A fully leased rental property can still produce a bad investor outcome if a roof fails, taxes rise, or a refinance lands at the wrong point in the rate cycle. That is why many accredited investors researching passive income investments real estate are no longer looking only at ownership. They are looking at the capital stack, asking a more disciplined question: where can income come from, and what is securing it?

For investors who want cash flow tied to real assets without taking on tenant issues, renovation risk, or property-level operating headaches, real estate-backed private credit deserves serious attention. It sits in a different part of the market than direct property ownership. Instead of buying and managing the property, the investor participates in loans secured by real estate collateral, often with defined terms, contractual interest payments, and a senior position in the capital structure.

Why passive income investments real estate look different now

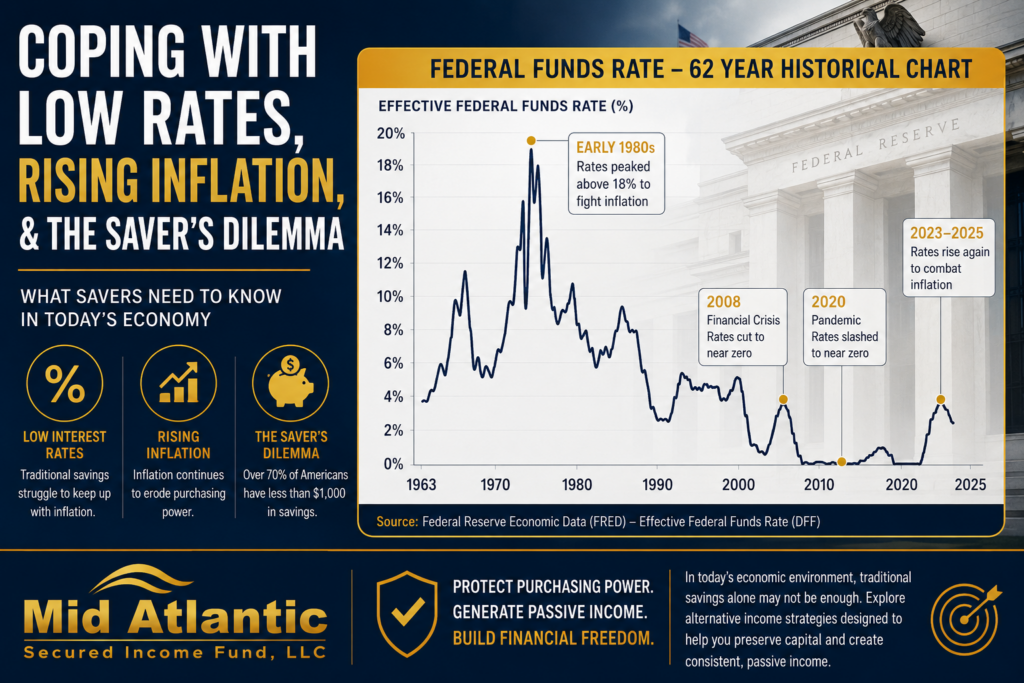

The appeal of real estate as an income asset is not new. What has changed is the backdrop. Public fixed-income products have faced periods of low real yield, while public equities have introduced more volatility than many income-focused investors want near or during retirement. At the same time, higher financing costs and tighter bank credit have expanded the opportunity set for private lenders that can underwrite conservatively and move with conviction.

That matters because not all real estate exposure is built for dependable income. Equity ownership may offer appreciation, but it also comes with more variables. Rent collections, occupancy, insurance costs, cap rate changes, and deferred maintenance all affect outcomes. In a private credit strategy, the primary objective is usually different. The emphasis is on current income, principal protection, and collateral coverage rather than on maximizing upside.

For accredited investors, that distinction is often the point. The goal is not to chase the highest possible return. It is to pursue attractive income with a structure designed to manage downside risk.

Passive income investments in real estate: debt versus equity

When people hear real estate investing, they often picture apartments, office buildings, or short-term rentals. That is the equity side of the market. Equity investors own the asset and benefit if net operating income rises or the property appreciates. They also absorb the first loss if the business plan underperforms.

Private real estate credit works differently. A lender is typically paid through interest and fees under a loan agreement secured by a mortgage or deed of trust. In many disciplined strategies, that loan is in first position, meaning it has priority over subordinate claims tied to the property. That seniority matters. So does loan-to-value discipline. A loan originated at 65 percent to 75 percent of property value generally offers more collateral cushion than a highly leveraged structure.

This does not eliminate risk. Real estate values can decline, projects can stall, and borrowers can default. But the risk profile is different from equity exposure. The investor is not depending entirely on a profitable sale or long-term appreciation to get paid. The repayment source may be refinance, sale, or operating cash flow, but the investment is anchored by a legal claim against the asset.

