The Return of Income-Focused Investing

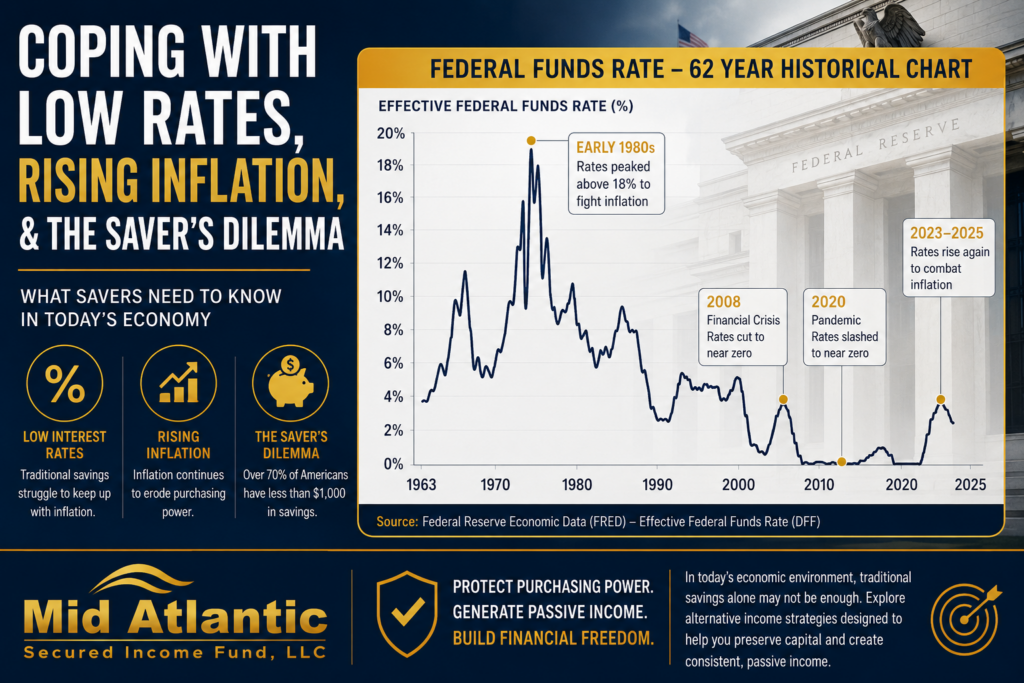

For much of the decade following the Global Financial Crisis, investors operated in a low-interest-rate environment where traditional fixed income struggled to provide meaningful income. U.S. Treasury yields remained historically compressed, investment-grade bonds often failed to keep pace with inflation, and many retirees were pushed further out on the risk spectrum in search of yield.

That environment has changed materially.

Rising interest rates, persistent inflation concerns, higher market volatility, and shifting macroeconomic conditions have brought fixed income investing back into focus—not merely as a defensive allocation, but as a core portfolio construction strategy.

Today’s investors are increasingly evaluating a broader universe of fixed income investment options, including:

- Treasury securities

- Municipal bonds

- Corporate credit

- Private credit

- Real estate debt funds

- Structured income strategies

- Asset-backed lending

- Alternative income-producing investments

At the same time, institutional investors, family offices, and accredited investors are rethinking what fixed income means in a modern portfolio.

Increasingly, the conversation is no longer simply about “bonds.” It is about:

- income durability,

- downside management,

- portfolio diversification,

- inflation resilience,

- and risk-adjusted returns.

This evolution has contributed to rapid growth across alternative credit markets and private lending strategies.

According to Preqin, global private debt assets under management surpassed approximately $1.6 trillion in recent years, reflecting institutional demand for floating-rate, collateral-backed, and income-oriented investment structures.

For investors seeking dependable income streams while balancing portfolio risk, understanding the full spectrum of fixed income investment options has become increasingly important.

What Are Fixed Income Investment Options?

Direct Answer

Fixed income investment options are investments designed primarily to generate predictable income payments through interest, distributions, or contractual cash flow obligations. These investments typically prioritize income generation, capital preservation, and lower volatility relative to growth-oriented equities.

