The Evolution of Modern Wealth Management

Wealth management has evolved far beyond traditional stock-and-bond portfolio construction. In today’s environment of persistent inflation, elevated interest-rate volatility, geopolitical uncertainty, and rapidly changing capital markets, affluent investors are increasingly seeking strategies that prioritize:

- capital preservation,

- income generation,

- downside protection,

- tax efficiency,

- diversification,

- and long-term financial resilience.

Modern wealth management is no longer solely about accumulating wealth. Increasingly, it is about protecting purchasing power, generating sustainable income, mitigating volatility, and preserving financial flexibility across generations.

This shift has accelerated dramatically since 2020 as investors faced:

- inflation spikes not seen in decades,

- banking instability,

- bond market drawdowns,

- heightened equity volatility,

- and growing concerns surrounding retirement sustainability.

As a result, many sophisticated investors are expanding beyond traditional public-market exposure and exploring alternative investment strategies such as:

- private credit,

- real estate-backed lending,

- private debt funds,

- self-directed IRA investing,

- and institutional-grade income-focused strategies.

For investors focused on long-term financial independence and wealth preservation, understanding modern wealth management has become more important than ever.

What Is Wealth Management?

Direct Answer

Wealth management is a comprehensive financial strategy focused on growing, preserving, protecting, and transferring wealth through diversified investment planning, risk management, tax efficiency, retirement strategies, estate planning, and income generation.

Unlike basic financial planning, wealth management typically integrates:

- investment management,

- retirement income planning,

- tax optimization,

- alternative investments,

- estate and legacy planning,

- and long-term capital preservation.

Sophisticated wealth management strategies increasingly incorporate private-market investments and alternative assets alongside traditional stocks and bonds.

Why Wealth Management Matters More in Today’s Economy

The economic environment facing investors today is materially different from prior decades.

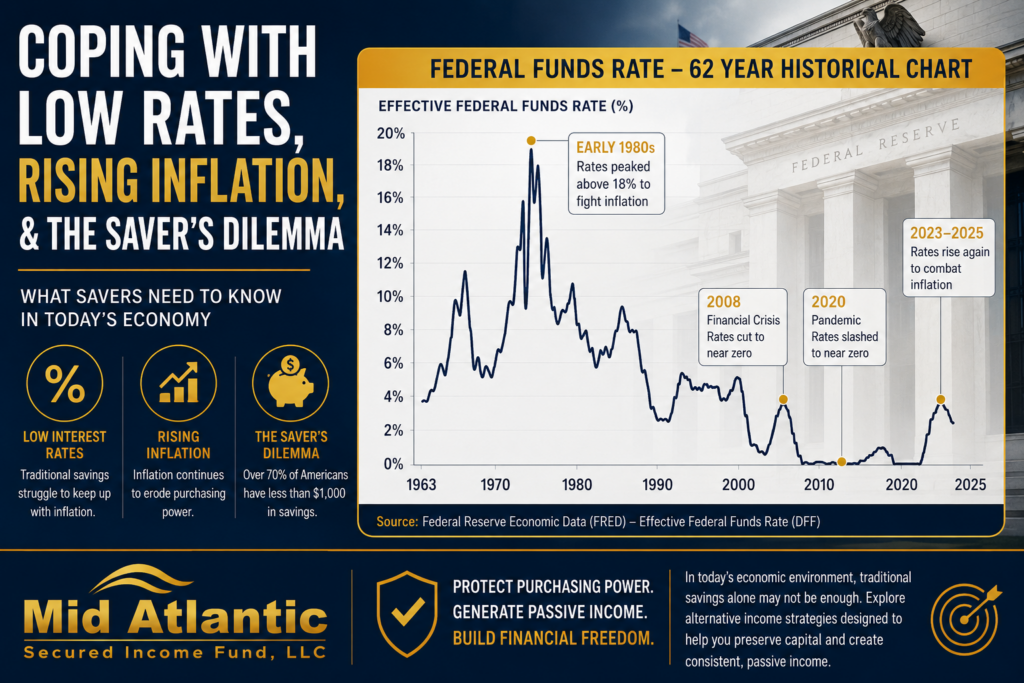

Inflation Has Changed Retirement Planning

According to the U.S. Bureau of Labor Statistics, inflation reached multi-decade highs following the pandemic-era economic cycle, significantly impacting purchasing power.

