Self Directed IRA Real Estate Debt Explained

Learn how self directed IRA real estate debt works, where income comes from, key risks, IRA rules, and what disciplined underwriting can protect.

Self Directed IRA Real Estate Debt Explained Read More »

Learn how self directed IRA real estate debt works, where income comes from, key risks, IRA rules, and what disciplined underwriting can protect.

Self Directed IRA Real Estate Debt Explained Read More »

As investors continue looking for ways to diversify beyond traditional markets, self-directed IRAs (SDIRAs) have become increasingly popular. These accounts allow owners access to alternative assets to build retirement wealth. Alternative investments, such as real estate, private credit, private equity, and other non-publicly traded offerings, are not typically available through traditional brokerage accounts. For retirement savers looking for diversification strategies, understanding how self-directed IRAs work and the rules that govern them is an important first step. What Is a Self-Directed IRA? A self-directed IRA allows investors to take a more active role in their retirement strategy by choosing a broader range of investments while maintaining the same tax advantages offered by conventional retirement accounts. A self-directed IRA is a retirement account that follows the same IRS rules and tax advantages as traditional IRAs. However, self-directed investors get to invest in an asset class called alternative investments, which includes a much larger pool of options besides stocks, bonds, and mutual funds. Traditional retirement accounts held at brokerage firms typically limit investors to publicly traded assets like stocks, bonds, and mutual funds. A self-directed IRA, however, allows retirement funds to be allocated into alternative assets that fall outside those traditional categories. These accounts can be structured in the same ways as conventional retirement plans, including: Traditional IRAs Roth IRAs SEP IRAs SIMPLE IRAs Solo 401(k)s The key difference is control. With a self-directed account, the investor chooses the investments for their account. A specialized self-directed IRA custodian, such as Advanta IRA, administers the account and handles required recordkeeping and IRS reporting. This structure allows investors to incorporate assets that may behave differently from public markets and potentially enhance diversification within a retirement portfolio. Income and gains generated by investments flow into the self-directed IRA, just as it works with a conventional plan, preserving the account’s tax advantages. Why Investors Are Turning to Alternative Assets Over the past decade, alternative investments have gained attention among retirement investors seeking to reduce dependence on public market performance. Alternative assets can offer different risk and return characteristics than traditional securities, which may help create a more balanced portfolio. Some reasons investors pursue alternative assets within self-directed retirement accounts include: Diversification: Assets like real estate, gold, and private equity often move independently of stock market performance. Income potential: Many alternative investments generate recurring income, such as rental income or interest payments generated by private loans from a self-directed IRA. Access to private markets: Investors can participate in private deals and funds not available on public exchanges. Greater investment control: Self-directed accounts allow investors to pursue opportunities aligned with their expertise and investment strategy. While these advantages attract many investors, alternative investments also require careful research, due diligence, and adherence to IRS rules governing retirement accounts. Common Alternative Assets Used in Self-Directed IRAs The IRS permits retirement accounts to hold many types of investments as long as they are not specifically prohibited. As a result, self-directed IRAs are used to invest in a variety of alternative asset classes. Real Estate Real estate remains one of the most widely used investments within self-directed IRAs. Investors may purchase assets such as: Residential rental properties Commercial real estate Raw land Real estate investment partnerships or syndications Private Credit Private credit investments have become increasingly popular as investors seek income-producing passive assets. Through a self-directed IRA, investors may participate in: Private lending arrangements Mortgage notes Debt funds Bridge loans These investments can provide interest income while allowing investors to participate in financing opportunities outside traditional banking channels. Private Equity and Private Placements Self-directed IRAs can also be used to invest in privately held companies or funds, including: Venture capital investments Startup opportunities Private equity funds Private stock These investments often target long-term growth and allow retirement investors to participate in opportunities typically available only to accredited investors. Precious Metals Certain precious metals that meet IRS purity requirements can also be held within a self-directed IRA. Gold, silver, platinum, and palladium are commonly used by investors who want exposure to tangible assets or potential inflation hedges. How to Open and Fund a Self-Directed IRA Opening a self-directed IRA typically follows a straightforward process, although it requires working with a custodian that supports alternative investments. Choose a Self-Directed IRA Custodian Because traditional brokerages generally do not administer alternative assets, investors must open accounts with custodians that specialize in self-directed retirement plans. These custodians provide the administrative infrastructure necessary for alternative investments. Not all custodians are alike. Fee structures differ. Not all custodians allow every available alternative asset. Some are more experienced with specific investments than others. Investors must make sure the self-directed custodian they choose fits the criteria for their investing goals. Open the Account The investor completes an account application and selects the appropriate plan type, such as a traditional IRA, Roth IRA, or SEP IRA. Fund the Account Self-directed IRAs can be funded in several ways: Transfers from existing IRAs Rollovers from employer-sponsored retirement plans Annual contributions Identify an Investment Once the account is funded, the investor performs due diligence and identifies an investment opportunity that aligns with their strategy. The custodian then processes the transaction and ensures the asset is titled properly in the name of the retirement account. Key Compliance Rules Investors Should Understand Although self-directed IRAs allow a wide range of investment options, they must still follow IRS rules governing retirement accounts. Understanding these rules is critical to preserving the account’s tax-advantaged status. Prohibited Transactions The IRS prohibits certain transactions between a retirement account and disqualified persons, which include: The account owner Spouses Parents and grandparents Children and grandchildren Entities controlled by the account holder or other disqualified persons Fiduciaries, investment advisors, or anyone providing service to the SDIRA Examples of prohibited transactions include: Using IRA-owned property for personal benefit Selling personal assets to the IRA Buying an investment from a disqualified person Prohibited Investments Per IRS regulations, self-directed IRAs may not invest in: Life insurance Collectibles (i.e., works of art, alcohol, certain coins) Violating