Common fixed income investment options include:

- Treasury bonds

- Municipal bonds

- Corporate bonds

- Certificates of deposit (CDs)

- Preferred securities

- Private credit funds

- Mortgage-backed securities

- Real estate debt funds

- Asset-backed lending strategies

Unlike stocks, which represent equity ownership and depend heavily on appreciation, fixed income investments are generally contractual obligations where investors receive scheduled payments over time.

Why Investors Allocate to Fixed Income

Fixed income serves multiple strategic purposes inside diversified portfolios.

1. Income Generation

The most obvious function is consistent income.

Many investors—particularly retirees and income-focused households—seek investments capable of generating:

- monthly income,

- quarterly distributions,

- predictable cash flow,

- or interest payments.

This can help support:

- retirement spending,

- reinvestment strategies,

- philanthropic goals,

- or wealth preservation planning.

2. Portfolio Diversification

Historically, fixed income has provided diversification benefits relative to equities.

While correlations vary depending on the macroeconomic environment, fixed income investments have traditionally helped:

- reduce overall portfolio volatility,

- cushion equity drawdowns,

- stabilize portfolio performance during recessions,

- and improve risk-adjusted returns.

This is particularly relevant for investors approaching retirement or managing substantial wealth.

3. Capital Preservation

Many fixed income investors prioritize:

- lower volatility,

- contractual repayment structures,

- seniority in capital stacks,

- and asset-backed collateral.

While no investment is risk-free, certain fixed income structures may offer stronger downside protections than pure equity investments.

For example:

- senior secured debt often has repayment priority ahead of common equity,

- collateral-backed lending may provide recovery support,

- and shorter-duration instruments may reduce interest-rate sensitivity.

Major Categories of Fixed Income Investments

U.S. Treasury Securities

Treasuries remain one of the most recognized fixed income investments globally.

Issued by the U.S. government, Treasury securities include:

- Treasury bills,

- Treasury notes,

- Treasury bonds,

- and Treasury Inflation-Protected Securities (TIPS).

Advantages

- High liquidity

- Strong credit quality

- Government backing

- Transparent pricing

Risks

- Inflation risk

- Interest-rate risk

- Lower yields relative to alternative credit

During periods of elevated inflation, real returns on Treasuries can become challenged.

Corporate Bonds

Corporate bonds allow investors to lend capital to businesses in exchange for interest payments.

These range across:

- investment-grade bonds,

- high-yield bonds,

- floating-rate credit,

- and subordinated debt.

Investment-Grade Bonds

Issued by financially strong companies with relatively lower default risk.

Generally:

- lower yields,

- lower volatility,

- stronger credit ratings.

High-Yield Bonds

Higher yields compensate investors for elevated credit risk.

These may experience:

- greater price volatility,

- higher default probabilities,

- increased recession sensitivity.

According to Moody’s and S&P Global, default cycles can accelerate meaningfully during economic contractions.

Municipal Bonds

Municipal bonds are debt obligations issued by states, cities, or municipalities.

They are often attractive to high-income investors because:

- interest income may be federally tax-exempt,

- some bonds may also offer state tax advantages.

Municipal bonds are commonly used by:

- retirees,

- high-net-worth households,

- tax-sensitive investors.

However, investors must still evaluate:

- issuer quality,

- pension liabilities,

- local economic conditions,

- and duration risk.

Certificates of Deposit (CDs)

CDs are deposit products issued by banks.

They offer:

- fixed interest rates,

- defined maturity dates,

- FDIC insurance within applicable limits.

While CDs may offer capital stability, they often provide limited growth potential after inflation and taxes.

Preferred Securities

Preferred securities occupy a hybrid position between debt and equity.

They often:

- pay higher yields,

- rank above common stock,

- but below senior debt obligations.

These instruments may be sensitive to:

- interest rates,

- issuer health,

- banking sector conditions.

What Is Private Credit?

Direct Answer

Private credit refers to non-bank lending strategies where capital is provided directly to borrowers outside traditional public bond markets.

Private credit may include:

- real estate lending,

- middle-market corporate lending,

- asset-backed lending,

- bridge financing,

- specialty finance,

- and senior secured debt strategies.