Even moderate inflation compounds dramatically over time.

For example:

- At 3% annual inflation, purchasing power declines roughly 50% over 24 years.

- Healthcare, insurance, and housing costs continue rising faster than headline inflation in many regions.

- Retirees relying solely on fixed-income instruments may face growing income pressure.

This has increased demand for:

- income-producing assets,

- inflation-resistant investments,

- and strategies with stronger yield potential.

The Traditional 60/40 Portfolio Has Faced Challenges

For decades, investors relied heavily on the classic:

- 60% equities,

- 40% bonds

portfolio structure.

However, recent years exposed vulnerabilities in this model.

Historically, bonds often served as a stabilizer during equity downturns. Yet rising interest rates caused simultaneous declines across both equities and fixed income during periods of market stress.

This has pushed many institutional allocators toward:

- private credit,

- infrastructure,

- real estate debt,

- alternative income strategies,

- and non-correlated assets.

According to Preqin and BlackRock research, private-market allocations among institutional investors continue increasing as firms seek diversification and more stable cash-flow profiles.

The Rise of Alternative Investments in Wealth Management

What Are Alternative Investments?

Alternative investments are assets outside traditional publicly traded stocks and bonds.

Examples include:

- private credit,

- real estate debt,

- private equity,

- hedge funds,

- infrastructure,

- private real estate,

- and asset-backed lending.

Alternative assets are increasingly used by sophisticated investors seeking:

- diversification,

- lower public-market correlation,

- enhanced yield potential,

- and more stable income streams.

Why High-Net-Worth Investors Are Increasingly Using Private Credit

Private credit has emerged as one of the fastest-growing segments within alternative investing.

Private credit generally refers to non-bank lending strategies where investors provide capital directly to businesses, real estate projects, or borrowers outside traditional public bond markets.

Common forms include:

- senior secured lending,

- bridge lending,

- real estate-backed debt,

- direct lending,

- asset-backed financing,

- and private debt funds.

Institutional investors are increasingly attracted to private credit because of:

- contractual income,

- collateral-backed structures,

- floating-rate characteristics,

- and historically lower volatility relative to equities.

According to major institutional research firms including BlackRock and Preqin, global private credit assets under management have expanded significantly over the last decade.

Understanding Asset-Backed Lending

What Is Asset-Backed Lending?

Asset-backed lending is a lending strategy where loans are secured by tangible collateral.

Collateral may include:

- real estate,

- receivables,

- equipment,

- inventory,

- or other hard assets.

In many private credit strategies, downside protection begins with collateral positioning.

This differs from unsecured lending structures where recovery options may be more limited during economic stress.

Why Sophisticated Investors Value Senior Secured Lending

Senior secured lending occupies a higher priority position within a borrower’s capital stack.

This means senior lenders generally have stronger claims on collateral and repayment priority compared to subordinate lenders or equity investors.

For income-focused investors, senior secured structures may offer:

- enhanced risk management,

- contractual cash flow,

- reduced equity market exposure,

- and potential downside mitigation.

These characteristics have become increasingly attractive in volatile macroeconomic environments.

Wealth Preservation vs Wealth Accumulation

Wealth Accumulation

Wealth accumulation focuses primarily on maximizing long-term growth.

This phase often emphasizes:

- equities,

- higher-growth strategies,

- and aggressive capital appreciation.

Younger investors frequently prioritize this stage.

Wealth Preservation

Wealth preservation becomes increasingly important later in life or during periods of economic uncertainty.

Goals often shift toward:

- protecting principal,

- generating stable income,

- reducing volatility,

- and maintaining purchasing power.

This is where many affluent investors begin incorporating:

- alternative income strategies,

- real estate-backed investments,

- and private credit exposure.

Passive Income and Wealth Management

What Is Passive Income?

Passive income refers to recurring income generated from investments requiring limited ongoing active involvement.

Examples include:

- dividends,

- rental income,

- interest payments,

- and private credit distributions.

For retirees and income-focused investors, passive income strategies can play a major role in financial independence and retirement sustainability.

Why Passive Income Matters in Retirement

One of the largest retirement risks is sequence-of-returns risk — the danger that market downturns early in retirement impair portfolio longevity.