Unlocking the Power of Self-Directed IRAs If you’re like many investors, your retirement journey likely began with stocks, bonds, mutual funds, or ETFs. While these traditional investments remain popular, they are not the only options available for building long-term wealth. A Self-Directed IRA (SDIRA) allows investors to expand beyond conventional assets and invest in a broader range of opportunities while maintaining the same tax advantages associated with traditional retirement accounts. For investors seeking greater control, diversification, and flexibility, understanding how Self-Directed IRAs work is an important first step. What Is a Self-Directed IRA? A Self-Directed IRA is a retirement account that gives the account holder authority to select and direct their own investments rather than being limited to the offerings of a traditional brokerage platform. While a qualified custodian or administrator manages account administration, recordkeeping, and compliance, the investor is responsible for identifying and selecting investment opportunities. Key Characteristics of a Self-Directed IRA Investor-directed investment decisions Access to alternative assets Tax-deferred or tax-free growth potential Available as Traditional or Roth IRA structures Subject to the same annual contribution limits as other IRAs This flexibility allows investors to build a retirement portfolio that aligns with their expertise, interests, and long-term financial objectives. Why Investors Choose Self-Directed IRAs Many retirement investors seek greater control over how their capital is allocated. A Self-Directed IRA provides the ability to diversify beyond traditional public markets and pursue opportunities that may not be available through standard retirement accounts. Common Benefits of Self-Directed IRAs Greater Investment Control Investors make their own investment decisions rather than being limited to a predefined menu of securities. Portfolio Diversification Alternative assets may provide exposure to different market segments beyond stocks and bonds. Tax Advantages Depending on account structure, investments may grow on a tax-deferred or tax-free basis. Access to Alternative Investments Investors can participate in opportunities that align with their knowledge and experience. What Can You Invest in With a Self-Directed IRA? One of the primary advantages of a Self-Directed IRA is the broad range of eligible investments. While all investments must comply with IRS regulations, investors often have access to significantly more options than traditional retirement accounts. Real Estate Real estate remains one of the most popular Self-Directed IRA investment categories. Eligible investments may include: Single-family rental properties Multifamily housing Commercial real estate Raw land Investment properties Development opportunities Income and gains generated by these investments flow back into the IRA, preserving the account’s tax advantages. Private Lending Many investors use Self-Directed IRAs to participate in private lending opportunities. Examples may include: Real estate-backed loans Promissory notes Secured lending transactions Private credit investments In these structures, interest payments generally flow directly back into the retirement account. Private Businesses and Private Equity Self-Directed IRAs may also invest in: Private companies Startups Limited partnerships Private equity opportunities These investments can provide exposure to opportunities outside of public stock markets. Precious Metals Certain IRS-approved precious metals may be held within a Self-Directed IRA. Eligible assets may include: Gold Silver Platinum Palladium Specific purity requirements and storage rules apply. Other Alternative Investments Depending on account structure and custodian capabilities, investors may also explore: Tax liens Cryptocurrency Private debt Notes Alternative funds Always verify eligibility and compliance requirements before investing. Important Self-Directed IRA Rules Investors Should Know While Self-Directed IRAs offer significant flexibility, they remain subject to IRS regulations. Understanding these rules is essential for maintaining the tax-advantaged status of the account. Prohibited Transactions Investors generally cannot: Use IRA assets for personal benefit Purchase property they already own Live in or personally use IRA-owned real estate Conduct certain transactions with disqualified persons Disqualified Persons Examples may include: The IRA owner Spouses Parents Grandparents Children Certain business entities controlled by the account owner Violating IRS rules can trigger penalties and tax consequences. How Does a Self-Directed IRA Work? The process is often simpler than many investors expect. Step 1: Open a Self-Directed IRA Establish an account with a qualified Self-Directed IRA custodian or administrator. Step 2: Fund the Account Funding can occur through: Annual contributions IRA transfers 401(k) rollovers Other eligible retirement account transfers Step 3: Identify an Investment Opportunity Research and evaluate investments that align with your objectives and risk tolerance. Step 4: Direct the Investment The custodian executes the transaction according to your instructions. Step 5: Income Returns to the IRA Rental income, interest payments, and investment proceeds generally flow back into the retirement account. Is a Self-Directed IRA Right for You? A Self-Directed IRA may be worth considering for investors who: Want greater control over retirement investments Understand alternative assets Seek diversification beyond public markets Have experience evaluating private investments Are comfortable conducting their own due diligence As with any investment strategy, it is important to understand both the opportunities and risks involved. Frequently Asked Questions About Self-Directed IRAs What is the difference between a Self-Directed IRA and a traditional IRA? A Self-Directed IRA offers access to a broader range of investments beyond traditional stocks, bonds, and mutual funds while maintaining the same tax advantages. Can a Self-Directed IRA invest in real estate? Yes. Many investors use Self-Directed IRAs to purchase rental properties, commercial real estate, land, and other eligible real estate investments. Can I manage my own Self-Directed IRA investments? Yes. The investor directs the investment decisions while the custodian handles administration and compliance. Are Self-Directed IRAs tax-advantaged? Yes. Traditional SDIRAs may provide tax-deferred growth, while Roth SDIRAs may provide tax-free qualified withdrawals. What investments are prohibited inside a Self-Directed IRA? Certain collectibles, life insurance, and prohibited transactions involving disqualified persons are generally not permitted. Learn More About Self-Directed IRAs Interested in learning more about Self-Directed IRAs? Contact American IRA, LLC at 866-7500-IRA (472) for a complimentary consultation, educational resources, and investor guides. American IRA, headquartered in Sioux Falls, South Dakota, serves as a neutral third-party administrator on behalf of the custodian, New Vision Trust Company, a South Dakota-chartered trust company. American IRA does not provide investment advice, investment recommendations, or endorsements. Investors should conduct their own due diligence and

Unlocking the Power of Self-Directed IRAs Read More »

