition that public markets alone may not provide sufficient diversification or income potential.

How Investors Evaluate Income Investments

Sophisticated investors often analyze:

Yield Quality

Is the income contractual or speculative?

Collateral Protection

Are investments secured by tangible assets?

Duration

How long is capital committed?

Diversification

Is exposure concentrated or diversified?

Manager Experience

Does the investment manager have underwriting expertise and operational discipline?

Market Conditions

How do macroeconomic trends affect risk and opportunity?

The Growing Importance of Financial Education

Financial literacy remains a major challenge in the United States.

Many investors still misunderstand:

- compound interest

- inflation

- risk-adjusted returns

- diversification

- retirement sustainability

- alternative investments

As private markets become increasingly accessible, investor education becomes even more important.

Educational content plays a critical role in helping investors evaluate opportunities responsibly.

Where Passive Income Fits Within Long-Term Wealth Planning

Passive income strategies are rarely standalone solutions.

Instead, they often serve as components within broader wealth management frameworks focused on:

- financial independence

- retirement income

- diversification

- capital preservation

- tax efficiency

- legacy planning

Sophisticated portfolio construction balances income generation with risk management and long-term growth objectives.

Conclusion: Passive Income Has Become a Strategic Portfolio Priority

Passive income investing has evolved far beyond simplistic “earn money while you sleep” narratives.

In today’s environment, it increasingly represents a sophisticated portfolio construction discipline centered around:

- recurring cash flow

- downside awareness

- diversification

- contractual income streams

- real asset exposure

- long-term resilience

Institutional investors have already embraced this shift.

Increasingly, accredited investors and affluent households are following similar principles by exploring private credit, real estate-backed lending, and alternative investment strategies capable of supporting durable income generation.

While no strategy eliminates risk, disciplined income-oriented investing may help investors pursue greater stability, flexibility, and long-term financial resilience in an increasingly uncertain world.

FAQ Section

What is passive income?

Passive income refers to recurring earnings generated from investments or assets requiring limited day-to-day active involvement.

What are common passive income investments?

Common passive income investments include dividend stocks, bonds, private credit, rental real estate, REITs, and income-focused alternative investments.

Why are investors interested in private credit?

Private credit may provide enhanced yield potential, contractual income streams, diversification benefits, and asset-backed collateral structures.

Are passive income investments safe?

No investment is completely safe. Passive income investments carry varying levels of credit, market, liquidity, and economic risk.

How do accredited investors use passive income strategies?

Many accredited investors allocate capital toward private credit, real estate-backed lending, and alternative income investments to complement traditional portfolios.

Why has passive income become more important recently?

Inflation, market volatility, retirement concerns, and changing economic conditions have increased demand for recurring income-producing investments.