When a portfolio built for income stops producing enough income, investors usually feel it before they see it on a statement. Cash drag, lower bond yields, and public market volatility can turn a retirement or treasury allocation problem into a planning problem. That is where private real estate lending opportunities begin to stand out – not as a replacement for every other asset class, but as a disciplined way to pursue current income through collateral-backed credit.

For accredited investors, the appeal is straightforward. Instead of taking equity risk on a property and waiting for appreciation, private lending focuses on the borrower’s ability to repay and the value of the underlying real estate securing the loan. The investment thesis is less about predicting market enthusiasm and more about underwriting, collateral coverage, loan structure, and duration. That distinction matters, especially in periods when capital preservation becomes just as important as yield.

What private real estate lending opportunities actually are

At a basic level, private real estate lending involves originating or participating in loans secured by real property. These loans are often short term and may finance acquisition, construction, renovation, redevelopment, or bridge needs. In many cases, the lender holds a first-position mortgage, which means it has senior claim on the collateral if the loan does not perform as agreed.

That structure is very different from owning rental property directly or investing in a common equity real estate vehicle. With direct ownership, investors absorb operating risk, leasing risk, expense inflation, and market timing risk. With private credit, the focus shifts to contractual payments, lien priority, and a defined repayment path. The borrower may benefit from speed and flexibility. The investor may benefit from income and an asset-backed risk framework.

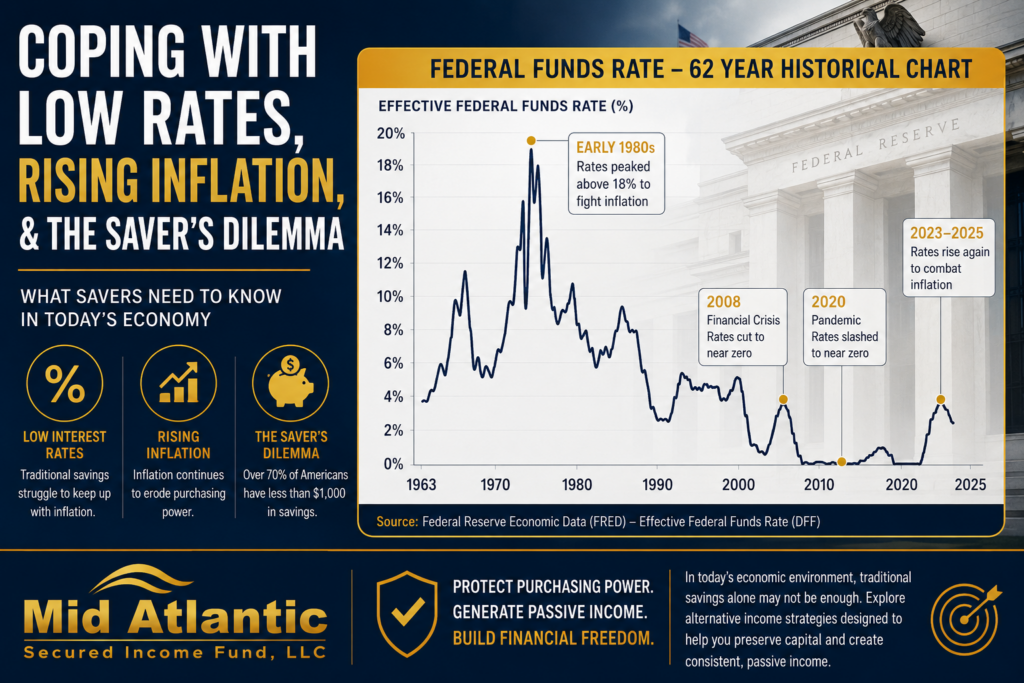

This is one reason private credit has attracted increasing attention from institutional and high-net-worth investors. The Federal Reserve’s higher-rate environment has changed the math for both borrowers and capital providers, but it has not eliminated demand for transitional real estate financing. In fact, when banks tighten underwriting or reduce exposure to certain property types, non-bank private lenders often become more relevant.

Why accredited investors are looking more closely now

The case for private real estate lending opportunities is not based on novelty. It is based on the gap between what many investors need and what traditional income allocations currently provide.

Public fixed income can still serve an important role, but duration risk, rate sensitivity, and reinvestment uncertainty remain real concerns. Equities may provide long-term growth, yet they are often too volatile for investors prioritizing dependable cash flow. Private real estate credit sits in a different part of the risk-return spectrum. It is generally illiquid, and that trade-off should be acknowledged clearly, but in exchange it may offer higher current income and lower mark-to-market volatility than publicly traded alternatives.

For retirees, rollover IRA investors, and self-directed IRA investors, that combination can be especially compelling. The objective is often not to maximize upside. It is to build a more durable income stream backed by hard assets and conservative underwriting. In that context, private credit is less about chasing returns and more about improving the structure of the income sleeve of a portfolio.

The features that separate disciplined lending from speculative lending

Not all private lending is created equal. The quality of an opportunity depends far less on the headline rate than on the underwriting standards behind it.