How to Self-Direct Your IRA: A Beginner’s Guide to Taking Control of Your Retirement Looking Beyond Stocks and Mutual Funds? Most investors build their retirement accounts using traditional investments such as stocks, bonds, mutual funds, and ETFs. While these investments can play an important role in a retirement portfolio, they are not the only options available. A Self-Directed IRA (SDIRA) gives investors the ability to invest in alternative assets such as real estate, private lending, private equity, and even cryptocurrency—all while maintaining the same tax advantages available through traditional retirement accounts. For investors seeking greater diversification and control, learning how to self-direct an IRA may open the door to new opportunities. What Is a Self-Directed IRA? Quick Definition A Self-Directed IRA is a retirement account that allows the account holder to choose and direct their own investments rather than being limited to traditional brokerage products such as stocks, bonds, and mutual funds. Self-Directed IRAs can be structured as: Traditional IRAs Roth IRAs SEP IRAs SIMPLE IRAs The primary difference is not the tax treatment—it is the expanded investment flexibility available to the account holder. What Can You Invest in With a Self-Directed IRA? One of the biggest advantages of a Self-Directed IRA is access to a much broader universe of investments. Popular Self-Directed IRA Investments Real Estate Real estate remains one of the most popular alternative investments held within Self-Directed IRAs. Examples include: Single-family rentals Multifamily properties Commercial real estate Land investments Real estate syndications Private Lending Many investors use Self-Directed IRAs to participate in private lending opportunities through: Real estate-backed loans Promissory notes Private credit investments Secured lending arrangements Private Equity and Startups Investors may also use Self-Directed IRAs to invest in: Private businesses Startup companies Venture capital opportunities Limited partnerships Cryptocurrency Certain custodians allow Self-Directed IRA investors to gain exposure to digital assets such as: Bitcoin Ethereum Other approved cryptocurrencies Precious Metals IRS-approved precious metals may also be eligible investments, including: Gold Silver Platinum Palladium Why Haven’t More Investors Heard About Self-Directed IRAs? Despite existing for decades, Self-Directed IRAs remain relatively unknown compared to traditional retirement accounts. One reason is that most large financial institutions focus primarily on traditional investment products. Alternative assets such as real estate, private notes, and private companies require specialized administration, custody, and compliance processes that many mainstream brokerage firms do not support. As a result, investors typically work with specialized Self-Directed IRA custodians who facilitate these alternative investments. Why Investors Choose Self-Directed IRAs Investors are increasingly looking for ways to diversify beyond traditional public markets. Key Benefits of Self-Directed IRAs Tax Advantages Depending on account type, investments may grow: Tax-deferred (Traditional IRA) Tax-free (Roth IRA) Greater Diversification Alternative assets can help investors reduce dependence on public market performance. More Control Investors decide where their retirement funds are allocated rather than selecting from a limited menu of investments. Access to Specialized Knowledge Many investors prefer investing in industries they understand, such as: Real estate Lending Small businesses Alternative assets Self-Directed IRA Investment Trends Recent industry data shows investors continue to allocate retirement assets across a diverse range of alternatives. Popular Asset Categories Investment Type Approximate Share Single-Family Real Estate 28.8% Cryptocurrency 17.7% Private Lending 17.7% Private Equity & Small Business 10.9% These trends demonstrate growing interest in investment opportunities outside traditional Wall Street products. How to Self-Direct Your IRA The process is often more straightforward than many investors expect. Step 1: Open a Self-Directed IRA Select a qualified Self-Directed IRA custodian and establish your account. Choose the structure that best fits your goals: Traditional IRA Roth IRA SEP IRA SIMPLE IRA Solo 401(k) Health Savings Account (HSA) Step 2: Fund Your Account Funding may occur through: Annual contributions IRA transfers 401(k) rollovers Other retirement account transfers Step 3: Identify an Investment Research and evaluate investment opportunities that align with your objectives and risk tolerance. Step 4: Direct the Investment Your custodian handles the transaction based on your instructions while helping maintain compliance requirements. Step 5: Allow Income to Flow Back Into the IRA Rental income, interest payments, dividends, and gains generally return directly to the retirement account, preserving its tax-advantaged status. Understanding Prohibited Transactions While Self-Directed IRAs offer flexibility, they remain subject to IRS rules. Examples of Prohibited Transactions Generally, you may not: Purchase property you already own Personally use IRA-owned property Conduct certain transactions with disqualified family members Receive direct personal benefits from IRA assets Failure to follow IRS guidelines could jeopardize the account’s tax advantages. Advanced Strategy: The Checkbook IRA LLC Some experienced investors choose to establish an IRA-owned LLC, often referred to as a Checkbook IRA. Potential Benefits Direct control over investment activity Faster transaction execution Greater privacy Simplified management of multiple investments This structure is particularly popular among active real estate investors and entrepreneurs. Because these arrangements involve additional complexity, investors should consult qualified legal, tax, and retirement professionals before implementation. Is a Self-Directed IRA Right for You? A Self-Directed IRA may be worth exploring if you: Want greater control over retirement investments Understand alternative assets Seek diversification beyond public markets Have experience evaluating private investments Prefer a hands-on approach to retirement planning Like any investment strategy, proper due diligence and risk management are essential. Frequently Asked Questions Can I buy real estate in a Self-Directed IRA? Yes. Many investors use Self-Directed IRAs to purchase rental properties, commercial real estate, land, and other eligible real estate investments. Can I invest in cryptocurrency through a Self-Directed IRA? Certain Self-Directed IRA custodians allow investors to hold cryptocurrency within qualified retirement accounts. What are the tax benefits of a Self-Directed IRA? Traditional SDIRAs may provide tax-deferred growth, while Roth SDIRAs may provide tax-free qualified withdrawals. Can I manage my own Self-Directed IRA investments? Yes. Investors direct investment decisions while custodians handle administration and compliance. What is a Checkbook IRA? A Checkbook IRA uses an IRA-owned LLC structure that may provide investors with more direct control over investment transactions. Take Control of Your Retirement Strategy A Self-Directed IRA can provide access

How to Self-Direct Your IRA and Take Control of Your Retirement Read More »