What makes a real estate-backed income strategy truly passive

Many investments are marketed as passive when they are only passive after a substantial amount of sourcing, oversight, and problem-solving. Direct ownership is the obvious example. Even with third-party management, investors still face capital calls, leasing issues, repairs, and uneven cash flow.

A well-structured private credit fund can be more genuinely passive because underwriting, loan servicing, borrower monitoring, and collateral administration are handled by an experienced manager. The investor is not evaluating individual contractors, negotiating leases, or managing draw requests on a construction site. Instead, the investor is relying on the manager’s process.

That shifts the key diligence question. Rather than asking whether a property has granite countertops or strong curb appeal, a sophisticated investor should ask how the platform originates loans, verifies collateral value, sizes leverage, documents security interests, and manages workouts when needed. In this segment of passive income investments real estate, manager discipline is not a detail. It is the investment.

The due diligence factors that matter most

In real estate-backed private credit, yield should never be reviewed in isolation. Higher stated income can simply reflect higher risk, weaker collateral, longer duration, or looser underwriting. The more useful analysis starts with loan quality.

A prudent investor should evaluate whether the strategy focuses on first-position loans, what typical loan-to-value ranges look like, how properties are valued, and whether the manager lends against residential, commercial, or mixed collateral. Duration also matters. Shorter-duration loans can reduce exposure to long-term rate uncertainty and changing market conditions, though they may require consistent origination strength to keep capital deployed.

Borrower quality is another key variable. Experienced borrowers with meaningful equity in the deal tend to behave differently than thinly capitalized sponsors relying on optimistic assumptions. The underwriting process should account for exit strategy viability, project timeline realism, market demand, and sponsor liquidity.

Then there is servicing and asset management. A private credit strategy should not be judged only by how it performs when every borrower pays on time. It should be judged by what happens when a project runs late, a budget changes, or a sale timeline slips. Strong operators have procedures for monitoring draws, tracking borrower performance, and enforcing loan documents before small problems become large ones.

Where real estate private credit can fit in an income portfolio

For accredited investors, private real estate credit often serves as a complement rather than a replacement. It may sit alongside public fixed income, cash reserves, and other alternative income strategies. Its role is usually straightforward: provide current income backed by tangible collateral, with lower correlation to daily market pricing than publicly traded securities.

That can be especially relevant for investors evaluating retirement income strategies. Monthly or periodic distributions may be more useful than paper gains that fluctuate with broad market sentiment. Investors using self-directed IRAs or rollover IRA capital often find the structure appealing because it can align with a need for income generation while keeping exposure tied to hard assets rather than unsecured obligations.

Still, fit depends on liquidity needs and investor profile. Private funds are not designed for daily trading or immediate access to capital. They are better suited to investors who understand private placement structures, can tolerate reduced liquidity, and prioritize income stability and asset backing over full liquidity.

Why underwriting discipline matters more than market narratives

There is a tendency in real estate to speak in broad cycles and headlines. Office is weak. Housing is undersupplied. Rates may fall. Banks are pulling back. Those themes matter, but they are not a substitute for credit work.

A conservative private lender can find opportunity in a mixed market if the basis is right, the collateral is sound, and the borrower has a credible path to repayment. A poorly underwritten loan can fail in a strong market. A carefully structured loan can perform in a more uncertain one. That is why experienced investors focus less on broad optimism and more on process.

The best private credit platforms tend to be consistent in ordinary ways. They maintain lending standards. They avoid stretching leverage to win volume. They favor collateral coverage over promotional return targets. They care about documentation, inspections, title, insurance, and servicing. None of that is flashy. For income-oriented investors, that is usually a good sign.

What accredited investors should ask before allocating

Before committing capital, investors should look for evidence of repeatable execution. How long has the manager operated through different market conditions? What types of loans are being originated? How is risk controlled at the asset level and portfolio level? Are distributions derived from actual lending activity, and how are defaults or extensions handled?

Track record deserves close attention, but so does the explanation behind it. A fund that emphasizes capital preservation, conservative loan terms, and disciplined collateral review is generally easier to underwrite than one built around broad claims and aggressive projections. In this part of the market, transparency around process is often more valuable than marketing language around yield.

This is one reason some investors are drawn to firms such as Mid Atlantic Secured Income Fund. The appeal is not simply that real estate is involved. It is that the strategy centers on secured lending, first-position mortgages, conservative loan-to-value parameters, and income generated by contractual loan payments rather than by speculative appreciation.

Passive income works best when it is built on active risk management behind the scenes. In real estate, that often means looking beyond ownership and toward lending structures where collateral, seniority, and underwriting discipline shape the outcome. For accredited investors who value current income and capital preservation, the right opportunity is often the one that does not ask for excitement at all – only consistency, security, and a process you can trust.