Building Resilient Wealth Through Diversification, Private Credit & Income-Focused Investing

For decades, strategic investment planning largely revolved around a familiar formula: public equities, investment-grade bonds, and broad market diversification. But the investment environment entering 2026 looks materially different than the one many investors built their portfolios around during the ultra-low interest rate era.

Persistent inflation pressures, elevated market volatility, shifting Federal Reserve policy, geopolitical uncertainty, and changing retirement demographics are reshaping how sophisticated investors think about long-term wealth preservation and income generation.

As a result, accredited investors, family offices, and institutional allocators are increasingly expanding beyond traditional 60/40 portfolio frameworks toward more diversified, income-oriented investment strategies that incorporate private credit, real estate-backed lending, alternative income vehicles, and non-correlated assets.

Strategic investment planning today is no longer simply about maximizing returns. Increasingly, it is about balancing:

- capital preservation,

- downside management,

- inflation resilience,

- tax efficiency,

- predictable income,

- liquidity considerations,

- and long-term portfolio durability.

This evolution is driving growing interest in alternative fixed-income strategies and secured lending investments that can potentially provide recurring income streams while maintaining a more conservative risk posture than many speculative growth assets.

What Is Strategic Investment Planning?

Direct Answer

Strategic investment planning is the process of building, allocating, managing, and periodically adjusting an investment portfolio based on an investor’s long-term financial goals, risk tolerance, liquidity needs, tax considerations, and market conditions.

A strategic investment plan typically includes:

- portfolio diversification,

- asset allocation,

- risk management,

- income generation,

- tax optimization,

- retirement planning,

- and long-term capital preservation strategies.

Sophisticated investment planning often incorporates both traditional and alternative asset classes to improve portfolio resilience across varying economic environments.

Why Strategic Investment Planning Matters More in 2026

The macroeconomic environment has fundamentally changed from the decade following the Global Financial Crisis.

Between 2009 and 2021, many investors benefited from:

- historically low interest rates,

- abundant liquidity,

- strong equity market expansion,

- and suppressed volatility.

However, several structural shifts are changing the investment landscape:

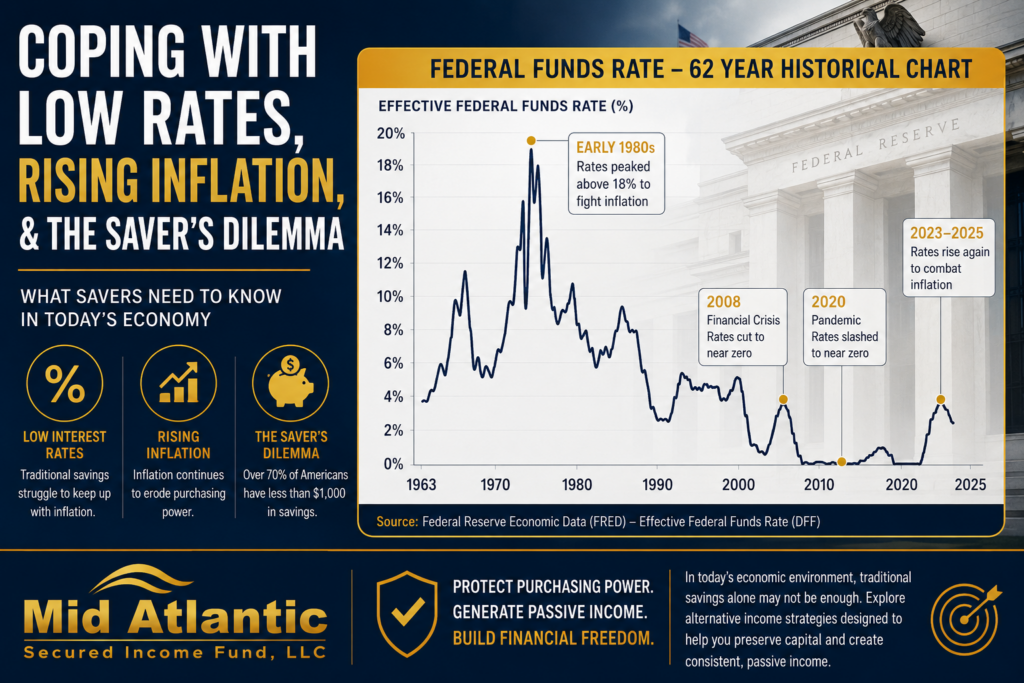

1. Higher-for-Longer Interest Rates

The Federal Reserve’s tightening cycle significantly altered fixed income dynamics. While higher rates have improved bond yields compared to prior years, they have also introduced:

