When income investors review their options today, the biggest frustration is not a lack of choices. It is a lack of confidence in how those choices behave when markets turn volatile, rates shift, or property values soften. That is where senior secured real estate investment stands apart. It is built around collateral, loan priority, and disciplined underwriting rather than appreciation assumptions or equity upside projections.

For accredited investors seeking dependable cash flow, that distinction matters. A senior secured position means the investment is backed by real estate and sits first in the repayment stack. If a borrower repays on schedule, investors receive the expected income. If a project faces stress, the lender’s senior claim on the collateral becomes a central line of defense. That does not remove risk, but it changes the risk profile in a meaningful way.

What senior secured real estate investment actually means

At its core, a senior secured real estate investment is an investment tied to a loan, not direct property ownership. The investor’s capital is deployed into debt backed by real estate, typically through a fund or private credit structure. The word senior refers to repayment priority. The word secured means the loan is collateralized by a mortgage or deed of trust on a specific property.

This structure differs from common equity real estate investing, where returns often depend on rent growth, cap rate compression, or a future sale at a higher price. In senior secured lending, the primary objective is current income and principal protection through the borrower’s contractual obligation to repay. The property serves as the lender’s collateral support, not simply the source of hoped-for upside.

In practical terms, many private real estate credit strategies focus on first-position mortgage loans for residential and commercial assets, including new construction, bridge financing, redevelopment, and transitional business-purpose loans. For investors, the appeal is straightforward – income is generated from loan interest, while downside protection is supported by collateral value and legal claim priority.

Why accredited investors look at this part of the market

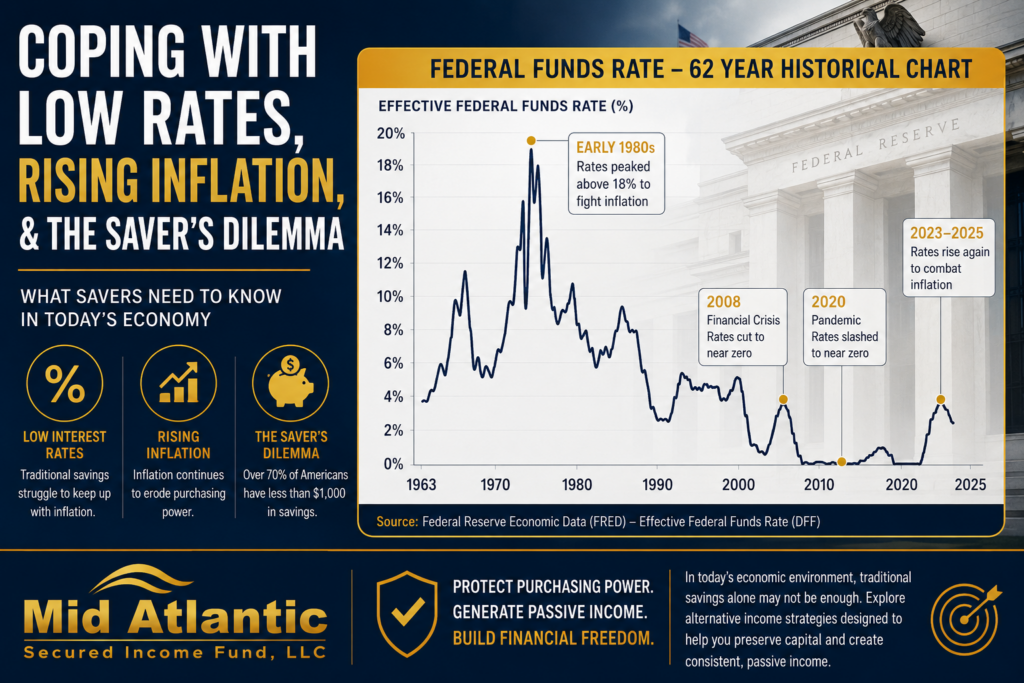

Traditional fixed-income allocations have become harder to rely on for predictable real after-inflation income. Public bonds can be sensitive to interest rate moves, and listed income products can still carry meaningful market volatility. Public REITs may provide yield, but they also trade like equities and can move sharply even when underlying real estate fundamentals remain stable.

Senior secured real estate investment offers a different exposure. Instead of buying a publicly traded security whose price can reprice minute by minute, investors are allocating to private loans with defined terms, stated rates, and specific collateral. That can be especially relevant for retirees, rollover IRA investors, and self-directed IRA investors who prioritize monthly or periodic income over mark-to-market fluctuations.

The Federal Reserve’s rate cycles and broader credit conditions also tend to push more borrowers toward private lenders when banks tighten standards. Data from the Federal Reserve’s Senior Loan Officer Opinion Survey has repeatedly shown that bank credit availability can contract in periods of uncertainty. When conventional lenders pull back, disciplined private lenders may be able to originate loans at stronger pricing and more conservative structures. For investors, that can create an environment where yield is supported by tighter underwriting rather than greater speculation.

