A quoted yield rarely tells the full story. When accredited investors evaluate real estate debt fund returns, the more useful question is not simply what the fund pays, but how that return is generated, what protects it, and how much variability sits beneath the headline number.

That distinction matters in a market where traditional fixed-income options can lag inflation or reset with rate cycles, while equity real estate can introduce valuation swings, leasing risk, and longer hold periods. A real estate debt fund occupies a different part of the capital stack. It is generally designed to produce income from loan interest rather than appreciation from property ownership. For investors seeking current cash flow, that difference is foundational.

What real estate debt fund returns actually come from

At a basic level, real estate debt funds earn income by lending against real property. The return to investors is usually sourced from borrower interest payments, origination fees, extension fees, and, in some structures, other loan-related income. In a well-run private credit strategy, those cash flows are generated by short-duration loans secured by tangible collateral rather than by assumptions about future property appreciation.

That is why debt fund returns tend to look different from equity real estate returns. Equity investors may target a higher total return, but much of it can depend on a future sale, rent growth, cap rate movement, or redevelopment success. Debt investors typically accept a more capped upside in exchange for a defined payment structure, a higher place in the capital stack, and a stronger focus on capital preservation.

This does not make debt inherently risk-free. It does mean the return profile is driven by underwriting discipline and loan performance, not by speculative exit assumptions.

The range of real estate debt fund returns depends on strategy

Not all real estate debt funds are built the same, so comparisons can be misleading. A fund making senior first-position bridge loans at conservative loan-to-value ratios should not be evaluated the same way as a higher-risk vehicle making subordinate debt, transitional construction loans with aggressive leverage, or loans in distressed markets.

In practice, real estate debt fund returns are shaped by several variables. The first is lien position. First-position mortgages generally offer stronger collateral protection than junior liens or preferred equity. The second is loan-to-value. Lower leverage can reduce loss severity if a borrower defaults. The third is duration. Shorter-duration lending can help a manager reprice risk more quickly when rates change and may reduce long exposure to shifting market conditions.

Property type also matters. Residential transitional assets, small balance commercial properties, and stabilized income-producing collateral each behave differently across market cycles. Geography matters as well, but only when it affects liquidity, borrower quality, and recovery prospects.

For income-focused investors, the key point is simple: a higher stated yield may reflect higher structural risk, not superior management.

How to evaluate returns beyond the advertised yield

Sophisticated investors usually start with yield, but they should not stop there. The return that matters is net return after fees, realized credit performance, and the operational ability of the manager to keep capital deployed.

A debt fund with an attractive target yield can still disappoint if it experiences cash drag, weak servicing, inconsistent underwriting, or elevated defaults. Likewise, a slightly lower-yielding fund may produce a better investor experience if it maintains stable distributions, protects principal effectively, and limits volatility.

There are several practical questions worth asking.

Gross yield versus net investor return

Some funds present a loan coupon or target return before management fees, incentive allocations, fund expenses, and reserve policies. Investors should distinguish between the economics of the loan book and the amount actually distributed or accrued to them.

Distribution rate versus total return

A fund may distribute income monthly or semi-annually, but the distribution rate is not always the same as total return. If there are realized losses, non-accrual loans, or periods of underdeployment, total return can differ meaningfully from the cash paid out.

Return stability across cycles

One year of strong performance is less informative than consistency through changing conditions. During tighter liquidity environments or rising rate periods, loan demand, borrower quality, and refinance outcomes can change quickly. A manager’s historical loss experience and continuity of distributions often reveal more than a marketing figure.

Underwriting and servicing capability

Origination is only half the equation. Funds that directly underwrite, structure, and service their loans often have better visibility into collateral, borrower behavior, extension risk, and workout execution. In private credit, returns are operational, not passive.

Risk controls are what make returns durable

For many accredited investors, especially those evaluating retirement income alternatives, the real attraction is not the possibility of the highest yield. It is the possibility of durable income with a defined risk framework.

That is where underwriting standards become central. Conservative loan-to-value ratios, first-position security, personal guarantees when appropriate, third-party valuations, title review, insurance verification, and borrower track record analysis all affect loss prevention. These may sound procedural, but they are directly connected to return quality.

According to Federal Reserve and FDIC data over multiple rate cycles, credit performance is highly sensitive to underwriting quality and asset coverage. In private real estate lending, collateral value is only useful if the lender has structured the loan correctly and can act decisively when performance deteriorates.

Investors should also pay attention to concentration risk. A fund overly exposed to one borrower, one project type, or one market can post attractive returns for a period, then face outsized pressure from a narrow problem set. Diversification inside the loan portfolio matters almost as much as diversification across an investor’s broader balance sheet.