- duration risk,

- refinancing pressure,

- commercial real estate stress,

- and elevated market uncertainty.

Investors are increasingly seeking income strategies less dependent on public market volatility.

2. Inflation Remains a Long-Term Concern

According to U.S. Bureau of Labor Statistics data, inflation surged to multi-decade highs during 2022–2023 and, while moderating, continues to influence consumer costs, wage pressures, and long-term purchasing power considerations.

This has made real return preservation increasingly important for retirees and wealth-focused investors.

3. The Retirement Wave Is Accelerating

The U.S. Census Bureau projects continued expansion of retirement-age demographics through the 2030s as Baby Boomers transition into income-focused portfolio stages.

This demographic shift is increasing demand for:

- recurring cash flow,

- lower-volatility investments,

- capital preservation strategies,

- and alternative income-oriented assets.

4. Public Market Volatility Has Increased

The S&P 500 experienced significant volatility throughout 2020–2024 due to:

- inflation uncertainty,

- banking sector stress,

- geopolitical instability,

- AI-driven market concentration,

- and rapidly shifting monetary policy.

As a result, investors are increasingly exploring portfolio diversification strategies that extend beyond public equities and traditional bonds.

The Core Pillars of Strategic Investment Planning

Effective strategic investment planning generally rests on five foundational pillars.

1. Portfolio Diversification

What Is Portfolio Diversification?

Portfolio diversification involves spreading investments across multiple asset classes, industries, geographies, and risk profiles to reduce concentration risk.

The objective is not simply maximizing returns, but improving risk-adjusted outcomes over time.

Why Diversification Matters

Different asset classes perform differently under varying economic conditions.

For example:

|

Asset Class |

Potential Strength |

|---|---|

|

Public Equities |

Long-term growth |

|

Investment-Grade Bonds |

Stability & income |

|

Private Credit |

Yield & lower public correlation |

|

Real Estate |

Inflation hedge |

|

Cash & Treasuries |

Liquidity |

|

Alternative Investments |

Portfolio diversification |

According to research from BlackRock and JP Morgan Asset Management, diversified portfolios historically experience lower volatility and improved long-term consistency versus concentrated allocations.

2. Asset Allocation

Asset allocation refers to determining how capital is distributed among investment categories.

This is often considered one of the most important drivers of long-term portfolio outcomes.

A strategic allocation may include:

- equities,

- fixed income,

- private credit,

- real estate debt,

- infrastructure,

- cash reserves,

- and alternative income investments.

Sophisticated investors increasingly utilize alternative investments to reduce reliance on traditional stock market performance.

3. Income Generation

Historically, many portfolios relied heavily on bonds for income.

However, prolonged periods of low rates forced many investors to seek alternative income-producing investments.

Today, investors are increasingly evaluating:

- private credit,

- secured lending,

- real estate-backed debt,

- infrastructure income,

- and alternative yield-oriented investments.

The objective is often to generate recurring cash flow while maintaining disciplined underwriting and risk management standards.

4. Risk Management

Strategic investment planning is fundamentally about risk management.

This includes evaluating:

- market risk,

- credit risk,

- liquidity risk,

- inflation risk,

- concentration risk,

- and duration risk.

Sophisticated investors increasingly focus on downside mitigation rather than solely maximizing upside.

5. Tax Efficiency

Tax-aware investing can materially improve after-tax outcomes.

Common tax-efficient strategies include:

- tax-deferred retirement accounts,

- Roth conversions,

- tax-loss harvesting,

- municipal bonds,

- SDIRA structures,

- and long-term capital gains planning.

