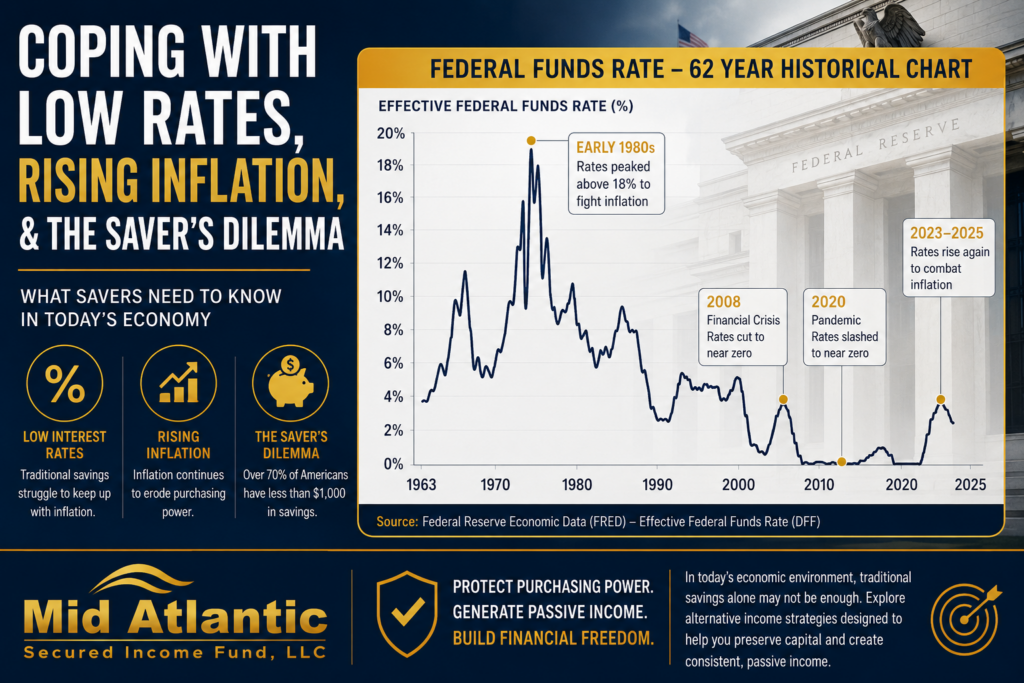

A rollover decision gets more consequential the moment your 401(k) stops feeling like a growth account and starts feeling like a future income source. That is why rollover 401k to IRA investment options deserve more than a quick comparison of fees and fund menus. The right choice affects liquidity, tax treatment, portfolio volatility, and how much control you actually have over retirement capital.

For many investors, the core question is not simply whether to move an old plan into an IRA. It is what kind of IRA structure and investment mix better supports the next stage of wealth management. A former employer plan may offer limited investment choices and little flexibility. An IRA often expands the field, but more choice also means more responsibility around underwriting, diversification, and risk control.

Expanding Your Investment Opportunity Set After a 401(k) Rollover

A typical 401(k) menu is built around public market securities such as mutual funds, target-date funds, and bond funds. That framework can work well during accumulation years, especially when payroll contributions and employer matches are still in play. Once the account becomes dormant, however, investors often begin to evaluate whether the menu still aligns with their income goals and risk tolerance.

Rolling to an IRA can broaden investment access. In a conventional IRA held at a brokerage firm, that usually means a wider range of ETFs, mutual funds, individual bonds, and CDs. In a self-directed IRA, the universe can extend further into certain alternative assets, including private real estate-backed debt, subject to custodian rules and IRS requirements.

That expanded access is the appeal, but it also introduces trade-offs. More flexibility may improve portfolio design, yet it can also create due diligence risk if an investor moves into assets they do not fully understand. Sophisticated investors generally benefit most when the rollover decision is paired with a clear mandate – income generation, principal stability, inflation resilience, or some combination of the three.

The main categories of rollover 401k to IRA investment options

The simplest path is a traditional rollover IRA invested in public market securities. That route usually preserves tax-deferred status and can reduce the administrative friction of managing an old employer plan. Investors who prioritize daily liquidity and broad diversification often remain in this lane, using a mix of investment-grade fixed income, equity income strategies, and cash equivalents.

The challenge is that traditional fixed-income products do not always deliver the level of current income retirees expect, especially after inflation and taxes are considered. Federal Reserve policy, credit spreads, and rate sensitivity can all affect outcomes. Bond funds may provide income, but they can also introduce mark-to-market volatility when rates rise.

A second category is the self-directed IRA, which is relevant for investors who want access to private market assets. This structure can open the door to private credit, private real estate debt, and other alternatives that are not typically available in standard employer plans. For accredited investors focused on cash flow, this is often where the conversation becomes more practical. The issue is not novelty. It is whether the asset is backed by collateral, how it is underwritten, and how the manager controls downside risk.