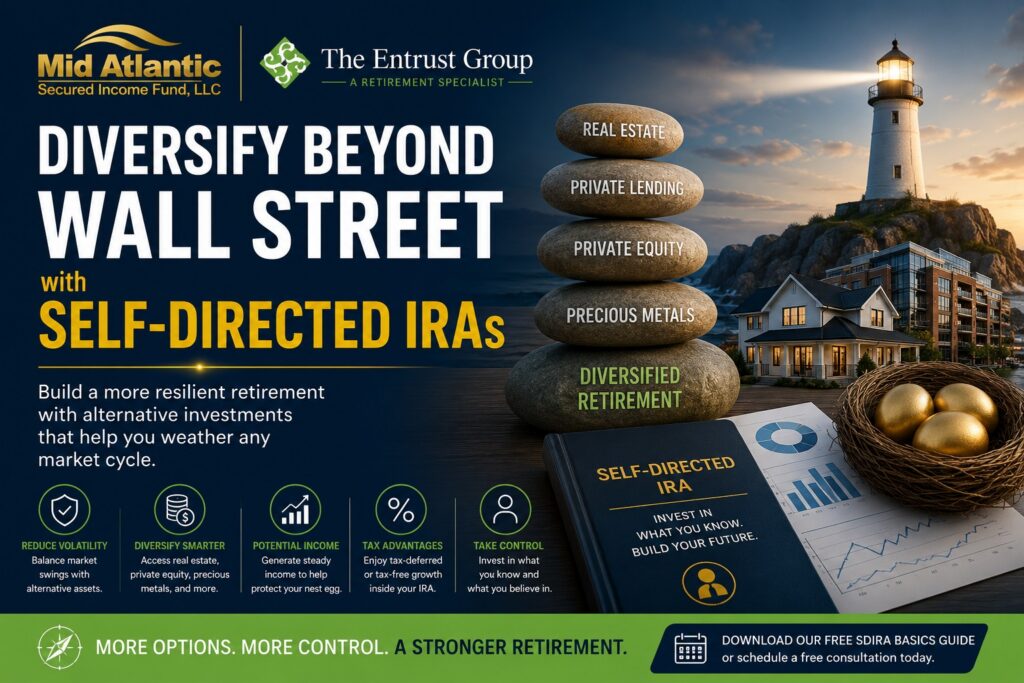

Why More Retirement Investors Are Diversifying Beyond Wall Street with Self-Directed IRAs The last few years have been a wild ride for public markets. We’ve seen record-setting tech booms, sudden crashes during COVID, and inflation-driven volatility that rattled even seasoned investors. For retirement savers, these swings can be unnerving. When your portfolio relies solely on Wall Street, your financial future is at the mercy of unpredictable market cycles. If you’re decades away from retirement, you may have time to recover from downturns. But as you get closer to retirement age, those sharp drops become harder to stomach—and harder to recover from. That’s why so many investors value stability and diversification. By expanding your retirement portfolio beyond publicly traded stocks and bonds, you could smooth out the highs and lows, protect your nest egg, and build a more resilient retirement plan. Why Diversification Matters You’ve probably heard the saying: “Don’t put all your eggs in one basket.” In investing, that’s the essence of diversification. It’s about spreading your money across different types of assets so that no single downturn can wipe out your progress. The challenge with standard retirement portfolios is that most public market assets move together during times of crisis. Stocks and bonds, which are supposed to balance each other, often correlate during sharp downturns, leaving investors exposed when they need stability most. For retirement savers, this volatility can have real consequences. If markets dip just before or during retirement, your account balance may shrink right when you need it to generate steady income. Fewer assets mean fewer years of security, and recovering from a major loss becomes much harder without the luxury of time on your side. SDIRAs: Opening the Door to Alternative Assets That’s where self-directed IRAs (SDIRAs) come in. An SDIRA is a type of retirement account that works just like a Traditional or Roth IRA in terms of tax benefits, but with one major difference: investment flexibility. Instead of being confined to mutual funds, ETFs, or a narrow slice of Wall Street, SDIRAs allow you to invest in any asset the IRS approves. This Can Include: Real estate (residential, commercial, or raw land) Private equity or startups Precious metals Promissory notes or private lending And much more By opening the door to these alternative assets, SDIRAs give investors a way to diversify beyond the ups and downs of public markets. You can put your expertise to work in areas you understand best, while still enjoying the tax-deferred or tax-free growth of an IRA. The Power of Diversification in Action Let’s put diversification into perspective with a simple scenario. Imagine two investors, each with a $250,000 retirement portfolio. Investor A Keeps 100% of their funds in the stock market. During strong years, their account grows quickly. But when the market dips (say, during a recession), they can lose tens of thousands in a matter of months. If a major downturn hits right before retirement, Investor A may be forced to delay retirement or reduce withdrawals to avoid the depletion of their portfolio. Investor B Holds a self-directed IRA (SDIRA) with a diversified portfolio: 60% public market assets 40% alternative assets like real estate and private lending While their growth during bull markets may not always match Investor A’s highs, their portfolio is far less vulnerable during downturns. The steady income or loan repayments from their alternative assets provide consistent cash flow and help preserve principal. The Outcome When the market swings, Investor A rides the rollercoaster—big gains followed by painful drops. Investor B, however, experiences steadier, more predictable growth. That stability can be crucial when approaching or living in retirement, ensuring they can count on a reliable income stream without worrying about timing the market. Tax Advantages of Using an SDIRA for Alternatives SDIRAs offer all of the same tax advantages as any other IRA. Traditional SDIRA With a Traditional SDIRA, your gains grow tax-deferred, meaning you won’t owe taxes until you take distributions in retirement. Roth SDIRA With a Roth SDIRA, qualified gains may grow entirely tax-free, letting you keep more of your returns. In either case, by keeping alternative investments inside a retirement account, you could shield your profits from annual taxation, allowing rental income, loan repayments, or private equity gains to compound faster over time. Risks & Considerations Of course, alternative investing comes with its own responsibilities. Liquidity Unlike stocks or bonds, real estate or private equity can’t always be sold quickly. Plan for the long term. Due Diligence With fewer disclosures than public companies, you must carefully vet each opportunity. Compliance The IRS has strict rules about prohibited transactions. Asking thorough questions of a knowledgeable custodian like The Entrust Group can help you stay compliant and avoid costly mistakes. Diversify Smarter with an SDIRA Market volatility isn’t going away. The question is whether your retirement portfolio is prepared to handle it. Diversification through a self-directed IRA allows you to balance Wall Street exposure with real estate, private equity, precious metals, and more—helping you weather downturns while building long-term stability. Ready to Explore How SDIRAs Could Fit Into Your Retirement Strategy? Download our free SDIRA Basics Guide for a step-by-step introduction. Or schedule a free consultation with an Entrust specialist to talk through your diversification options. Your future deserves more than just riding the ups and downs of the market. With the right tools, you can take control.

Achieving True Diversification in Your Retirement Portfolio Read More »

Top Self-Directed IRA Trends Driving Growth Through 2025 The self-directed IRA landscape continues to evolve as investors seek greater control, diversification, and access to non-traditional assets. With macroeconomic pressures like inflation, volatile public markets, and changing tax policy shaping retirement strategies, the Top Self-Directed IRA Trends Driving Growth Through 2025 offer a unique solution: tax-advantaged investing with the flexibility to pursue alternative assets that align with an investor’s goals and expertise. Broader Adoption of Alternative Assets One of the defining features of SDIRAs is the ability to invest in alternative assets. In both 2024 and 2025, investor interest has surged in opportunities that go beyond stocks and bonds—particularly among those with knowledge in specific asset classes. Common investment types include: Private real estate (residential and commercial) Private equity or private debt Precious metals Cryptocurrency held via compliant custodians Crowdfunded business ventures Crowdfunding platforms Self-directed IRAs are not a new topic. In fact, they have been around since 1974. With the rise of accessible information, more investors are learning their options can be more than only what the stock market has to offer. For those seeking opportunities to secure monthly passive income, self-directed IRAs can provide access to alternative investments that align with personal financial goals. Real Estate Strategies Shift in Response to Market Forces Real estate remains one of the most popular investment types within SDIRAs, but 2025 sees a notable shift in strategy beyond traditional single-family rentals: Multi-family and co-living arrangements, which address the growing demand for affordable housing. Flex spaces and shared work environments, responding to the sustained rise of remote and hybrid work models International real estate opportunities in locations like Costa Rica, Portugal, and Mexico, particularly for tourism or rental income. Artificial Intelligence Fuels Smarter, Passive Investment Tools Artificial intelligence is rapidly influencing the way investors evaluate opportunities. By analyzing market patterns and reallocating assets automatically, more investors are being drawn into the predictive insights AI investing platforms have to offer. Growth in Social Impact-Aligned Investing Gains Grounds In 2025, more self-directed investors are using their accounts to align their retirement dollars with environmental or social priorities closer to their values. Affordable housing or community redevelopment Renewable energy infrastructure Sustainable agriculture projects Demographics and Legislative Updates Supporting Growth Younger investors are increasingly aware of alternative investment options and are beginning to leverage SDIRAs to pursue them. Additionally, updates under SECURE 2.0 in 2025—including enhanced catch-up contribution allowances—offer greater flexibility and higher savings thresholds for older investors. Millennials and Gen X are entering their peak investing years and are more open to alternatives than older generations. Catch-up contribution limits expanded in 2025 under SECURE 2.0, allowing those aged 60-63 to contribute an additional $10,000 annually. The Department of Labor and IRS continue to provide clarifications on alternative asset custody, especially regarding digital assets and foreign holdings. Passive Syndications and Private Funds on the Rise While direct real estate ownership remains popular, professionally managed private placements—including private equity funds, real estate syndications, and private debt funds—are on the rise. Drivers of Growth: A growing number of Investors prefer passive structures that don’t require hands-on property management. More fund sponsors are designing offerings specifically for SDIRA eligibility. These structures appeal to investors who want diversification without the demands of day-to-day management. As always, it’s crucial to evaluate tax considerations such as unrelated business taxable income (UBTI) or unrelated debt-financed income (UDFI). Check out this resource that includes information about how to calculate UBIT & UDFI, if it were to occur. Cryptocurrency: Still Niche, But Still Here For a Reason Despite a volatile history, cryptocurrency remains a niche but persistent interest among SDIRA investors. In 2025, it’s important to understand these key points when using a self-directed IRA to invest in cryptocurrency: Digital assets must be held through a qualified administrator or exchange. Personal wallets or self-custody are strictly prohibited to avoid disqualification. Accurate documentation and reporting are essential. Final Thoughts: Looking Ahead to Late 2025 and Beyond The SDIRA market in 2025 reflects a maturing landscape—defined by greater investor control, expanding access to alternative assets, and the growing need for diversification amid a changing economic landscape. To stay ahead, investors should: Stay current with evolving IRS and regulatory guidance Perform in-depth due diligence on all investment opportunities Partner with an experienced IRA Administrator and trusted professionals.