For accredited investors, self-directed IRAs (SDIRAs) have become increasingly popular vehicles for accessing alternative investments with potential tax advantages.

Why Accredited Investors Are Expanding Into Private Credit

Private credit has emerged as one of the fastest-growing segments of alternative investing.

According to Preqin, global private credit assets under management exceeded $1.7 trillion in recent years and continue expanding rapidly.

Several factors are driving this trend.

Reduced Correlation to Public Markets

Unlike publicly traded equities, many private credit investments are less directly tied to daily market sentiment and stock market volatility.

This may improve diversification within broader portfolios.

Income-Oriented Structures

Many private credit investments are designed around recurring interest income rather than speculative capital appreciation.

This appeals to:

- retirees,

- family offices,

- income-focused investors,

- and wealth preservation strategies.

Asset-Backed Structures

Certain private credit strategies utilize:

- first-position liens,

- real estate collateral,

- secured lending agreements,

- and conservative underwriting frameworks.

This can provide an additional layer of downside-oriented structuring compared to unsecured investments.

Strategic Investment Planning and Retirement Income

Why Retirement Planning Has Changed

Retirement planning has evolved dramatically over the past two decades.

Traditional pension systems have declined while:

- life expectancy has increased,

- healthcare costs have risen,

- and market volatility has intensified.

As a result, many investors are shifting from accumulation-focused investing toward income-focused portfolio construction.

Key Retirement Planning Considerations

Modern retirement investment planning often prioritizes:

- reliable income,

- reduced volatility,

- inflation resilience,

- tax efficiency,

- liquidity management,

- and sequence-of-returns risk mitigation.

Sequence-of-Returns Risk

One major challenge retirees face is experiencing significant portfolio losses early in retirement.

Large drawdowns during withdrawal periods can materially impact long-term sustainability.

This is one reason many investors incorporate diversified income-producing investments alongside traditional equity exposure.

Are Debt Funds Safer Than Stocks?

Direct Answer

Debt funds and private credit investments are not risk-free, but they may exhibit lower volatility and different risk characteristics compared to equities.

In many secured lending structures:

- investors occupy higher positions in the capital stack,

- loans may be backed by collateral,

- and income generation is contractually structured through interest payments.

However, risks still include:

- borrower default,

- illiquidity,

- economic downturns,

- underwriting quality,

- and real estate market stress.

Risk levels vary significantly depending on the investment strategy and manager discipline.

Strategic Investment Planning for Family Offices

Family offices increasingly emphasize:

- wealth preservation,

- intergenerational planning,

- downside protection,

- and diversified income streams.

Institutional allocators are increasingly allocating capital toward:

- private credit,

- infrastructure,

- real estate debt,

- and alternative fixed-income strategies.

According to Goldman Sachs and McKinsey research, family offices continue increasing exposure to alternatives due to concerns surrounding public market concentration and long-term inflation risks.

The Role of Real Estate-Backed Lending

Real estate-backed lending strategies have gained increased attention in recent years because they combine:

- income generation,

- collateralization,

- and potential inflation resilience.

These strategies may include:

- bridge lending,

- construction financing,

- stabilized property lending,

- acquisition financing,

- and senior secured debt structures.

Many investors view real estate debt as a middle ground between traditional bonds and direct real estate ownership.

How Strategic Investment Planning Supports Wealth Preservation

Wealth preservation is often overlooked during strong bull markets.

However, preserving capital during economic downturns can be just as important as generating returns.

Sophisticated wealth preservation strategies often emphasize:

- diversification,

- downside protection,

- disciplined underwriting,

- liquidity planning,

- and risk-adjusted income generation.

Common Mistakes Investors Make

1. Overconcentration

Concentrated positions may create outsized risk exposure.

2. Chasing Yield Without Understanding Risk

Higher yield frequently corresponds with higher risk.

Investors should evaluate:

- collateral quality,

- underwriting standards,

- borrower strength,

- liquidity constraints,

- and manager experience.

3. Ignoring Liquidity Needs

Alternative investments may have longer holding periods and reduced liquidity versus publicly traded securities.