Many retirees increasingly seek:

- contractual income,

- lower volatility,

- and diversified income streams.

This has contributed to growing interest in:

- private lending,

- real estate debt funds,

- and asset-backed income strategies.

Real Estate-Backed Debt Funds Explained

What Is a Real Estate Debt Fund?

A real estate debt fund pools investor capital to provide loans secured by real estate assets.

These may include:

- residential projects,

- multifamily developments,

- bridge loans,

- stabilized commercial assets,

- and construction financing.

Unlike equity real estate investing, debt-focused strategies primarily generate returns through interest income rather than property appreciation alone.

Why Investors Use Real Estate Debt Strategies

Potential advantages include:

- recurring income generation,

- collateral-backed structures,

- reduced correlation to public equities,

- and shorter-duration investment profiles.

In many cases, real estate debt investors prioritize:

- consistent cash flow,

- conservative underwriting,

- and capital preservation.

The Role of Diversification in Wealth Management

Why Diversification Still Matters

Diversification remains one of the foundational principles of sophisticated wealth management.

However, diversification today increasingly extends beyond:

- stocks,

- bonds,

- and mutual funds.

Modern diversification often includes:

- private credit,

- real estate debt,

- alternative income strategies,

- and private-market exposure.

The objective is not simply increasing the number of holdings — it is reducing concentration risk and improving portfolio resilience across varying economic conditions.

Inflation, Interest Rates & Wealth Management

How Inflation Impacts Investors

Inflation erodes purchasing power over time.

For retirees, this can materially impact:

- lifestyle sustainability,

- retirement income sufficiency,

- and healthcare affordability.

Investors increasingly seek strategies capable of generating:

- higher income potential,

- inflation resilience,

- and stable cash-flow characteristics.

How Higher Interest Rates Changed Fixed Income

Rising interest rates have altered the fixed-income landscape.

Traditional long-duration bonds experienced significant price declines during recent rate cycles.

Meanwhile, many private credit strategies benefited from:

- shorter durations,

- floating-rate structures,

- and enhanced income generation.

This has led many sophisticated investors to reevaluate traditional fixed-income allocations.

Wealth Management and Self-Directed IRAs

What Is an SDIRA?

A Self-Directed IRA (SDIRA) allows investors to hold alternative assets within retirement accounts.

Potential investments may include:

- private credit,

- real estate debt funds,

- private placements,

- and other non-traditional assets.

Many investors use SDIRAs to diversify retirement portfolios beyond publicly traded securities.

Why Investors Use Alternative Assets in Retirement Accounts

Sophisticated investors may seek:

- tax-advantaged income generation,

- alternative diversification,

- and inflation-resistant strategies.

However, SDIRA investing requires careful due diligence, compliance awareness, and understanding of prohibited transaction rules.

Wealth Management in an AI-Driven Economy

Artificial intelligence is reshaping financial services rapidly.

AI-driven analytics now influence:

- portfolio construction,

- risk management,

- fraud detection,

- macroeconomic forecasting,

- and investor personalization.

However, despite technological advances, core wealth-management principles remain unchanged:

- disciplined diversification,

- risk management,

- long-term planning,

- and prudent capital allocation.

Why Financial Education Matters

One of the greatest threats to long-term wealth is not necessarily market volatility — it is poor financial decision-making.

Financial literacy affects:

- saving habits,

- debt management,

- retirement planning,

- investment behavior,

- and long-term financial resilience.

Sophisticated investors often prioritize ongoing financial education because informed decision-making compounds over time.

Wealth Management Is About More Than Returns

Many investors mistakenly define wealth management purely through performance metrics.

In reality, sophisticated wealth management also focuses on:

- risk-adjusted outcomes,

- stability,

- liquidity planning,

- tax efficiency,

- family legacy,

- and long-term flexibility.

Successful wealth management often means balancing growth with protection.

How Sophisticated Investors Think Differently

Experienced investors often focus less on chasing maximum returns and more on:

- preserving capital,

- controlling downside exposure,

- maintaining liquidity,

- generating durable income,

- and building long-term resilience.

This mindset becomes especially important during uncertain economic periods.

The Growing Importance of Private Markets

Private markets continue attracting institutional capital globally.

According to institutional research from firms such as BlackRock, Preqin, and McKinsey:

- private credit continues growing rapidly,

- alternative allocations are increasing,

- and institutional investors increasingly seek differentiated income sources.

