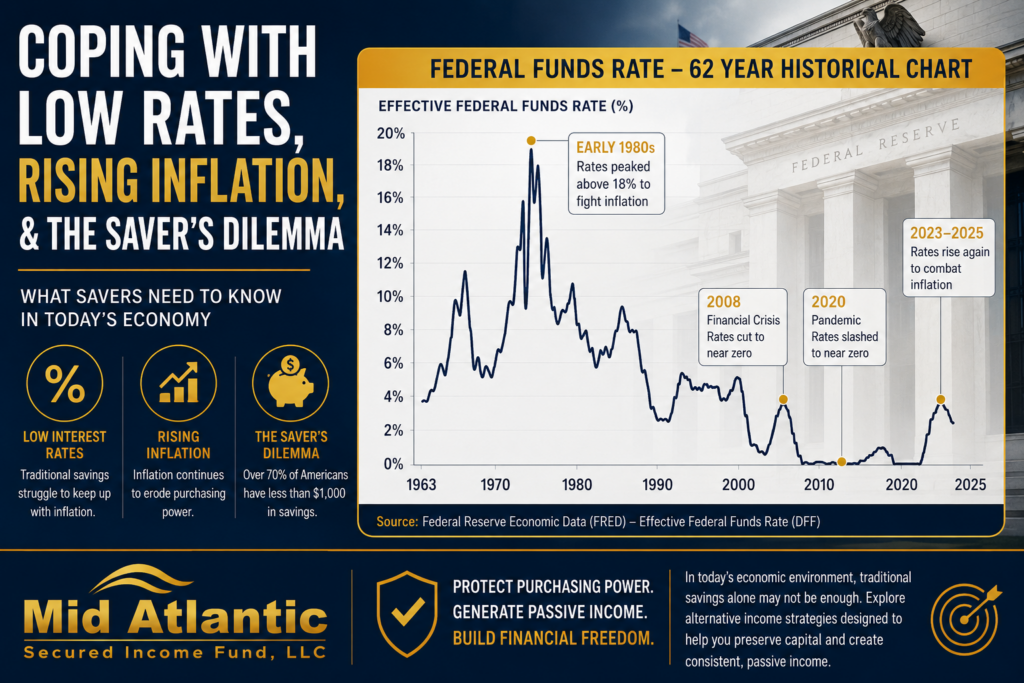

When investors say they want income, what they often mean is simpler: they do not want to spend the next decade rebuilding capital after a bad drawdown. That is why top capital preservation investment strategies deserve a serious look, especially for accredited investors, retirees, and rollover IRA holders who need current income without taking equity-like volatility.

Capital preservation is not the same as avoiding risk altogether. It is the disciplined practice of structuring a portfolio so that principal protection comes first, yield comes second, and speculation stays in the background. In a market shaped by changing interest rates, tighter credit conditions, and periodic swings in public valuations, that distinction matters.

What capital preservation really requires

A preservation-focused investor is not just asking, “What can this investment earn?” The better question is, “What protects my downside if conditions worsen?” That shift in thinking changes the entire evaluation process.

In practice, capital preservation tends to rest on a few core features: seniority in the capital stack, tangible collateral, short to intermediate duration, strong liquidity planning, and underwriting discipline. The Federal Reserve and FDIC data have repeatedly reminded investors that nominal safety and real safety are not always the same thing. Cash may offer stability in principal, but inflation can steadily erode purchasing power. Long-duration bonds may look conservative, yet they can suffer meaningful mark-to-market losses when rates rise.

That is why the strongest strategies often combine stability, income, and explicit downside controls rather than relying on a single label like “safe.”

Top capital preservation investment strategies for income-focused investors

High-yield savings and Treasury bills

For pure liquidity and near-term cash needs, few tools are more straightforward than FDIC-insured deposit accounts and short-term US Treasury bills. These are often the first layer of a preservation strategy because they provide immediate access to funds and low default risk.

The trade-off is clear. Yields can fluctuate quickly, and after taxes and inflation, real returns may be modest. For investors with upcoming spending needs or those waiting to deploy capital, these vehicles are useful. For investors trying to generate durable passive income, they are usually a parking place, not a complete solution.

Short-duration investment-grade bonds

Short-duration bonds can still play a role when the goal is to limit sensitivity to interest rate movements. Compared with longer-term bonds, they generally experience less price volatility when rates move higher.

Still, preservation-minded investors should be realistic. Investment-grade does not eliminate duration risk, reinvestment risk, or credit risk. If the objective is steady income with reduced mark-to-market volatility, shorter duration tends to be more consistent than stretching for yield through longer maturities.

Laddered fixed-income allocations

A laddered approach spreads maturities across different time frames so capital comes due periodically rather than all at once. That can improve liquidity planning and reduce the risk of allocating everything at one interest rate level.

This is less an asset class than a discipline. It works best for investors who want predictable cash flow scheduling and flexibility. The limitation is that ladders still depend on the quality of the underlying instruments. A ladder of weak credits is still weak credit exposure.

