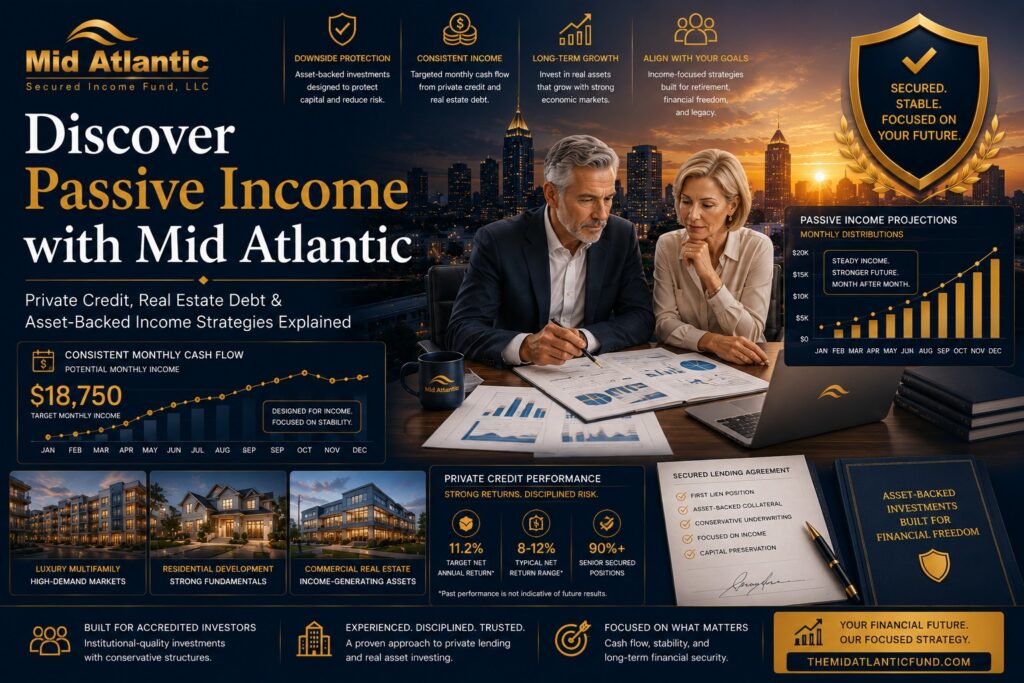

Secured Income for Angel Investors in the US

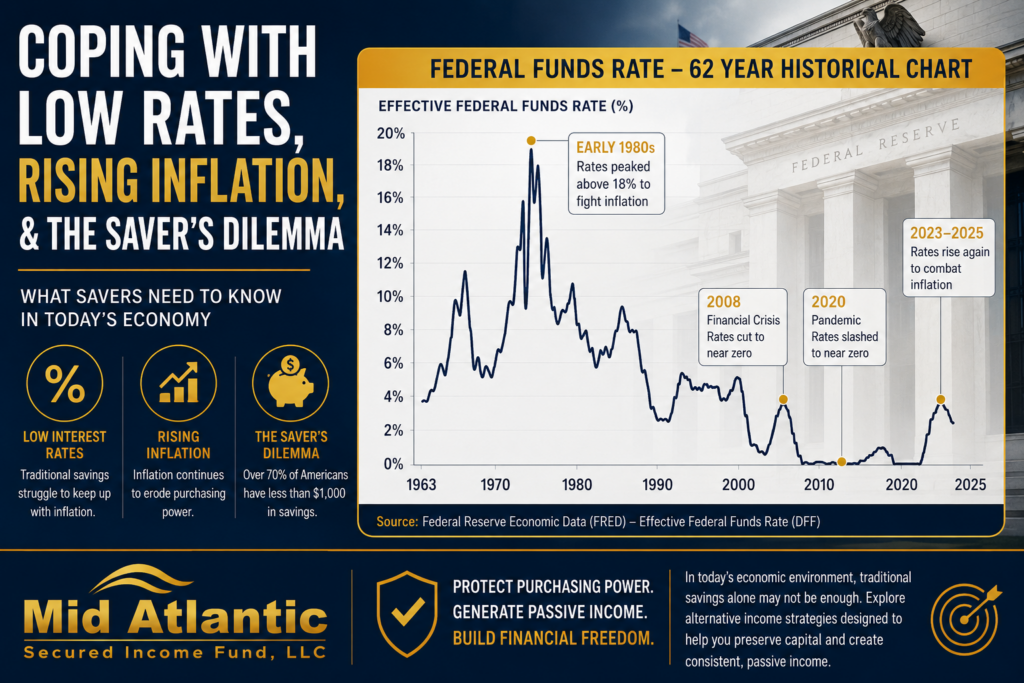

Why Angel Investors Are Reconsidering Portfolio Construction Angel investing has long represented one of the most compelling paths to asymmetric wealth creation. Early-stage startup investments have the potential to generate extraordinary returns when companies successfully scale, raise institutional capital, or achieve liquidity events. Yet experienced angel investors also understand a less glamorous reality: Startup investing is inherently high risk. Illiquidity, valuation uncertainty, extended holding periods, and elevated failure rates create portfolio instability that can persist for years before outcomes become clear. For many accredited investors, entrepreneurs, founders, and early-stage allocators, this has created a growing interest in balancing high-upside venture exposure with more durable income-producing investments. Increasingly, angel investors are asking: How can startup investors generate recurring passive income? What role should secured investments play alongside venture exposure? How do institutional investors balance risk and cash flow? Can private credit improve portfolio resilience? How can accredited investors preserve capital while maintaining growth exposure? This shift reflects a broader evolution occurring across institutional portfolio construction. Sophisticated investors increasingly recognize that long-term wealth creation is not solely about maximizing upside. It is also about: managing volatility, improving liquidity flexibility, preserving purchasing power, and creating sustainable recurring cash flow. As a result, many angel investors increasingly allocate portions of their portfolios toward: private credit, asset-backed investments, secured lending, alternative income strategies, and diversified passive income structures. What Is Secured Income Investing? Direct Answer Secured income investing refers to investment strategies designed to generate recurring cash flow through investments backed by collateral or underlying assets. Examples may include: private credit, senior secured lending, real estate-backed lending, asset-backed investments, and contractual income-producing strategies. Many accredited investors use secured income investments to diversify risk, improve portfolio resilience, and generate passive income alongside higher-volatility growth investments. Why Angel Investors Need Diversification Venture Capital Concentration Risk Is Real One of the defining characteristics of startup investing is concentration risk. Many angel portfolios become heavily exposed to: technology startups, illiquid equity positions, macroeconomic growth cycles, and speculative valuation environments. This concentration may create several challenges: Portfolio Challenge Impact Illiquidity Limited near-term cash flow Extended holding periods Delayed realization timelines High failure rates Capital impairment risk Market volatility Valuation uncertainty Capital call fatigue Ongoing reinvestment pressure Institutional investors rarely rely exclusively on high-risk growth assets. Instead, sophisticated portfolios increasingly incorporate income-producing investments designed to stabilize broader portfolio performance. The Institutional Shift Toward Private Credit Private Credit Has Become Mainstream Private credit has rapidly evolved from a niche alternative asset class into a core institutional allocation strategy. According to Apollo Global Management, BlackRock, and Preqin, private credit has become one of the fastest-growing segments within alternative investments globally. Several structural forces have contributed to this expansion: bank retrenchment, higher interest rates, increased demand for income, public market volatility, and institutional diversification strategies. What Is Private Credit? Direct Answer Private credit refers to non-bank lending where investors provide capital directly to borrowers through privately negotiated debt investments rather than traditional public bond markets or bank financing. Private credit strategies may include: bridge lending, commercial real estate lending, construction financing, asset-backed lending, and