4. Failing to Rebalance

Strategic investment planning requires periodic reassessment and portfolio adjustments.

Strategic Investment Planning in an AI-Driven Economy

Artificial intelligence is reshaping:

- labor markets,

- productivity,

- capital flows,

- and market concentration.

This has created significant growth opportunities but also increased concentration risks within public markets.

Many investors are responding by diversifying beyond mega-cap technology exposure into:

- real assets,

- private credit,

- and alternative income-oriented strategies.

Why Income-Focused Investing Is Gaining Momentum

Income-focused investing is increasingly attractive because:

- interest rates remain elevated,

- retirees need predictable cash flow,

- inflation pressures persist,

- and volatility remains elevated.

Many investors are prioritizing:

- consistency,

- resilience,

- and capital discipline over speculative growth.

Strategic Investment Planning and Self-Directed IRAs (SDIRAs)

Self-directed IRAs allow eligible investors to access broader alternative investment opportunities beyond traditional stocks and mutual funds.

This may include:

- private credit,

- real estate debt,

- private real estate,

- and alternative income investments.

SDIRAs have become increasingly popular among accredited investors seeking:

- diversification,

- tax-advantaged growth,

- and income-oriented retirement strategies.

How Accredited Investors Use Strategic Investment Planning

Sophisticated investors often combine:

- public market exposure,

- private credit,

- real estate-backed lending,

- tax-aware planning,

- and alternative investments.

The objective is often to create:

- resilient portfolios,

- diversified income streams,

- and improved downside management across economic cycles.

Institutional Trends Shaping 2026

Several major institutional trends are influencing investment planning decisions:

Growing Allocation to Alternatives

According to BlackRock and Preqin research, institutional investors continue increasing allocations toward alternative assets.

Increased Demand for Income

Higher living costs and retirement pressures are increasing demand for recurring cash flow investments.

Greater Focus on Risk Management

Investors increasingly prioritize resilience and downside mitigation over speculative return chasing.

Strategic Investment Planning Is Ultimately About Alignment

The best investment strategy is not universal.

Effective strategic investment planning aligns investments with:

- financial objectives,

- time horizon,

- risk tolerance,

- liquidity needs,

- and long-term lifestyle goals.

For some investors, this may mean prioritizing growth.

For others, it may emphasize:

- stability,

- recurring income,

- wealth preservation,

- and diversification.

Conclusion

Strategic investment planning has evolved significantly in recent years.

The traditional portfolio frameworks that dominated prior decades are increasingly being supplemented by:

- alternative investments,

- private credit,

- secured lending strategies,

- and diversified income-producing assets.

Sophisticated investors are increasingly focused on:

- resilience,

- risk-adjusted returns,

- downside awareness,

- and long-term portfolio durability.

As economic conditions continue evolving, strategic investment planning remains one of the most important tools for preserving wealth, generating income, and navigating uncertainty across market cycles.

For accredited investors exploring alternative income-oriented strategies, understanding portfolio construction, diversification, risk management, and disciplined underwriting has become increasingly important in building long-term financial resilience.

FAQ Section

What is strategic investment planning?

Strategic investment planning is the process of designing and managing a long-term investment portfolio based on financial goals, risk tolerance, income needs, tax considerations, and market conditions.

Why is diversification important in investing?

Diversification helps reduce concentration risk by spreading investments across multiple asset classes and investment types.

What are alternative investments?

Alternative investments include assets outside traditional stocks and bonds, such as private credit, real estate debt, infrastructure, and private equity.

What is private credit investing?

Private credit investing involves lending capital directly to businesses or borrowers outside traditional public bond markets.

Are secured income investments safer?

Secured investments may offer additional downside protections through collateral structures, but all investments involve risk, including loss of principal.

Why are family offices investing more in private credit?

Family offices increasingly seek diversified income streams, lower public market correlation, and alternative yield opportunities.

What role do SDIRAs play in investment planning?

Self-directed IRAs allow eligible investors to access alternative investments while maintaining certain tax advantages associated with retirement accounts.