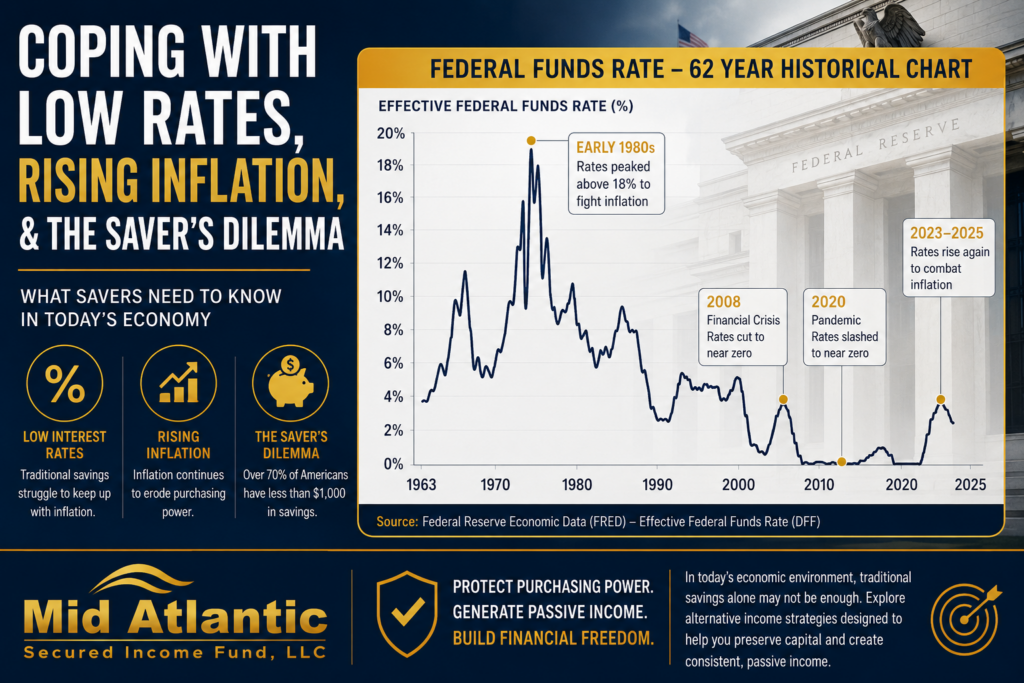

Interest rates can help and hurt debt fund returns

Rising base rates often lead investors to assume debt funds automatically benefit. Sometimes they do, especially when new loans are originated at wider spreads or floating-rate structures reprice upward. But the picture is more nuanced.

Higher rates can improve asset yields while also increasing borrower stress. Debt service costs rise. Refinance options may narrow. Property values can face pressure if cap rates expand or transaction activity slows. A manager who chases yield in that environment can expose investors to more extension risk and workout complexity.

By contrast, managers focused on short-duration lending and conservative leverage may be better positioned to preserve income quality through changing rate environments. They can adjust pricing on new originations while maintaining a margin of safety on collateral.

That trade-off is central to understanding real estate debt fund returns. Yield expansion is only beneficial if credit discipline stays intact.

Why many investors use debt funds for income, not speculation

Real estate-backed private credit tends to appeal to accredited investors who want current income without direct property ownership. That includes retirees, family offices, and self-directed IRA investors seeking an alternative to low-yield savings products, long-duration bonds, or more volatile public market exposure.

For those investors, the benefit is often structural. They are not taking on tenant management, renovation execution, leasing uncertainty, or property disposition risk in the same way an equity owner would. Instead, they are evaluating a manager’s ability to originate and protect senior secured loans.

This is also why debt funds can fit naturally into certain rollover IRA or SDIRA strategies, subject to each investor’s legal, tax, and custodial considerations. The appeal is usually predictable cash flow and asset-backed exposure, not aggressive capital appreciation.

What a disciplined return profile often looks like

The strongest private credit platforms usually emphasize consistency over headline chasing. That means focusing on income generated by real borrowers, real collateral, and repeatable underwriting processes. It often also means accepting that some high-yield opportunities should be declined.

A disciplined fund may target loans in the 65 to 75 percent loan-to-value range, maintain first-position mortgages, keep durations relatively short, and prioritize markets where collateral can be understood and liquidated if needed. Those choices can limit upside compared with more aggressive strategies, but they are often what support lower volatility and more dependable distributions.

That is particularly relevant in an environment where investors are rethinking the role of traditional fixed income. When yields in public markets move, the question is not whether private credit pays more on paper. The better question is whether the return is backed by hard assets, conservative structure, and a manager with the operational depth to protect principal.

Mid Atlantic Secured Income Fund is positioned around that discipline-first model, with an emphasis on short-term first-position mortgage loans and capital preservation ahead of return maximization.

The better question to ask before investing

Instead of asking whether a debt fund offers a high enough return, ask whether its return framework makes sense. How is the income generated? What happens when a loan extends or defaults? How much collateral coverage is built into the portfolio? How experienced is the team in both origination and recovery?

In private real estate credit, return and risk are inseparable. Investors who understand that tend to make better allocation decisions, especially when the goal is dependable income rather than market-dependent appreciation.

A well-structured debt fund should leave you with more than a yield figure. It should give you a clear explanation of how that income is earned, what stands behind it, and why the manager believes protecting principal comes first.