A growing number of high-net-worth investors are asking a more practical question than how to maximize upside. They want to know how to generate dependable income without taking full equity-market risk or tying capital to assets they have to manage themselves. That is where alternative investments for accredited investors deserve a closer look, particularly for those prioritizing capital preservation, monthly cash flow, and lower correlation to public markets.

For many accredited investors, the issue is not access. It is selectivity. Private offerings, real estate deals, and specialty funds are widely available, but the dispersion in quality is significant. The difference between a disciplined income strategy and a speculative alternative often comes down to structure, underwriting, and how seriously the manager treats downside protection.

What accredited investors are really looking for

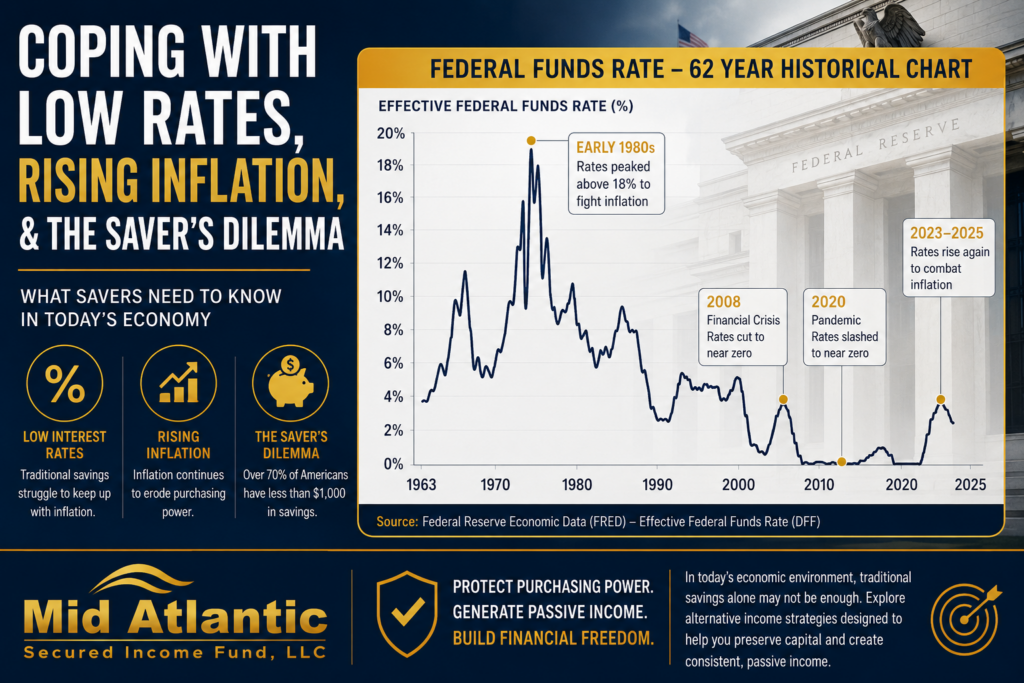

Most sophisticated investors do not pursue alternatives simply because they are private. They pursue them because traditional income options have become less predictable in real terms. Public bonds are interest-rate sensitive. Equities can produce income, but dividend strategies still carry market volatility and valuation risk. Cash equivalents provide liquidity, yet they may not meet long-term income needs after inflation and taxes.

That gap has pushed more accredited investors toward strategies built around contractual income, shorter durations, and tangible collateral. In practical terms, that often means private credit, real estate-backed lending, and other structures where return is driven by borrower payments rather than asset appreciation alone.

This distinction matters. An investment dependent on selling an asset at a higher valuation carries a different risk profile than one structured to generate current income from a borrower’s obligation to repay principal and interest. Both can have a place in a portfolio, but they serve different objectives.

Alternative investments for accredited investors by category

The broad alternative universe includes private equity, hedge funds, private credit, direct real estate, and niche asset strategies. For income-focused accredited investors, however, the most relevant comparison is often between equity-oriented alternatives and credit-oriented alternatives.

Private equity can offer meaningful upside, but it generally requires a longer hold period and a higher tolerance for illiquidity and valuation uncertainty. Returns may depend on business growth, recapitalizations, or eventual exits. Direct real estate ownership offers tax advantages and inflation sensitivity, but it can also involve leasing risk, operating costs, vacancy, and execution burdens.

Private credit tends to attract a different investor profile. It is often better suited to those who want current distributions, clearer loan-level economics, and a senior position in the capital stack. When that credit is backed by real estate, investors gain an additional layer of risk management through hard-asset collateral. That does not eliminate risk, but it can materially change the recovery profile compared with unsecured lending or equity speculation.

Why private credit stands out

Private credit has grown substantially over the last decade in part because banks have become more constrained in certain types of lending. That has created space for private lenders to finance transitional projects, bridge needs, redevelopment, and short-term business opportunities that require speed and structure.

For accredited investors, the appeal is straightforward. Loans are typically underwritten to specific collateral, repayment sources, and loan-to-value thresholds. Duration is often shorter than many private equity strategies. Income is generated through contractual interest payments rather than hoped-for future appreciation.