Institutional investors increasingly allocate to private credit because it may provide:

- enhanced yields,

- floating-rate exposure,

- reduced public market correlation,

- and collateral-backed structures.

The Growth of Private Credit Markets

Private credit has expanded significantly since the 2008 financial crisis.

As regulatory capital requirements tightened for traditional banks, non-bank lenders filled financing gaps across commercial real estate, middle-market lending, and specialty finance sectors.

According to Preqin and BlackRock research:

- private credit assets under management have grown rapidly over the past decade,

- institutional allocations continue increasing,

- and private wealth platforms are expanding access to alternative credit strategies.

Key drivers include:

- higher yields,

- customized lending structures,

- floating-rate characteristics,

- and diversification benefits.

Real Estate Debt Funds as Fixed Income Investments

Real estate debt funds have become increasingly important within alternative fixed income allocations.

Unlike equity real estate investing, debt-focused real estate strategies prioritize:

- loan income,

- contractual interest payments,

- collateral-backed lending,

- and senior lien positioning.

Common Real Estate Debt Structures

- Bridge loans

- Construction lending

- Transitional real estate financing

- Multifamily lending

- Residential redevelopment financing

- Commercial mortgage lending

Why Accredited Investors Use Real Estate Debt Funds

Many accredited investors allocate to real estate-backed debt strategies because they may offer:

Asset-Backed Structures

Loans are often secured by physical real estate collateral.

Monthly or Quarterly Income

Certain private debt funds prioritize recurring distributions.

Reduced Equity Volatility

Debt-focused strategies may exhibit different risk profiles than direct equity ownership.

Potential Inflation Advantages

Floating-rate loans and shorter durations may help manage inflationary environments.

Are Debt Funds Safer Than Stocks?

Direct Answer

Debt funds are not inherently “safe,” but certain debt structures may offer lower volatility and stronger downside protections than equities due to contractual repayment obligations, seniority in the capital stack, and collateral-backed lending structures.

However, risks still exist, including:

- borrower default,

- illiquidity,

- interest-rate risk,

- and market downturns.

Investors should evaluate:

- underwriting quality,

- collateral coverage,

- manager experience,

- loan structures,

- and diversification.

Key Risks of Fixed Income Investments

Interest Rate Risk

Bond prices generally move inversely to interest rates.

Long-duration bonds may experience larger declines when rates rise.

Inflation Risk

Fixed payments lose purchasing power when inflation remains elevated.

This has become increasingly relevant following post-pandemic inflationary pressures.

Credit Risk

Borrowers may fail to repay obligations.

This risk varies substantially across:

- government debt,

- investment-grade credit,

- high-yield bonds,

- and private lending strategies.

Liquidity Risk

Private investments may be less liquid than publicly traded securities.

Investors should understand:

- redemption policies,

- lock-up periods,

- and portfolio liquidity structures.

How Institutional Investors Build Fixed Income Allocations

Large institutional portfolios rarely rely on a single fixed income category.

Instead, many use layered allocations including:

- public bonds,

- floating-rate loans,

- private credit,

- real estate debt,

- short-duration strategies,

- inflation-sensitive assets,

- and opportunistic income strategies.

This diversified approach may help:

- reduce concentration risk,

- stabilize income streams,

- improve risk-adjusted returns,

- and navigate changing rate environments.

Fixed Income Portfolio Construction Strategies

Laddering

Bond laddering staggers maturities over time.

Benefits may include:

- reduced reinvestment risk,

- improved liquidity,

- and interest-rate flexibility.

Barbell Strategy

Combines:

- short-duration holdings,

- with longer-duration yield-generating assets.

Used to balance:

- liquidity,

- duration exposure,

- and income generation.

Diversified Credit Allocation

Blends:

- government debt,

- corporate bonds,

- private credit,

- real estate debt,

- and alternative income strategies.

Increasingly common among sophisticated investors.

The Role of Fixed Income in Retirement Planning

Fixed income often becomes increasingly important as investors approach retirement.