Public market income options inside an IRA

Traditional IRAs are often populated with dividend-focused equity funds, bond ladders, Treasury exposure, money market instruments, and diversified allocation models. Each has a role, but each behaves differently under stress.

Dividend strategies can produce income, yet the underlying securities remain equities. That means the income stream is tied to companies whose stock prices can reprice sharply during market drawdowns. Bond funds may look defensive on paper, but duration risk and credit risk still matter. Money market funds and short-term CDs can provide stability, though their yields may lag inflation over longer periods.

For investors nearing or in retirement, the question is rarely yield alone. It is the interaction between income and principal volatility. A portfolio that produces acceptable cash flow but loses meaningful value in a downturn may force difficult timing decisions. That is one reason some rollover IRA investors look beyond conventional stock-and-bond allocations.

Where self-directed IRAs fit

A self-directed IRA can be appropriate when the investor wants greater control over asset selection and understands the operational rules. The structure itself is not the investment. It is simply the vehicle that allows the account to hold eligible alternative assets through a qualified custodian.

Within that framework, some investors allocate to private real estate-backed credit rather than direct property ownership. That distinction matters. Owning a property inside an IRA can involve maintenance complexity, valuation questions, and cash management issues. By contrast, private mortgage lending or participation in a real estate-backed private credit fund may offer exposure to real estate collateral without the day-to-day burden of managing a property.

This is where underwriting discipline becomes central. Not all private debt is created equal. Investors should distinguish between first-position loans and subordinate debt, between conservative loan-to-value ratios and aggressive leverage, and between short-duration lending and capital that may be tied up for longer than expected.

Evaluating real estate-backed private credit in a rollover IRA

For accredited investors seeking income, private credit backed by real estate can serve a different purpose than public bonds or REITs. The return profile is generally driven by contractual loan payments rather than public market sentiment. When structured conservatively, the focus shifts toward collateral quality, borrower strength, debt position, and duration.

A prudent review starts with the loan book. Are loans secured by residential or commercial real estate? Is the manager originating first-position mortgages or participating in junior tranches? What are the typical loan-to-value parameters? A disciplined lender operating in the 65% to 75% range is managing risk differently than one stretching leverage to pursue headline returns.

Investors should also assess distribution history, loss history, servicing capability, and how the manager handles workouts if a borrower underperforms. In private credit, process is not a minor detail. Origination, funding, servicing, and enforcement all affect capital preservation.

For the right investor, this type of exposure may complement a rollover IRA by providing current income potential with less direct correlation to public equities. But the trade-off is liquidity. Private funds and private notes are not the same as exchange-traded securities. Capital may be committed for a period of time, and valuations are typically not updated by the market every second. Some investors view that as a feature, others as a constraint.

What to weigh before moving retirement assets

The best rollover decision depends on what problem you are trying to solve. If the issue is excessive fees in an old 401(k), a standard IRA may address it. If the issue is limited income and high sensitivity to public market volatility, broader IRA investment options may be more relevant.

Before executing a rollover, investors should consider investment objective, liquidity needs, time horizon, and concentration limits. A retiree drawing current income may prioritize consistency and downside protection differently than an executive with ten more years before distributions begin. Likewise, an investor using a self-directed IRA should be comfortable with private placement documents, subscription processes, and custodian administration.

It is also worth reviewing plan-specific factors. Some 401(k) plans offer institutional share classes or creditor protections that may be advantageous in certain circumstances. Others are simply limited menus with little flexibility. The account type matters, but the quality of available investments matters just as much.

A disciplined framework for choosing among options

A useful way to assess rollover 401k to IRA investment options is to separate them into three buckets: liquidity, income, and security. Public securities generally offer strong liquidity. Traditional fixed income may offer moderate income, but pricing can be sensitive to rate changes. Real estate-backed private credit may offer stronger current income characteristics for some accredited investors, but with reduced liquidity and a greater need for manager-level due diligence.

That does not mean one category is universally better. It means each serves a different role. Many sophisticated investors build around that reality instead of chasing a single solution. They may keep liquid reserves in conventional instruments while allocating a measured portion of retirement capital to asset-backed private credit strategies designed to emphasize collateral protection and recurring distributions.

That measured approach is often the more durable one. At Mid Atlantic Secured Income Fund, the emphasis on first-position lending, conservative underwriting, and capital preservation reflects a broader principle that applies well beyond any single fund: retirement assets usually benefit more from discipline than from reach.

If you are evaluating an old 401(k), the real opportunity is not merely moving the account. It is using the rollover as a chance to align retirement capital with the income, risk controls, and asset backing you actually want for the years ahead.