The Top Self Directed IRA Trends Driving Growth Through 2025 and Beyond Read More »

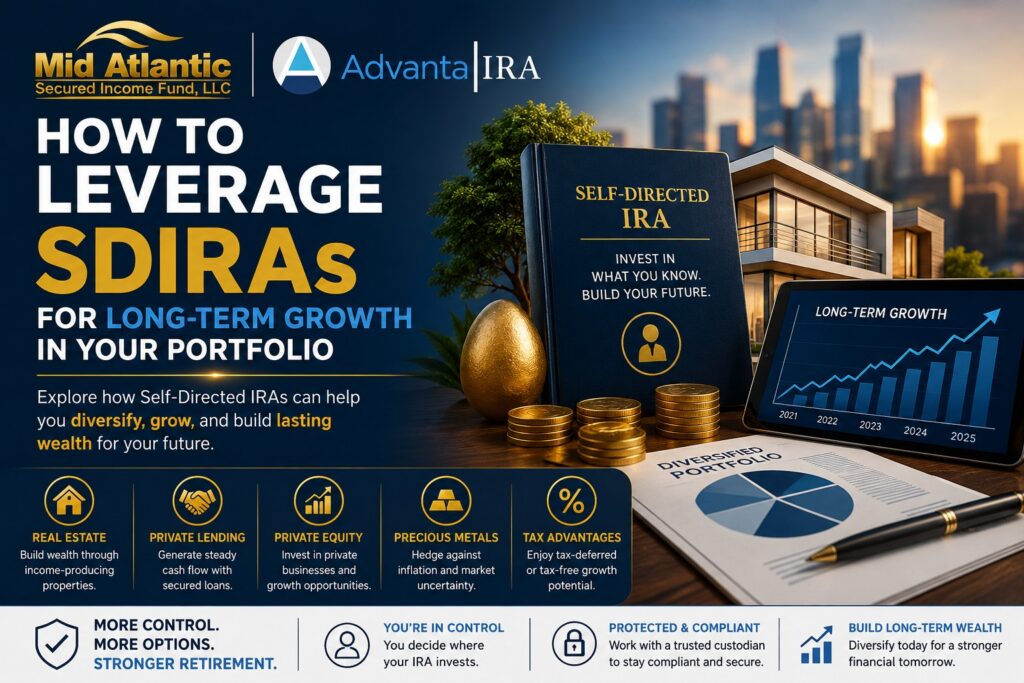

Leverage SDIRAs for Long-Term Portfolio Growth Traditional retirement plans limit investors to stocks, bonds, and mutual funds—but what if you could unlock an entirely new asset class—one that offers diversification, control, and high-return potential? With a Self-Directed IRA (SDIRA), you can. This powerful retirement tool allows you to invest in alternative assets such as real estate, private lending, and private equity—strategies that sophisticated investors have used for decades to build wealth and preserve capital. Leverage SDIRAs for Long-Term Portfolio Growth to broaden your investment strategy and take control of your financial future. Investors who want to take a hands-on approach to their retirement portfolio can leverage these unique options to diversify their holdings and enhance potential returns. You can choose assets that align with your expertise and long-term wealth-building goals—whether that means exploring real estate, private equity, or opting to invest your IRA in private credit, a growing alternative favored for its income potential and stability.. Using Self-Directed IRAs as a Long-Term Growth Strategy Investors who use self-directed IRAs for long-term growth often focus on alternative assets that have the potential to provide stability, cash flow, and appreciation over time. Below are familiar and unique strategies self-directed investors use to achieve their goals through alternative investments. Remember, traditional retirement accounts held with mainstream custodians often do not allow these alternative options. SDIRAs give investors an edge above the rest in reaching long-term growth in their retirement portfolios. 6 Common Alternative Investments Private Equity and Private Placements Investing in private equity for companies and startups can provide a unique opportunity for potentially substantial returns. Many high-net-worth individuals allocate a portion of their portfolios to private equity, taking advantage of early-stage investments in businesses poised for growth. Example: An SDIRA investor allocates $200,000 into a PE fund specializing in biotech startups. The fund holds investments for 8 years, eventually selling a high-growth company to a larger pharmaceutical firm, generating a 4x return. Private placements—such as pre-IPO stock, venture capital funds, and direct investments in companies—allow SDIRA holders to access high-value opportunities beyond publicly traded markets. Example: An SDIRA investor participates in a private placement real estate fund with a 5-year term. The fund invests in multifamily properties, generating quarterly income distributions and returning principal upon asset liquidation at year 5. Real Estate Syndications Real estate remains one of the most sought-after asset classes for SDIRA investors. Syndications are passive investments, providing a way to invest in large-scale commercial properties, multifamily units, self-storage facilities, and other real estate ventures. By pooling capital with other investors, SDIRA holders can participate in high-value projects without the need for active management. Example: An SDIRA investor allocates $150,000 into a multifamily real estate syndication with a 5-year hold period. The investment provides quarterly distributions of 8% annualized returns plus a projected 2x equity multiple at the end of year 5 when the property is refinanced or sold. Private Lending Private lending through an SDIRA offers investors a steady, tax-advantaged income stream while maintaining asset-backed security. Unlike traditional lending institutions, private lenders—such as Mid Atlantic Secured Income Fund—work directly with borrowers to provide flexible financing solutions. These loans are typically secured by real estate, making them an attractive low-volatility investment option within an SDIRA portfolio. Example: A self-directed IRA investor lends $100,000 to a real estate fix-and-flip investor at 10% annual interest, secured by the property. The borrower completes the renovation and repays the loan in 12 months, earning the investor $10,000 in tax-advantaged interest income. Impact Investments and Sustainable Ventures A growing number of investors seek opportunities that align with their values. Impact investing—focusing on ESG (environmental, social, and governance) initiatives—allows SDIRA holders to support businesses and projects that generate financial returns while positively impacting society. Example: An SDIRA investor places $200,000 into a solar energy infrastructure fund that finances commercial solar farms. The fund distributes 7% annual returns from power purchase agreements with corporations and municipalities. Precious Metals Gold, silver, platinum, and palladium have long been favored as hedges against inflation and economic uncertainty. Gold, silver, platinum, and palladium investments for SDIRAs must meet certain fineness and other specifications for precious metal investments in retirement plans. These assets provide long-term appreciation and portfolio diversification. Example: An SDIRA investor allocates $50,000 into gold bullion during an economic downturn. Over the next seven years, as inflation rises, gold’s value increases by 30%, allowing the investor to preserve and grow their retirement savings in a stable, tangible asset. Hard Assets Besides real estate and precious metals, SDIRA holders invest in tangible assets oil and gas investments, farmland, and timberland. The goal is to create potential hedges against inflation, stock market volatility, and economic downturns. Example: An investor uses $75,000 from their SDIRA to buy agricultural land leased to a local organic farm. The land generates annual lease income, capturing appreciation over time. After 8 years, the investor sells the land for $140,000, nearly doubling their initial investment while enjoying steady passive income along the way. Lesser-Known Tangible Assets that Facilitate Long-Term Growth Equipment leasing: Investors can purchase industrial machinery, construction equipment, medical devices, or agricultural machinery and lease them to businesses for a steady income stream. Mineral rights and royalties: Investors can own the rights to extract natural resources like oil, gas, or minerals, earning royalty payments when companies extract resources from their land. Livestock and agriculture: Some investors purchase cattle, horses, or other livestock as investment assets. Additionally, investing in crops and agribusiness (such as vineyards or organic farms) can generate passive returns. Commodities (beyond precious metals): While gold and silver are common, other commodities like platinum, palladium, and industrial metals (copper, nickel, etc.) are permissible in SDIRAs. Infrastructure: Investing in toll roads, renewable energy projects (solar or wind farms), or other public-private infrastructure projects can provide stable returns over time. Water rights and conservation: Some investors buy water rights, which allow them to lease access to businesses, farmers, or municipalities in need of water sources. Shipping containers: Investors can purchase shipping containers and lease them to

