When an investor no longer needs more market drama and starts prioritizing cash flow, the conversation changes fast. The best passive income investments for accredited investors are rarely the loudest products in the market. They are the ones with durable income mechanics, understandable risk, and a structure that still makes sense when conditions tighten.

For accredited investors, that usually means looking beyond traditional bonds, public REITs, or broad equity income strategies and evaluating private market income opportunities on their merits. The key question is not simply where the headline yield is highest. It is where income is supported by underwriting discipline, asset coverage, and a realistic path to preserving capital.

What makes an income investment worth owning

Passive income can come from many places, but not all income is created the same way. Some strategies depend heavily on market sentiment, refinancing conditions, or aggressive growth assumptions. Others are built around contractual payments, hard assets, and shorter-duration structures that may offer more control over downside risk.

For most accredited investors, the right filter includes four factors: current income, volatility, liquidity, and loss severity if something goes wrong. A high distribution rate may look attractive, but if principal is exposed to long-duration market swings or speculative valuation assumptions, the real risk-adjusted return may be less compelling than advertised.

That is why sophisticated investors often separate passive income strategies into two buckets. The first is market-priced income, where values can move daily and distributions can rise or fall with public markets. The second is contract-driven income, where cash flow is tied more directly to loan terms, lease payments, or private agreements. In uncertain rate environments, that distinction matters.

Best passive income investments for accredited investors by category

Private real estate credit funds

For investors focused on income and capital preservation, private real estate credit deserves serious attention. These funds generally lend against real property and generate returns through interest payments rather than property appreciation. That difference is central. In a debt structure, the investor is not relying on a building to sell at a higher valuation. The income comes from the borrower making scheduled payments under defined loan terms.

The strongest versions of this strategy tend to focus on first-position loans, conservative loan-to-value ratios, and short durations. That structure can provide multiple layers of protection: real estate collateral, legal priority in the capital stack, and the ability to reprice or recycle capital more frequently than long-term fixed-income instruments. For accredited investors seeking monthly or periodic income, this is often one of the most practical alternatives to traditional yield products.

Of course, manager selection is critical. A private credit fund is only as strong as its underwriting, servicing, and workout discipline. Investors should look closely at collateral standards, default management experience, historical loss performance, and whether the manager prioritizes principal protection over volume.

Private debt backed by business receivables or asset-based lending

Another category worth evaluating is private asset-based lending tied to receivables, invoices, or other business assets. These strategies can produce attractive income because borrowers are paying for speed, flexibility, and structured capital that banks may not provide.

The trade-off is that business-credit collateral is often less straightforward than real estate. Recovery values can change faster, and the underwriting burden is higher. Investors should want to understand exactly what secures the loan, how collateral is monitored, and how quickly a manager can intervene if performance weakens. In the right hands, this can be a useful income sleeve. In weaker hands, it can become an exercise in chasing yield.

Private real estate equity funds

Real estate equity funds are often marketed as passive income investments, and some do distribute cash flow from rental operations. But they should be evaluated differently from private credit. Equity investors sit behind debt in the capital stack and are more exposed to valuation declines, leasing risk, operating expenses, and exit timing.

That does not make private real estate equity inherently unattractive. It can play a role for investors who want a blend of income and long-term appreciation. But for those whose priority is dependable current income with lower volatility, equity structures are usually less predictable than senior secured lending strategies.

Private placements with fixed distribution targets

Some private placements offer contractual or semi-structured income features, often in niche lending or specialty finance. These can be appealing, especially to investors moving assets from an old 401(k) or evaluating self-directed IRA opportunities. Still, structure matters more than marketing language.

Accredited investors should ask whether distributions are funded by actual operating cash flow, whether assets are marked conservatively, and whether the manager has a credible history across multiple market cycles. Yield without transparency is not an income strategy. It is an assumption.

Why private real estate-backed credit stands out

Among the best passive income investments for accredited investors, real estate-backed private credit often stands out because it aligns income generation with collateral protection. That is particularly relevant in periods when public fixed-income markets face duration pressure or when equity income strategies remain exposed to broad market repricing.

A well-structured real estate credit strategy can offer several advantages. First, income is derived from borrower interest payments, not from hoping cap rates compress or rents rise enough to support future valuations. Second, shorter loan durations can reduce interest rate sensitivity compared with longer-maturity bonds. Third, first-lien positions and conservative loan-to-value ratios may improve recovery prospects if a loan underperforms.