The first question is lien position. A first-position mortgage generally offers stronger protection than subordinated or mezzanine exposure because repayment priority matters in distressed scenarios. The second is loan-to-value ratio. Conservative leverage, often in the 65% to 75% range, can provide a meaningful equity cushion beneath the lender’s capital. That cushion is not a guarantee against loss, but it can materially improve downside protection.

The third is duration. Short-term loans can reduce exposure to long-cycle uncertainty, particularly in changing rate environments. If a loan is expected to repay in 6 to 18 months rather than 5 to 10 years, the lender may have more flexibility to reprice risk and recycle capital.

The fourth is the manager’s operating capability. Origination is only one part of the business. Servicing, draw management, borrower communication, collateral monitoring, and workout experience all matter. A lender that can source deals but not manage credit events is not truly built for risk management.

Finally, there is sponsor discipline. Investors should care about whether the manager is focused on preserving capital first or stretching for yield. That difference often shows up in the details – appraisal review, title and insurance verification, borrower experience, exit analysis, and reserves.

Where the opportunity tends to be strongest

Private real estate lending opportunities are often strongest in situations where financing needs are real, time-sensitive, and not ideally suited to traditional bank underwriting. Bridge loans are one example. A borrower may need short-duration capital to acquire an asset, stabilize occupancy, or complete a business plan before refinancing or sale.

Construction and renovation lending can also be attractive when managed carefully. These loans can carry execution risk, so disciplined draw controls and budget oversight are essential. But when the collateral, borrower experience, and capital structure are properly underwritten, they can provide compelling income with tangible asset support.

Redevelopment and value-add projects can fit as well, though selectivity matters. The right opportunity is not simply the one with the highest projected spread. It is the one where the lender has multiple ways to get repaid and enough collateral protection if the timeline slips.

Commercial and residential loans each have a place. Residential assets may offer greater familiarity and broader liquidity in some markets. Commercial assets can provide strong opportunities too, but they require more nuanced underwriting tied to tenancy, cash flow, use case, and local market depth. There is no universal winner. It depends on the lender’s expertise and the discipline of the credit process.

What risks deserve the most attention

Private credit is often described as lower volatility, which can be true relative to public markets. Lower volatility does not mean low risk in every scenario.

The central risk is credit risk – the borrower may not repay on schedule or at all. Real estate-backed lending adds collateral protection, but collateral is only useful if it is properly valued, legally secured, and sufficiently liquid in a downside scenario. That is why independent valuation, title review, insurance requirements, and legal documentation are not administrative details. They are part of the risk framework.

Liquidity risk is also significant. Private funds and private loans are not designed for daily redemptions. Investors should match these allocations to capital that can remain committed through the expected term. If an investor needs immediate flexibility, that mismatch should be addressed before investing, not after.

There is also manager risk. A strong-looking portfolio can still underperform if the manager weakens underwriting to deploy capital, concentrates exposure too heavily, or lacks workout experience. In private credit, manager selection is often as important as asset selection.

How to evaluate private real estate lending opportunities

A sophisticated review starts with the basics. What type of loans does the manager originate? Are they first-position mortgages? What is the typical loan-to-value range? What property types are financed? What is the average loan term? How are borrowers sourced and screened?

From there, investors should assess process quality. Is underwriting centralized and documented? Are valuations and legal reviews handled by qualified third parties? How are construction draws controlled? What happens when a borrower misses milestones or requests an extension?

Track record should be evaluated carefully. Longevity alone is not enough. Investors should look for evidence of credit discipline across market conditions, consistency of distributions if applicable, and clarity around realized losses, if any. Transparency matters. So does the willingness to discuss what can go wrong.

For investors using self-directed IRAs or rollover retirement capital, structure matters as well. The strategy should fit the account type, liquidity needs, and income objectives. While investors should consult their own tax and legal advisors on account-specific considerations, the broader point is simple: retirement capital often benefits from strategies built around contractual income and risk controls rather than appreciation-driven uncertainty.

A firm such as Mid Atlantic Secured Income Fund reflects the type of framework many accredited investors seek – short-duration, real estate-backed lending with first-lien focus, conservative leverage, and emphasis on consistent income over speculation.

Why this part of private credit deserves a place on the shortlist

The strongest case for private real estate lending is not that it outperforms every other option in every environment. It is that it addresses a specific investor need with a structure designed around security and income. For accredited investors who want hard-asset backing, current cash flow, and lower dependence on public market pricing, that can be a meaningful advantage.

There are trade-offs. Private strategies require patience, due diligence, and comfort with reduced liquidity. They also require trust in the manager’s underwriting discipline. But for investors willing to make that trade, private real estate credit can offer something increasingly valuable: income that is tied to contracts, collateral, and process rather than sentiment.

The most durable opportunities are usually the least theatrical. They come from conservative structures, experienced operators, and a clear commitment to managing risk before reaching for return. That is often where confidence is built, and where income strategies tend to age well.