How to Leverage SDIRAs for Long-Term Growth in Your Portfolio Read More »

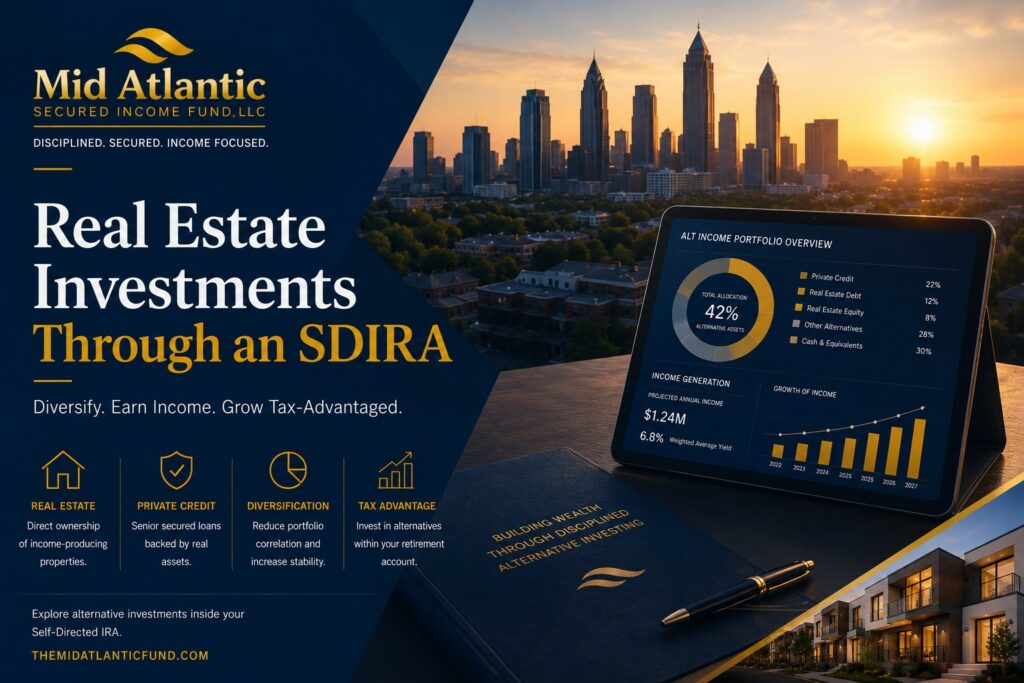

The Retirement Landscape Has Changed For decades, retirement investing in the United States revolved around a familiar framework: public equities, mutual funds, target-date funds, and traditional fixed income products. The conventional 60/40 portfolio dominated retirement planning conversations across wealth management firms, pension consultants, and retail brokerage platforms. But the investing environment entering 2026 looks materially different from the one many retirees prepared for. Persistent inflation concerns, elevated market volatility, compressed equity valuations, interest rate uncertainty, and growing concerns around sequence-of-return risk have pushed many investors to reconsider how retirement capital should be allocated. At the same time, institutional investors—including pension funds, sovereign wealth funds, endowments, and family offices—have steadily increased allocations to alternative investments and private markets. Increasingly, accredited investors are asking a similar question: What if retirement portfolios could access the same types of investments institutional investors use? That question has accelerated interest in high return SDIRA investments—particularly investments tied to private credit, real estate-backed lending, alternative income strategies, and asset-backed private debt. Self-directed IRAs (SDIRAs) are no longer viewed as niche vehicles reserved for specialized investors. They are becoming increasingly relevant in a market where diversification, downside protection, and durable income matter more than ever. What Is a Self-Directed IRA (SDIRA)? Direct Answer A self-directed IRA (SDIRA) is a retirement account that allows investors to allocate capital beyond traditional stocks, bonds, and mutual funds into alternative assets such as real estate, private credit, private equity, and other non-traditional investments. Unlike standard brokerage IRAs, SDIRAs provide significantly broader investment flexibility. Permitted investments may include: Private debt funds Real estate-backed lending Commercial real estate Multifamily developments Mortgage notes Alternative income funds Tax liens Private businesses Venture capital Structured lending opportunities The tax treatment generally mirrors traditional or Roth IRA structures depending on account type. Why High Net Worth Investors Are Increasingly Using SDIRAs The rise of SDIRAs is closely tied to broader institutional investing trends. According to alternative investment research from Preqin and BlackRock, institutional allocations to private markets have expanded dramatically over the past decade. Family offices and pension funds have increasingly sought investments that offer: Lower correlation to public markets Predictable cash flow Inflation resilience Asset-backed collateral structures Enhanced diversification Income generation outside traditional bond markets Retail retirement portfolios, by contrast, often remain concentrated in public equities and traditional fixed income products. Sophisticated investors increasingly recognize that concentration risk can become particularly problematic during periods of elevated market volatility. This shift has accelerated interest in SDIRA structures that enable exposure to private market opportunities traditionally associated with institutional capital. Why Traditional Retirement Portfolios Face New Challenges The Bond Market Is No Longer What It Once Was For decades, bonds provided investors with both income and diversification benefits. However, the macroeconomic environment changed significantly after the 2020–2024 period. Key structural pressures include: 1. Inflation Risk Even moderate inflation materially impacts purchasing power over long retirement horizons. According to U.S. Bureau of Labor Statistics data, cumulative inflation since 2020 has significantly eroded the real value of fixed retirement income streams. 2. Interest Rate Volatility Rapid interest rate adjustments created meaningful volatility in traditional bond portfolios. Long-duration bonds experienced substantial price declines during tightening cycles, surprising many investors who historically viewed bonds as stable portfolio anchors. 3. Correlation Risk Historically, stocks and bonds often moved inversely. But during certain inflationary environments, both asset classes may decline simultaneously—reducing diversification benefits. 4. Sequence-of-Return Risk For retirees drawing income, large early retirement losses can materially impair long-term portfolio sustainability. This has increased demand for alternative income-producing assets with lower public market correlation. What Are High Return SDIRA Investments? Direct Answer High return SDIRA investments are alternative assets held within a self-directed IRA that seek enhanced returns, income generation, diversification, or inflation resilience compared to traditional retirement investments. Common categories include: Investment Type Potential Objective Private Credit Funds Income generation Real Estate Debt Asset-backed cash flow Multifamily Lending Inflation-linked collateral Commercial Bridge Loans Short-duration income Secured Income Funds Passive income Mortgage Notes Yield enhancement Alternative Real Estate Diversification Private Equity Long-term growth Structured Credit Portfolio stabilization Importantly, higher return potential generally involves higher risk and reduced liquidity relative to publicly traded securities. Why Private Credit Has Become One of the Fastest Growing Alternative Asset Classes Private credit has emerged as one of the fastest-growing institutional asset classes globally. According to Preqin and IMF research, global private credit assets under management have expanded significantly over the past decade as banks reduced certain lending activities following post-2008 regulatory reforms. This created opportunities for non-bank lenders and private debt funds. Why Investors Are Drawn to Private Credit Private credit strategies often emphasize: Senior secured lending Contractual income streams Collateral-backed structures Floating-rate protections Lower public market correlation Shorter duration exposure These characteristics have become increasingly attractive during periods of market uncertainty. For SDIRA investors, private credit can offer exposure to institutional-style lending strategies within a tax-advantaged retirement account structure. How Real Estate-Backed Lending Works Inside an SDIRA Direct Answer Real estate-backed lending involves loans secured by physical real estate collateral. Investors may gain exposure through private debt funds, mortgage funds, or direct lending structures held within a self-directed IRA. Common collateral may include: Residential real estate Multifamily properties Commercial buildings Development projects Bridge financing Construction lending The underlying concept is relatively straightforward: The investment generates income through borrower interest payments while maintaining collateral protections tied to real estate assets. This differs materially from unsecured investments whose valuations depend solely on market sentiment or earnings multiples. Why Accredited Investors Often Prioritize Alternative Income Investments Accredited investors frequently face different portfolio construction challenges than average retail investors. Once investors achieve meaningful net worth, preserving purchasing power and generating reliable income often become as important as maximizing pure growth. As a result, many high-net-worth investors focus on: Diversification across asset classes Income durability Capital preservation Tax efficiency Lower volatility strategies Inflation resilience Estate planning considerations Alternative investments may help address some of these objectives when appropriately structured within a diversified portfolio. Are SDIRA Investments Safer Than Stocks? Direct Answer SDIRA investments