In a well-run real estate-backed private credit fund, underwriting discipline is the core product. Investors are not simply buying yield. They are relying on the manager’s ability to assess property value, borrower capacity, exit strategy, market conditions, and protective structuring before capital is deployed.

What to evaluate before committing capital

Not all alternative investments for accredited investors are built with the same priorities. A fund pursuing maximum return may use leverage aggressively, stretch on collateral quality, or move down the capital stack. Another may focus more narrowly on first-position loans, conservative loan-to-value ratios, and short-duration repayment timelines. Those are not cosmetic differences. They shape the entire risk profile.

Start with the source of return. Is the investment designed to produce current income from interest payments, or is most of the projected return tied to an eventual sale or refinancing event? Income generated from borrower payments may be more aligned with investors seeking retirement cash flow or a complement to fixed income.

Then look at collateral and position. Senior secured lending generally provides stronger structural protection than equity ownership or subordinate debt. A first-position mortgage on residential or commercial real estate offers a defined claim on collateral if performance deteriorates. The quality, marketability, and valuation of that collateral still matter, but lien position is a meaningful part of risk control.

Manager discipline is equally important. Investors should understand how deals are sourced, underwritten, funded, monitored, and serviced. A conservative lending platform usually has clear standards around property valuation, borrower due diligence, legal review, title position, and loan documentation. It also has a repeatable process for managing exceptions rather than improvising under pressure.

Track record deserves careful attention, but it should be interpreted correctly. High historical returns alone do not tell the full story. More useful indicators include realized losses, continuity of investor distributions, duration management, and whether the manager has navigated changing rate and credit environments without abandoning underwriting standards.

Liquidity and timing still matter

Even an attractive private investment can be a poor fit if the investor mismatches capital needs. Alternative funds are commonly less liquid than public securities. Redemption features, lockups, and funding timelines vary. That is not inherently negative, but it means investors should align commitment size with their liquidity requirements, tax planning, and distribution needs.

For retirement-focused investors using self-directed IRAs or rollover capital from old 401(k) accounts, this becomes especially relevant. The objective is often stable passive income and portfolio diversification, not frequent trading. In that context, a lower-volatility, income-oriented private strategy may fit well, provided the investor understands the holding period, custodial requirements, and distribution framework.

Where real estate-backed private debt fits in a portfolio

Real estate-backed private debt can serve as a middle ground between low-yield conventional income products and higher-volatility equity alternatives. It may appeal to accredited investors who want exposure to real estate economics without taking on direct ownership responsibilities or relying entirely on appreciation.

The strongest use case is often income diversification. If a portfolio is heavily exposed to public stocks and rate-sensitive bonds, a private credit allocation backed by hard assets may introduce a different return driver. Instead of depending on stock market sentiment or long-duration bond pricing, the investment return is linked to loan coupons, collateral, and repayment events.

This approach may also help investors who value shorter-duration exposure. Long-term real estate projects and private equity funds can tie up capital for years. By contrast, short-term bridge, renovation, or construction loans often have more defined timelines and business-purpose repayment plans. Again, that does not make them risk-free. Construction execution, borrower performance, and local market conditions still require close review. But shorter duration can reduce certain types of uncertainty.

A disciplined fund manager may further strengthen the profile by staying in first-lien positions and maintaining conservative loan-to-value ratios, often in ranges intended to preserve equity cushion beneath the lender’s capital. That collateral buffer is one of the clearest distinctions between secured private debt and unsecured income strategies.

Common mistakes investors make with alternatives

One common mistake is treating all alternatives as diversification by default. A private investment is not necessarily defensive just because it is not publicly traded. Some private strategies are highly cyclical, illiquid, or dependent on optimistic assumptions. Investors need to examine what actually drives performance.

Another mistake is overemphasizing headline yield. Higher income can be attractive, but it should be understood in context. What protections support that yield? Is the loan senior secured? How conservative is the collateral coverage? Is the manager sacrificing structure to meet a return target? The right question is not simply how much income a strategy pays, but how that income is generated.

A third mistake is underestimating operations. In private credit, servicing, monitoring, and workout capability matter. A manager that originates loans but lacks strong servicing controls may struggle when a borrower misses milestones or market conditions shift. Operational discipline is part of investor protection.

A more selective approach to alternative investments for accredited investors

The best alternative allocation is usually the one that matches the investor’s actual objective. If the goal is current income, lower volatility, and stronger downside orientation, a secured private credit strategy may deserve more weight than an appreciation-driven alternative. If the goal is long-duration upside and the investor can tolerate more uncertainty, equity-style alternatives may play a larger role.

That is why experienced investors increasingly separate alternatives into two buckets: those designed to pursue growth and those designed to protect capital while producing income. Both can be valid. But they should not be evaluated with the same lens.

For accredited investors seeking predictable cash flow, disciplined underwriting, and real asset collateral, real estate-backed private debt remains one of the more practical places to focus. Firms such as Mid Atlantic Secured Income Fund reflect that approach by centering the investment case on secured lending, conservative structure, and consistency rather than speculation. In a market that often rewards noise, that kind of discipline is worth paying attention to.

A good alternative investment should not ask you to suspend your standards. It should meet them more rigorously than the public market ever could.