The risk controls that matter most

Not all secured lending is equally conservative. The quality of a senior secured real estate investment depends less on the label and more on how the loans are originated, underwritten, and serviced.

Loan-to-value ratio is one of the first metrics sophisticated investors should examine. A lender originating in the 65 to 75 percent range generally preserves a collateral cushion beneath the loan balance. That buffer matters because repayment outcomes are not driven only by the original business plan. They are influenced by market conditions, construction timelines, leasing performance, and borrower execution. Conservative leverage gives the lender more room to manage through those variables.

The second critical factor is lien position. First-position mortgages have priority over junior debt and equity. If a workout, sale, or foreclosure becomes necessary, that senior status is central to recovery prospects. A high stated yield attached to a weaker position in the capital stack can be less attractive than a moderate yield with stronger structural protection.

The third factor is underwriting discipline. Strong private credit managers do not underwrite to best-case scenarios. They review borrower experience, guarantor strength, exit strategy, property condition, market demand, budget assumptions, and time to stabilization. They also evaluate whether the collateral can support recovery even if the original plan takes longer or costs more than expected.

Servicing capability matters as well. A lender that originates and actively services its own loans is often better positioned to monitor draws, inspect progress, enforce covenants, and address issues early. In private credit, risk management does not end at closing.

How returns are generated, and what can affect them

In this asset class, returns generally come from interest paid by borrowers, along with certain loan fees depending on the structure. That tends to make income more current and contract-based than equity real estate strategies, where distributions may depend on operating performance or asset sales.

Still, investors should avoid treating all income as equally durable. A portfolio concentrated in one asset type, one borrower profile, or one geographic pocket may carry more risk than a diversified book of short-duration loans. Duration also matters. Shorter-term loans can allow capital to recycle into new opportunities as market conditions change, but they also require a manager with consistent origination capability and disciplined deployment.

Default risk, extension risk, and collateral valuation risk remain real. If a borrower cannot execute the exit plan, a loan may require modification, additional oversight, or enforcement action. The point of senior secured lending is not that problems never occur. It is that the structure is designed to give the lender stronger tools and a better position if they do.

Senior secured real estate investment versus equity real estate

For many investors, this is the key comparison. Equity real estate can offer substantial upside, but it also carries more exposure to operating costs, leasing risk, cap rate changes, and asset-level volatility. Investors are often paid last, after debt service and other obligations are satisfied.

A senior secured real estate investment occupies a different place in the capital stack. The lender is paid before equity. That usually means lower upside than a highly successful equity deal, but it can also mean materially better downside protection. For investors focused on capital preservation and income consistency, that trade-off is often intentional.

This is especially relevant for investors using self-directed retirement capital. An old 401(k) rolled into an IRA or SDIRA may be better aligned with an income-oriented credit strategy than with speculative property equity that depends on a favorable sale environment years down the road. Suitability depends on the investor’s time horizon, liquidity needs, and overall portfolio design, but the appeal is clear – current income backed by hard assets and senior claim priority.

What to evaluate before committing capital

A disciplined review starts with the manager, not the marketing. Investors should understand whether the firm originates loans directly or buys participation interests, how it handles due diligence, what its historical loss experience looks like, and how distributions are funded. A consistent track record, conservative credit standards, and transparent reporting matter far more than headline yield alone.

It is also worth reviewing the portfolio’s composition. Are the loans first-position only, or is the strategy mixing in subordinate debt? What property types are included? How are construction risks controlled? What happens when a borrower misses milestones or requests an extension? These questions help distinguish a collateral-first lender from a yield-first lender.

For accredited investors considering private funds, alignment is another major issue. The strongest managers tend to emphasize capital preservation, moderate leverage, and repeatable process. At Mid Atlantic Secured Income Fund, that philosophy is reflected in the focus on short-term first-position mortgage lending, conservative collateral coverage, and income-oriented private credit rather than equity-style real estate speculation.

Where this strategy fits in an income portfolio

Senior secured real estate investment is not a replacement for every other income asset. It is a specialized allocation within private credit, and it comes with illiquidity and manager selection risk. But for accredited investors who want yield tied to real assets, reduced exposure to public market swings, and a structure centered on senior claim protection, it can fill an important role.

That role is often strongest when the goal is not chasing the highest possible return, but building a steadier stream of income from investments that are underwritten loan by loan. In periods when preserving principal matters as much as generating yield, structure matters. And in private real estate credit, seniority, collateral, and underwriting discipline are the parts of the structure that deserve the closest attention.

The best income strategies do not ask investors to hope for the perfect market. They ask whether the investment can still perform when conditions are merely normal, or even somewhat difficult. That is usually the right standard to apply here.