Retirement Investing Is Undergoing a Structural Shift For decades, retirement investing largely revolved around public markets. Traditional retirement portfolios were commonly built using combinations of: Public equities Mutual funds ETFs Corporate bonds Treasury securities Target-date retirement products While these structures remain foundational components of many portfolios, investors entering 2026 increasingly recognize a fundamental reality: Public market exposure alone may no longer provide sufficient diversification, income resilience, or inflation protection for long-term retirement objectives. This shift has accelerated interest in alternative investments—and particularly in direct real estate investments through SDIRAs. Self-directed IRAs (SDIRAs) have emerged as one of the fastest-growing vehicles for accredited investors seeking: Passive income Real asset exposure Portfolio diversification Inflation resilience Tax-advantaged growth Alternative investments outside traditional Wall Street products Increasingly, investors are asking a different type of retirement question: What if retirement capital could be allocated like institutional capital? That question is reshaping modern retirement portfolio construction. What Is a Self-Directed IRA (SDIRA)? Direct Answer A self-directed IRA (SDIRA) is a retirement account that allows investors to hold alternative assets beyond traditional publicly traded securities. Unlike standard brokerage IRAs, SDIRAs permit investments in: Real estate Private credit Mortgage notes Private debt funds Multifamily properties Commercial real estate Alternative income investments Real estate-backed lending Private businesses Certain structured alternative assets The tax structure generally mirrors traditional or Roth IRA frameworks while dramatically expanding investment flexibility. What Are Direct Real Estate Investments Through SDIRA? Direct Answer Direct real estate investments through SDIRAs involve using self-directed retirement accounts to invest in real estate assets or real estate-backed investments rather than limiting retirement savings to stocks and bonds. Common SDIRA real estate strategies include: Strategy Typical Objective Rental Properties Cash flow & appreciation Multifamily Investments Income diversification Private Real Estate Funds Passive exposure Mortgage Notes Fixed income generation Real Estate Debt Funds Asset-backed yield Bridge Lending Short-duration income Construction Lending Higher yield opportunities Commercial Real Estate Inflation-linked income Real Estate Syndications Passive alternative investing These investments may provide both diversification and access to alternative income streams not typically available within standard retirement accounts. Why Real Estate Has Become Central to Modern Portfolio Diversification Institutional investors have long viewed real estate as a core portfolio allocation. According to research from BlackRock, McKinsey, and Preqin, institutional capital increasingly allocates to private real assets because of several characteristics: Inflation sensitivity Tangible asset backing Income generation potential Lower correlation to public equities Long-duration wealth preservation Portfolio diversification benefits Many sophisticated investors are now seeking similar exposure through SDIRAs. Why Traditional Retirement Portfolios Face New Pressures The retirement investing environment entering 2026 differs significantly from prior decades. Several structural forces are reshaping portfolio construction: 1. Inflation Concerns Persistent inflation materially impacts retirement purchasing power over long time horizons. Even moderate inflation compounds significantly over decades. According to Bureau of Labor Statistics data, cumulative inflation since 2020 has meaningfully increased retirement income pressure for many households. 2. Equity Market Volatility Public equity valuations remain vulnerable to: Interest rate uncertainty Slowing earnings growth Geopolitical instability Liquidity tightening Recession concerns Investors increasingly recognize the need for non-correlated income streams. 3. Bond Market Challenges Traditional fixed income strategies experienced unusual volatility during recent rate cycles. Long-duration bond portfolios faced price declines that surprised many investors accustomed to bonds serving as stable portfolio anchors. 4. Longevity Risk Retirees today may need portfolios capable of supporting income needs for 25–35 years or longer. This increases the importance of durable cash flow and long-term purchasing power protection. Why Investors Are Turning to Real Assets Real assets—including real estate—often behave differently from purely financial assets. Unlike many securities whose valuations depend heavily on market sentiment, real estate investments are tied to physical assets and economic utility. This distinction matters. Sophisticated investors increasingly prioritize: Tangible collateral Income-producing assets Inflation-linked cash flows Asset-backed investment structures Real estate investments may help address several of these priorities simultaneously. How SDIRA Real Estate Investing Works The mechanics of SDIRA investing differ from standard brokerage retirement accounts. Step 1: Establish a Self-Directed IRA The investor opens an SDIRA through a qualified custodian specializing in alternative assets. Step 2: Fund the Account Funding may occur through: IRA transfers 401(k) rollovers Contributions Existing retirement assets Step 3: Select Alternative Investments The SDIRA can then allocate capital toward permitted alternative investments. Step 4: Income and Growth Remain Within the IRA Rental income, interest payments, or investment gains typically remain inside the retirement account structure. Tax treatment depends on whether the account is structured as a Traditional SDIRA or Roth SDIRA. Why Accredited Investors Are Increasingly Using SDIRAs High-net-worth investors often seek broader diversification than conventional retirement products provide. Increasingly, sophisticated investors are allocating capital toward: Private credit Real estate debt Alternative income funds Real estate-backed lending Structured credit Asset-backed investments The appeal is not merely return potential. Rather, many investors seek: Diversification Capital preservation Passive income Inflation resilience Reduced public market correlation Direct Real Estate Ownership vs Real Estate Debt Exposure Not all real estate investing operates the same way. Understanding the distinction between equity and debt exposure is critical. Direct Equity Ownership Examples: Rental properties Multifamily ownership Commercial buildings Potential advantages: Appreciation upside Tax advantages Long-term inflation hedge Potential risks: Operational complexity Vacancy exposure Market cycles Maintenance costs Real Estate Debt Investments Examples: Mortgage funds Bridge lending Construction lending Secured income funds Potential advantages: Contractual income Senior lien positioning Reduced operational burden Asset-backed structures Potential risks: Credit risk Underwriting risk Liquidity constraints Sophisticated portfolios often incorporate both approaches strategically. Why Passive Income Matters More in Retirement Planning Retirement investing increasingly emphasizes income durability rather than purely maximizing growth. Many investors entering retirement prioritize: Monthly income stability Reduced portfolio volatility Inflation-adjusted cash flow Long-term sustainability This is one reason private credit and real estate-backed lending strategies continue gaining traction among retirement investors. Are Real Estate Investments Safer Than Stocks? Direct Answer Real estate investments are not inherently safer than stocks. Risk depends on: Leverage levels Market conditions Asset quality Underwriting discipline Location Liquidity Management expertise However, some real estate investments may provide