Cash-value life insurance for specific planning cases

For certain high-net-worth investors with estate planning objectives, cash-value life insurance may provide a conservative component within a broader wealth structure. It can offer contractual features and tax advantages depending on policy design.

But this is not a universal income solution, and it should not be treated as one. Fees, surrender schedules, and complexity can make it a poor fit for investors whose primary goal is current yield and transparent collateral-backed risk management.

Private credit with senior secured positioning

This is where many sophisticated investors begin to see a more compelling balance between preservation and income. Private credit, when structured conservatively, can offer contractual cash flow, lower correlation to public markets, and stronger downside protection than unsecured lending or equity ownership.

The key phrase is when structured conservatively. Not all private credit is designed for capital preservation. Investors should look closely at loan duration, borrower quality, underwriting standards, collateral coverage, lien position, and manager experience.

Senior secured private credit typically sits ahead of equity in the capital stack, and in many cases ahead of subordinate debt as well. That matters because repayment priority is one of the most practical forms of risk control. The strategy becomes more compelling when loans are short duration, asset-backed, and originated with conservative advance rates.

Real estate-backed first-position mortgage lending

Among the top capital preservation investment strategies, real estate-backed first-position lending deserves special attention for accredited investors seeking current income with tangible collateral support. Rather than relying on property appreciation, this approach focuses on lending against real assets at conservative loan-to-value levels.

That distinction is significant. Equity-style real estate investing often depends on market timing, lease-up assumptions, operating execution, and exit pricing. A first-position lender is in a different risk posture. The lender is not betting on upside first. The lender is underwriting collateral value, borrower execution, and a margin of safety from day one.

Conservative loan-to-value ratios, often in the 65% to 75% range, create an equity cushion designed to absorb potential market softening. Short-duration loan structures can further reduce exposure to long-cycle valuation swings. When loans are secured by residential or commercial real estate and managed through disciplined servicing, investors gain exposure to contractual income tied to hard assets rather than public market sentiment.

This does not mean the strategy is risk-free. Real estate values can decline, projects can be delayed, and workouts can take time. But from a preservation standpoint, the combination of first-lien security, collateral coverage, and underwriting discipline often compares favorably with unsecured income products or long-duration bond exposure.

Structured alternative income funds

For investors who prefer pooled access rather than selecting individual deals, a professionally managed alternative income fund can offer diversification across multiple loans and borrowers. That can reduce single-asset concentration and provide a more consistent distribution profile.

Manager selection is critical here. Investors should study whether the fund emphasizes collateralized lending, how it handles borrower defaults, what its duration profile looks like, and whether distributions are supported by actual loan income rather than financial engineering. A disciplined manager with a capital-preservation-first mandate will typically communicate more about downside controls than headline returns.

How to evaluate capital preservation strategies without chasing labels

The most common mistake in this category is assuming that familiar means safe. Many investors learned during recent rate cycles that traditional bond allocations can lose value, and many also learned that cash can quietly lose purchasing power over time. Preservation requires looking beneath the label.

A better evaluation framework starts with a few direct questions. What stands behind the investment if performance weakens? Is there hard collateral? Where does the investor sit in the repayment hierarchy? How long is the capital exposed? What underwriting standards govern new allocations? And how much of the return depends on market appreciation versus contractual cash flow?

For accredited investors, this framework often leads toward strategies that are less dependent on public market pricing and more dependent on asset coverage and structure. That is one reason real estate-backed private credit has gained attention among investors looking for alternatives to traditional fixed income, particularly within self-directed IRAs and rollover IRA capital seeking passive income.

When each strategy makes sense

There is no single best answer for every investor. A retiree holding one to two years of living expenses may prioritize liquidity first and private credit second. A family office with a longer time horizon may accept lower liquidity in exchange for higher current income and stronger asset-backed protections. An investor moving funds from an old 401(k) into a self-directed IRA may focus on balancing distribution needs with principal stability.

In that context, preservation is usually strongest when built in layers. Cash and short-term Treasuries can cover immediate liquidity. Short-duration bonds can provide familiar fixed-income exposure. Senior secured private credit and real estate-backed lending can serve as the higher-income component designed to preserve capital through collateral, structure, and disciplined underwriting.

That layered approach is often more resilient than relying on any one bucket to do everything.

Why underwriting discipline matters more than yield

Yield attracts attention, but underwriting protects capital. Two investments with similar stated returns can have very different risk profiles depending on lien position, collateral type, loan-to-value ratio, borrower quality, and servicing capability.

That is particularly true in private markets, where manager discipline determines outcomes. A fund that originates short-term first-position loans with conservative underwriting is operating very differently from a lender stretching leverage or relying on optimistic property values. Mid Atlantic Secured Income Fund’s emphasis on collateralized lending and conservative loan structures reflects the kind of framework serious preservation-oriented investors tend to value.

Investors who keep that focus are usually asking the right question. Not “What is the highest yield available?” but “What process stands between my capital and permanent loss?”

For investors seeking dependable income, the strongest strategy is often the one that still looks sound when markets get less cooperative. That is where capital preservation stops being a marketing phrase and becomes an investment standard.