Best Investment Funds for Retirement in 2026: Institutional Portfolio Strategies Beyond Traditional Stocks and Bonds

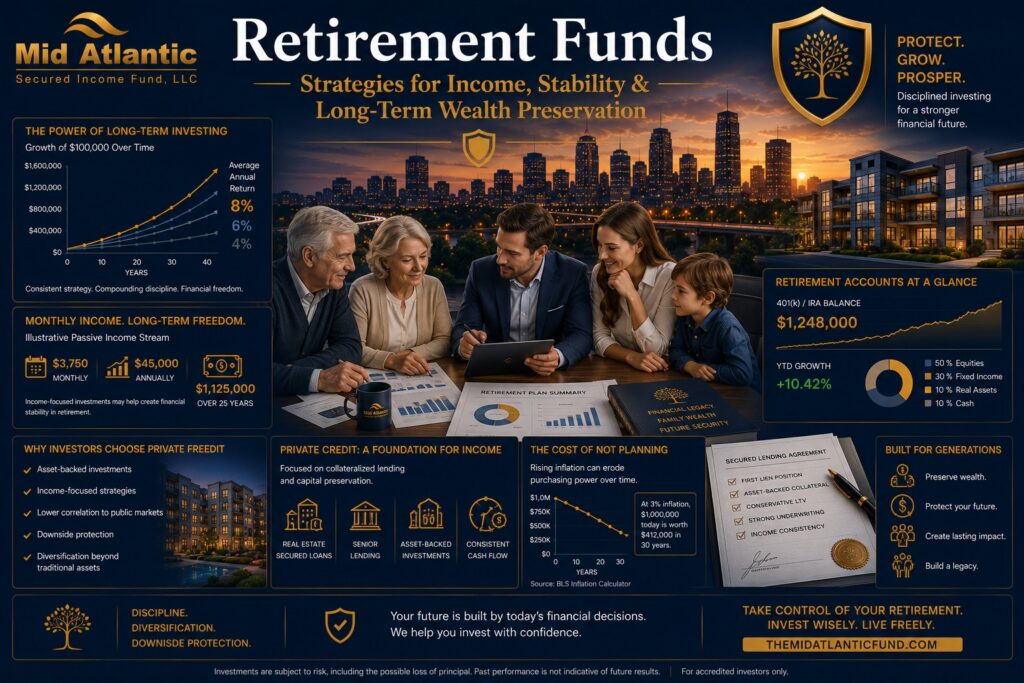

Retirement Investing Is Undergoing a Structural Shift For decades, retirement investing in the United States largely followed a familiar formula: stocks for growth, bonds for stability, and mutual funds as the default allocation vehicle. That framework is increasingly being challenged. Persistent inflation pressures, elevated market volatility, longer retirements, shifting interest rate environments, and declining confidence in traditional 60/40 portfolios are causing retirees and pre-retirees to rethink how retirement capital should be managed. Institutional investors have already adapted. According to BlackRock, Apollo, Goldman Sachs, and Preqin research, pension funds, endowments, family offices, and insurance companies have steadily increased allocations to alternative income-oriented investments over the last decade. Private credit, infrastructure, real estate-backed debt, and non-correlated income strategies are now core components of institutional retirement portfolios. Individual accredited investors are beginning to follow the same trend. The modern retirement portfolio is no longer built solely around maximizing returns. Instead, sophisticated investors increasingly focus on: durable income generation, downside mitigation, inflation resilience, tax efficiency, diversification beyond public markets, and capital preservation across market cycles. This evolution has fundamentally changed the conversation around the best investment funds for retirement. What Are the Best Investment Funds for Retirement? Direct Answer The best investment funds for retirement are those that align with an investor’s: income needs, risk tolerance, liquidity requirements, time horizon, and long-term wealth preservation objectives. For many investors, a diversified retirement portfolio may include: dividend equity funds, bond funds, private credit funds, real estate debt funds, REITs, infrastructure investments, and alternative income-focused strategies. Increasingly, institutional investors and accredited individuals are incorporating private credit and asset-backed income funds to complement traditional stock and bond allocations. Why Retirement Investors Are Expanding Beyond Traditional Portfolios The Traditional 60/40 Portfolio Faces New Challenges For decades, retirement portfolios often relied on: 60% equities 40% fixed income The assumption was straightforward: equities drove growth, bonds provided stability. However, recent macroeconomic conditions exposed vulnerabilities in this approach. In 2022, both stocks and bonds declined simultaneously — a historically uncommon event that challenged assumptions around diversification. Meanwhile: inflation remained elevated, bond purchasing power deteriorated, and retirees faced increased sequence-of-return risk. According to Morningstar and BlackRock research: retirees are increasingly prioritizing income stability over pure appreciation, especially in the years immediately before and after retirement. Understanding Sequence-of-Return Risk Why Early Retirement Losses Matter More Than Many Investors Realize Sequence-of-return risk refers to the danger of experiencing significant portfolio losses early in retirement while simultaneously withdrawing income. Even if long-term market averages eventually recover, early losses combined with withdrawals can permanently impair retirement sustainability. This is one reason many institutional retirement frameworks now emphasize: diversified income streams, lower volatility assets, and non-correlated investments. Categories of Retirement Investment Funds 1. Dividend Equity Funds Dividend-focused funds invest in companies that distribute regular cash dividends. These funds are commonly used for: income generation, inflation participation, and long-term equity exposure. Advantages Potential dividend growth Public market liquidity Exposure to blue-chip companies Risks Equity market volatility Dividend reductions during recessions Correlation to broader