The Evolution of Retirement Investing For decades, retirement investing in the United States largely revolved around a familiar framework: publicly traded stocks, mutual funds, index funds, ETFs, and traditional bond allocations. While these strategies remain foundational for many investors, the retirement landscape has changed substantially over the last twenty years. Persistent inflation pressures, market volatility, demographic shifts, and concerns surrounding long-term purchasing power have pushed many high-net-worth investors to explore alternative retirement investment strategies. One of the fastest-growing approaches among sophisticated investors is the use of Self-Directed IRAs (SDIRAs) to access alternative assets — particularly real estate investments and private credit opportunities. Today, investors increasingly seek retirement portfolios that prioritize: diversification beyond public markets, inflation resilience, asset-backed income generation, lower correlation to equities, and long-term capital preservation. As institutional investors and family offices continue increasing allocations to private markets, accredited investors are increasingly adopting similar strategies within tax-advantaged retirement structures. What Is a Self-Directed IRA (SDIRA)? Direct Answer A Self-Directed IRA (SDIRA) is a retirement account that allows investors to hold alternative assets beyond traditional stocks, bonds, and mutual funds. Depending on IRS guidelines and custodian capabilities, SDIRAs may invest in: real estate, private credit, private funds, real estate debt, private lending, syndications, tax liens, and other alternative investments. Unlike conventional brokerage IRAs, SDIRAs provide broader investment flexibility. Why Investors Are Turning to SDIRAs The growth of SDIRA investing reflects broader macroeconomic trends. According to Federal Reserve data, retirement investors increasingly face concerns regarding: inflation-adjusted retirement income, equity market volatility, concentration risk, and longevity planning. At the same time, institutional capital continues flowing into alternative investments. According to Preqin, global alternative assets under management are projected to exceed $24 trillion by 2028, driven heavily by: private credit, real estate, infrastructure, and alternative income-producing investments. Many retirement-focused investors increasingly want access to these same categories inside tax-advantaged accounts. What Types of Real Estate Investments Can Be Held in an SDIRA? Common SDIRA Real Estate Investments Self-Directed IRAs may hold a wide range of real estate-related investments depending on custodian policies and IRS regulations. Direct Real Estate Ownership Examples include: single-family rental homes, multifamily properties, commercial real estate, industrial assets, land investments, and vacation rental properties. Real Estate Debt Investments Many investors prefer real estate debt over direct ownership due to: potentially reduced operational complexity, contractual income streams, and senior collateral positions. Examples include: bridge loans, private lending, mortgage notes, real estate debt funds, and secured lending investments. Real Estate Syndications SDIRAs may also participate in private real estate syndications involving: apartment communities, self-storage, industrial logistics, student housing, and mixed-use developments. Private Credit Funds Many accredited investors increasingly use SDIRAs to gain exposure to: senior secured private credit, asset-backed lending, and real estate-secured income strategies. Why Real Estate Investments Remain Attractive for Retirement Portfolios Inflation Protection Real estate has historically been viewed as a potential hedge against inflation. As inflation rises: replacement costs increase, rents may rise, and underlying asset values can adjust over time. According to the Federal Reserve and NAREIT research, commercial and residential real estate often demonstrate inflation-sensitive characteristics over longer investment cycles. Income Generation Many retirement investors increasingly prioritize income-producing investments. Real estate-related strategies may generate: rental cash flow, interest income, or contractual loan payments. This becomes particularly important for retirees seeking portfolio cash flow rather than purely appreciation-focused investing. Diversification Beyond Public Markets Real estate investments often behave differently than publicly traded equities. This lower correlation may improve portfolio diversification. Sophisticated investors increasingly recognize diversification as: Diversifying economic drivers — not simply owning more securities. Why Many Investors Prefer Real Estate Debt Over Direct Ownership While direct property ownership can offer appreciation potential, many investors increasingly prefer debt-oriented real estate strategies. Key Advantages of Real Estate Debt Strategies 1. Senior Positioning Debt investors often occupy a senior position within the capital stack. This may provide additional downside protection compared to equity ownership. 2. Contractual Income Debt structures typically involve contractual repayment schedules. This may create more predictable income streams than property appreciation strategies. 3. Lower Operational Burden Direct ownership may involve: maintenance, tenant management, leasing risk, and operational complexity. Debt-focused strategies may reduce these responsibilities. 4. Defined Investment Horizons Many private credit investments operate with defined maturities and repayment structures. How Accredited Investors Use SDIRAs for Alternative Investments The Institutional Shift Into Private Markets Family offices, pension funds, and institutional investors have substantially increased allocations to private markets over the last decade. According to BlackRock and McKinsey research: private credit has become one of the fastest-growing institutional asset classes, alternative investments continue gaining share within diversified portfolios, and income-focused private lending strategies remain in high demand. Accredited investors increasingly seek similar access through SDIRAs. Tax Advantages of SDIRA Investing Tax-Deferred or Tax-Free Growth Depending on account structure: Traditional SDIRAs may allow tax-deferred growth Roth SDIRAs may allow tax-free qualified distributions This can create meaningful long-term compounding advantages. Why Retirement Investors Are Seeking Alternative Income The Retirement Income Challenge Traditional retirement planning increasingly faces structural pressure from: longer life expectancy, inflation, lower historical bond yields, and market volatility. Many retirees now seek: diversified income streams, asset-backed investments, and alternative cash-flow-producing assets. Private credit and real estate-backed lending strategies have increasingly emerged within this conversation. Understanding the Risks of SDIRA Real Estate Investing All investments involve risk. Alternative investments may carry unique considerations. Key SDIRA Investment Risks Illiquidity Risk Private investments are typically less liquid than publicly traded securities. Real Estate Market Risk Property values may fluctuate based on: interest rates, economic conditions, demographic shifts, and regional market dynamics. Credit Risk Borrowers may default on loans or obligations. Regulatory & IRS Compliance Risk SDIRAs must follow IRS rules regarding: prohibited transactions, disqualified persons, and operational compliance. Investors should work closely with qualified custodians and tax professionals. What Sophisticated Investors Look for in SDIRA Custodians Choosing the right custodian is critical. Common Factors Investors Evaluate Alternative Asset Experience Not all custodians specialize in alternative investments. Sophisticated investors often prioritize custodians experienced with: real estate, private lending, private placements, and