specialty finance. Private credit often emphasizes: contractual income, underwriting discipline, collateral awareness, and portfolio diversification. Why Angel Investors Are Exploring Income-Producing Investments Cash Flow Improves Portfolio Flexibility One challenge many angel investors encounter is the absence of recurring liquidity. Startup equity investments may require years before monetization occurs — if monetization occurs at all. Income-producing investments may help offset this dynamic by providing: recurring cash flow, reinvestment flexibility, portfolio stability, and reduced dependence on liquidity events. This becomes particularly important during: venture funding slowdowns, public market corrections, higher interest rate environments, and economic recessions. Institutional investors frequently emphasize balancing: growth exposure, passive income, and downside management. Understanding Secured Investments What Are Secured Investments? Secured investments are investments backed by collateral or underlying assets that may provide additional structural protections compared to unsecured investments. Examples may include: senior secured private loans, real estate-backed lending, collateralized credit investments, and asset-backed income strategies. Collateral structures do not eliminate risk. However, they may improve downside positioning during periods of economic stress. Real Estate-Backed Lending and Portfolio Stability Why Real Assets Matter Real estate-backed lending strategies increasingly play an important role within diversified accredited investor portfolios. Debt-oriented real estate investments often emphasize: contractual repayment, underwriting discipline, collateral backing, and recurring income generation. Institutional investors frequently evaluate: loan-to-value ratios, borrower quality, geographic diversification, and asset quality when assessing real estate-backed lending opportunities. Real assets may also provide diversification relative to venture equity exposure. Are Debt Investments Safer Than Startup Equity? Direct Answer Debt-oriented investments are not risk-free, but certain secured lending and private credit investments may provide: contractual income, collateral backing, lower volatility characteristics, or senior repayment positioning relative to early-stage venture equity investing. All investments carry risk. Sophisticated investors evaluate investments based on: diversification, underwriting quality, economic conditions, liquidity, and portfolio objectives. Angel Investing and Behavioral Finance Emotional Decision-Making Can Distort Portfolios Behavioral finance plays a significant role within startup investing. Angel investors often become emotionally attached to: founders, company narratives, disruptive technologies, and outsized return potential. While conviction matters, concentration risk and emotional investing may distort portfolio construction over time. Income-producing investments may help improve psychological stability by emphasizing: recurring cash flow, portfolio balance, and long-term financial durability. Institutional investors frequently structure portfolios specifically to reduce emotionally reactive decision-making. Inflation and Angel Investor Portfolios Inflation Changes Portfolio Priorities Inflation materially affects long-term portfolio sustainability. According to the U.S. Bureau of Labor Statistics, inflation surged to multi-decade highs following pandemic-era monetary expansion and supply chain disruptions. This has increased investor focus on: cash-flow-producing investments, alternative income strategies, real assets, and diversified portfolio construction. Angel investors increasingly seek investments capable of generating passive income while preserving purchasing power over time. How Institutional Investors Balance Growth and Income Institutions Rarely Rely on One Asset Class Large institutional investors rarely structure portfolios around a single source of return. Instead, sophisticated portfolios increasingly balance: growth assets, private markets, income-producing investments, and defensive diversification. Several institutional principles increasingly influence

Secured Income for Angel Investors in the US Read More »