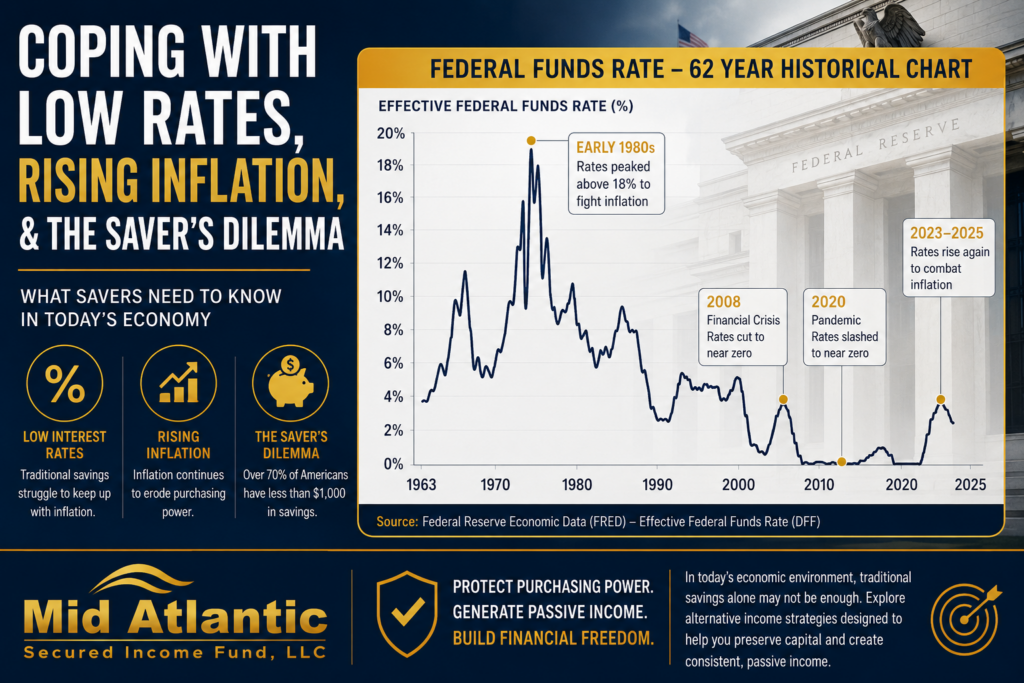

This is one reason many accredited investors, family offices, and SDIRA account holders increasingly evaluate private mortgage lending as an income alternative. The Federal Reserve’s rate cycle has reminded investors that duration risk is real, and the FDIC’s long-term deposit data continues to show that conventional cash vehicles often struggle to keep up with inflation over time. In that context, asset-backed private credit can fill a practical role between low-yield cash and higher-volatility market exposure.

What to review before investing

Income investors should be skeptical in the right way. Not cynical, but disciplined. A private fund may present an attractive distribution profile, yet the underlying risk can vary significantly depending on asset quality and manager process.

Start with the collateral. Is the investment backed by hard assets, and if so, what type? Real estate collateral generally offers a clearer recovery framework than many unsecured or lightly secured structures. Then review position in the capital stack. First-position senior debt typically offers a different risk profile than subordinated debt or equity.

Next, assess duration and liquidity. Shorter-duration strategies can help reduce exposure to long-term rate movements, but private investments are still less liquid than public securities. Investors should match the strategy to their actual time horizon rather than treat all passive income as interchangeable.

Finally, evaluate the operator. This is where experience matters most. Underwriting standards, servicing capability, borrower selection, and default resolution discipline are not marketing details. They are the investment. Firms that emphasize conservative loan-to-value ratios, active asset management, and consistency of distributions are generally better aligned with income-focused investors than managers competing primarily on yield.

A note on retirement capital and self-directed accounts

Many accredited investors first encounter alternative income strategies after a liquidity event, retirement transition, or rollover from an unused 401(k). In those cases, the objective is often straightforward: replace idle capital or low-yield holdings with investments that can generate meaningful current income without taking equity-like volatility.

That is where private credit can fit naturally, including through certain self-directed IRA structures when appropriate for the investor’s broader plan. The appeal is not complexity. It is function. Contractual income, asset backing, and a clearer risk framework can be easier to evaluate than public market noise, especially for investors focused on distribution consistency rather than benchmark tracking.

Mid Atlantic Secured Income Fund operates in that part of the market, with a focus on short-term first-position mortgage lending and a capital-preservation-first approach. Whether an investor evaluates one fund or several, the broader principle holds: passive income works best when the source of return is clear, the collateral is tangible, and risk controls are visible.

Choosing the right fit

The best passive income investment is rarely universal. It depends on whether the investor values liquidity above yield, wants pure income versus income plus appreciation, or needs a structure compatible with retirement assets. But for accredited investors who want predictable cash flow and a stronger emphasis on downside protection, private real estate-backed credit remains one of the more compelling categories to study closely.

If the income is real, the collateral is real, and the underwriting is disciplined, passive investing can feel less like reaching for yield and more like applying common sense to capital.