This trend reflects broader changes in modern portfolio construction.

Why Geographic Trends Matter

Regional economic growth plays a major role in investment opportunities.

The Southeast United States — particularly Atlanta — continues benefiting from:

- population growth,

- business migration,

- infrastructure investment,

- and housing demand.

These macroeconomic tailwinds can influence:

- real estate demand,

- lending activity,

- and broader economic expansion.

Understanding Risk in Wealth Management

Are Alternative Investments Risk-Free?

No investment is risk-free.

Alternative investments carry unique considerations including:

- illiquidity,

- underwriting risk,

- economic sensitivity,

- borrower performance,

- and market conditions.

Investors should carefully evaluate:

- investment structures,

- collateral quality,

- manager experience,

- and overall portfolio fit.

How Sophisticated Investors Evaluate Risk

Institutional-style investors often prioritize:

- collateral positioning,

- loan-to-value ratios,

- underwriting discipline,

- sponsor quality,

- and cash-flow durability.

Risk management frequently matters more than maximizing headline returns.

The Importance of Income Consistency

During periods of market volatility, income consistency becomes increasingly valuable.

Many investors seek investments capable of generating:

- recurring cash flow,

- contractual income,

- and lower public-market sensitivity.

This helps support:

- retirement sustainability,

- lifestyle planning,

- and long-term financial confidence.

Building a Long-Term Wealth Strategy

Key Components of Sophisticated Wealth Management

A comprehensive wealth-management framework often includes:

1. Diversification

Reducing concentration risk across asset classes.

2. Income Planning

Generating sustainable cash flow.

3. Inflation Protection

Maintaining purchasing power.

4. Risk Management

Protecting capital during downturns.

5. Tax Efficiency

Structuring investments thoughtfully.

6. Estate Planning

Preserving wealth across generations.

7. Alternative Investments

Enhancing diversification and income potential.

Why Wealth Preservation Becomes Increasingly Important Over Time

As investors near retirement or enter income-distribution phases, wealth preservation often becomes more important than aggressive growth.

This may shift portfolio priorities toward:

- income-focused strategies,

- private credit,

- asset-backed investments,

- and lower-volatility allocations.

Institutional Thinking for Individual Investors

Historically, many alternative investments were primarily accessible to large institutions.

Today, accredited investors increasingly seek institutional-style strategies focused on:

- income generation,

- downside protection,

- and diversification.

This trend continues reshaping modern wealth management.

Final Thoughts

The future of wealth management is becoming increasingly:

- diversified,

- income-focused,

- alternative-oriented,

- and risk-aware.

Sophisticated investors are recognizing that long-term financial success is not solely about chasing growth. Increasingly, it is about creating resilient portfolios capable of navigating changing economic cycles while preserving purchasing power and generating sustainable income.

In a world shaped by inflation, volatility, demographic shifts, and evolving markets, disciplined wealth management remains one of the most important foundations for long-term financial stability and freedom.

FAQ Section

What is wealth management?

Wealth management is a comprehensive financial strategy focused on growing, preserving, protecting, and transferring wealth through investment management, retirement planning, tax strategies, estate planning, and risk management.

Why are affluent investors using private credit?

Many affluent investors use private credit because it may provide contractual income, diversification benefits, asset-backed structures, and lower correlation to public equity markets.

What are alternative investments?

Alternative investments are assets outside traditional stocks and bonds, including private credit, real estate debt, private equity, infrastructure, and hedge funds.

How do real estate debt funds work?

Real estate debt funds pool investor capital to provide loans secured by real estate assets. Investors generally earn returns primarily through interest income generated by those loans.

Are private credit investments safer than stocks?

Private credit investments may experience lower volatility than equities in certain environments due to contractual income and collateral-backed structures. However, all investments involve risk and potential loss of principal.

What is passive income investing?

Passive income investing focuses on generating recurring income streams through investments such as dividends, interest payments, rental income, or private lending distributions.

What is an SDIRA?

A Self-Directed IRA allows investors to hold alternative assets within retirement accounts, including private credit, private placements, and certain real estate-related investments.

Why does diversification matter?

Diversification helps reduce concentration risk and may improve long-term portfolio resilience across changing market environments.