Key objectives may include:

- income replacement,

- volatility reduction,

- portfolio preservation,

- and sequence-of-returns risk management.

Sequence risk refers to the danger of experiencing major portfolio losses early in retirement while withdrawing income.

Income-producing investments may help moderate this risk by reducing dependence on equity appreciation alone.

Fixed Income vs. Equities

|

Factor |

Fixed Income |

Equities |

|---|---|---|

|

Primary Goal |

Income generation |

Capital appreciation |

|

Volatility |

Typically lower |

Typically higher |

|

Cash Flow |

Contractual or scheduled |

Variable |

|

Upside Potential |

Generally capped |

Higher long-term upside |

|

Downside Protection |

Often stronger seniority |

Residual claim |

|

Inflation Sensitivity |

Moderate to high |

Mixed |

How Rising Rates Changed Fixed Income Markets

For years, investors questioned whether fixed income still offered meaningful value.

Higher rates have shifted that conversation.

Today:

- Treasury yields are materially higher than pandemic-era lows,

- private credit yields have expanded,

- floating-rate structures have become more attractive,

- and institutional investors are reassessing strategic fixed income allocations.

This changing environment has renewed interest in:

- income strategies,

- downside protection,

- and diversified alternative credit exposure.

What Sophisticated Investors Evaluate in Fixed Income Funds

Institutional investors often evaluate:

Underwriting Discipline

How conservative is the lending process?

Collateral Coverage

What backs the investment?

Historical Loss Performance

How has the manager navigated downturns?

Duration Profile

How sensitive is the portfolio to rate movements?

Diversification

Is exposure concentrated or diversified?

Alignment of Interests

Does management invest alongside investors?

Why Alternative Fixed Income Is Expanding

Alternative income investments continue gaining traction because traditional bond portfolios alone may not fully satisfy:

- yield objectives,

- diversification needs,

- inflation concerns,

- or income expectations.

As a result, private credit, real estate debt, and specialty finance have become increasingly mainstream among:

- family offices,

- RIAs,

- institutional allocators,

- and accredited investors.

The Evolution of Modern Income Investing

The definition of fixed income investing has expanded dramatically.

Historically, investors relied heavily on:

- government bonds,

- CDs,

- and traditional bond funds.

Today’s landscape includes:

- private lending,

- real estate-backed credit,

- structured income strategies,

- floating-rate debt,

- and alternative credit solutions.

This evolution reflects changing market realities:

- higher volatility,

- inflation pressures,

- demographic shifts,

- and increasing demand for durable income streams.

Final Thoughts

Fixed income investment options remain foundational to modern portfolio construction.

But today’s environment requires investors to think beyond traditional bonds alone.

Sophisticated income-oriented portfolios increasingly combine:

- public fixed income,

- private credit,

- real estate-backed lending,

- and diversified alternative income strategies.

For accredited investors, family offices, and long-term allocators, the focus is often less about chasing maximum returns and more about building resilient portfolios capable of generating durable income across changing market cycles.

That requires:

- disciplined underwriting,

- diversification,

- thoughtful risk management,

- and a long-term perspective.

As markets evolve, fixed income itself continues evolving alongside them.

FAQ Section

What are fixed income investment options?

Fixed income investment options are investments designed primarily to generate recurring income payments through interest or contractual cash flow obligations. Examples include bonds, Treasury securities, CDs, private credit funds, and real estate debt investments.

Are fixed income investments safer than stocks?

Fixed income investments may offer lower volatility and stronger downside protections than equities, but they are not risk-free. Risks include interest-rate risk, inflation risk, borrower default, and liquidity constraints.

What is private credit investing?

Private credit investing involves lending capital directly to borrowers outside traditional public bond markets. Strategies may include real estate lending, middle-market lending, bridge loans, and asset-backed financing.

Why are investors allocating to alternative fixed income?

Many investors seek higher yields, portfolio diversification, floating-rate exposure, and collateral-backed investment structures that may not be available through traditional bond portfolios.

How do real estate debt funds work?

Real estate debt funds provide financing secured by real estate collateral. Investors typically receive income generated through interest payments from borrowers.