markets 2. Bond Funds Bond funds remain foundational components of many retirement portfolios. They typically include: Treasury bonds, municipal bonds, investment-grade corporate debt, and government-backed securities. Advantages Historically lower volatility than equities Income generation Capital preservation characteristics Risks Interest rate sensitivity Inflation erosion Lower yields during certain economic cycles 3. Real Estate Investment Trusts (REITs) REITs provide exposure to income-producing real estate assets. Examples include: apartment portfolios, industrial warehouses, data centers, medical office buildings, and commercial real estate. NAREIT data has historically shown that REITs can provide: income, inflation sensitivity, and diversification benefits. Risks Public market volatility Commercial real estate downturns Interest rate exposure 4. Private Credit Funds One of the Fastest Growing Institutional Asset Classes Private credit has emerged as one of the most significant institutional investment trends of the past decade. According to Preqin: global private credit assets under management surpassed $1.7 trillion in recent years, with continued projected growth through the decade. Private credit funds generally provide financing outside traditional banking channels. These may include: senior secured loans, real estate-backed lending, bridge lending, asset-backed financing, and specialty finance strategies. Why Institutional Investors Use Private Credit Institutional allocators often utilize private credit because it may offer: income potential, floating-rate structures, collateral-backed lending, lower public market correlation, and downside-focused underwriting. Unlike traditional equity investments, many private credit structures prioritize: contractual cash flow, asset security, and capital stack positioning. What Is a Real Estate Debt Fund? Direct Answer A real estate debt fund pools investor capital to originate or acquire loans secured by real estate collateral. Unlike equity real estate investing, debt funds generally focus on: loan income, interest payments, and collateral-backed lending structures. Some funds specialize in: first-lien positions, bridge lending, construction financing, or stabilized real estate loans. Why Real Estate-Backed Income Strategies Appeal to Retirees Retirement investors increasingly seek investments tied to: tangible assets, contractual income, and collateral-backed structures. Real estate-backed lending strategies may provide: monthly or periodic distributions, lower volatility than equities, and defensive portfolio characteristics. Sophisticated retirement investors often value: asset security, disciplined underwriting, and income consistency over speculative appreciation. Accredited Investors and Alternative Retirement Strategies Why High-Net-Worth Investors Often Allocate Differently Accredited investors frequently have access to investments unavailable in traditional brokerage accounts. These may include: private credit funds, institutional debt strategies, private real estate vehicles, and specialty income funds. According to numerous family office studies, high-net-worth portfolios often allocate meaningfully to: alternatives, real assets, and private markets. The rationale is typically centered on: diversification, inflation mitigation, and non-correlated income generation. How SDIRAs Expand Retirement Investment Flexibility What Is an SDIRA? A Self-Directed IRA (SDIRA) allows investors to hold a broader range of investments inside retirement accounts. These may include: private credit, private real estate, real estate debt funds, precious metals, private equity, and alternative assets. SDIRAs are commonly used by investors seeking: diversification beyond public markets, tax-advantaged alternative investments, and greater portfolio flexibility. Related Internal Resource: https://themidatlanticfund.com/ira-investing-with-mid-atlantic-fund/ Retirement Income Versus Retirement Growth The Psychological Shift Many Investors Experience During accumulation years, investors often focus primarily on: maximizing growth, increasing